Online retail sales growth slowed in May following a fairly strong April

Insight

European yields soar as ECB pivots more hawkish – Lagarde fails to rule out hiking in 2022

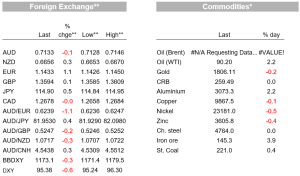

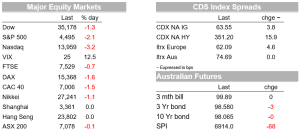

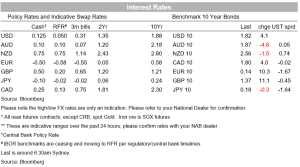

The hawkish pivot from central banks continued overnight with the ECB President refusing to rule out a rate increase this year, and across the Channel the BoE were split on the possibility of hiking by 50bps (4 out of 9 wanted to hike by 50bps). Yields spiked in Europe with German 10yr yields +10.3bps to 0.14%, along with UK 10yr Gilt yields +11.1bps to 1.37%, and spilled over to US markets with the 10yr Treasury yield also +5.9bps to 1.83%. FX followed the move in rates with EUR skyrocketing +1.1% to 1.1436, and bringing down USD indexes given its large weight with the DXY -0.6% overnight. The EUR lift though did help other pairs a little higher with NZD +0.3% and AUD little changed. Equity markets tanked with the initial moves driven by Meta’s (i.e. Facebook’s) earnings disappoint after the close yesterday, though losses have extended following the ECB’s hawkish pivot with the S&P500 -2.1% as we head into the last hour of power.

First to the ECB’s hawkish pivot. ECB President Lagarde shocked markets overnight with a dramatic shift in language, opening up the possibility of a 2022 hike as markets had been pricing into the meeting. President Lagarde declined to rule out a rate hike this year, which is a big change from her attitude in December when she said it was “very unlikely”. Lagarde noted “risks to the inflation outlook are tilted to the upside, particularly in the near term” and signalled the potential for a major policy pivot at an upcoming meeting: “Our March meeting, and then later on, our June meeting will be critically important to determine whether the three criterias of our forward guidance are fully satisfied.” The market ramped up pricing for ECB rate hikes this year following the press conference, with around a 70% chance of a 10bps move now priced for June and more than 40bps now priced-in by the end of the year.

Press reports following the ECB meeting hinted a major policy pivot is likely with the FT reporting

“one or two ” ECB members had called for an immediate tightening of policy. As for the ECB’s QE programs, Lagarde confirmed the ECB’s pandemic bond buying programme would stop in March, although a separate bond buying programme would continue, at a temporarily increased rate, from this point. Bloomberg later reported that the ECB could stop all bond purchases as early as Q3, which would be earlier than previous guidance. When the ECB stops buying bonds is important because Lagarde has repeatedly said that it would only raise rates after this point, and feeds through to expectation of a major hawkish pivot. In summary the ECB has clearly opened the door to ending asset purchases and hiking rates multiple times this year.

Across the Channel the BoE also met and were also extremely hawkish. While the BoE hiked rates by 25bps as expected, four out of nine MPC members wanted a 50bps hike!. The BoE now sees inflation peaking at around 7¼%, more than 1% higher than previously, even though it is projected to be slightly below target in two years’ time (based on market pricing for rate hikes). The four members who voted for the 50bps argued that inflation pressures were broadening, and a larger rate move would reduce the risk that inflation and wage expectations become embedded at uncomfortably high levels. The majority argued that raising the cash rate by increments greater than 25bps “ could have an outsized impact on expectations for the further path of policy, which was already sufficient, in the central projection, to push inflation well below the target in year three of the forecast”. Note the market path was for the Bank Rate to rise to around 1½% by mid-2023 (see BoE Meeting Minutes for details).

The BoE also confirmed its earlier decision to stop reinvestments on its bond portfolio now that its policy rate was at 0.50%, which will see its holdings shrink over time (a process sometimes referred to as ‘quantitative tightening’), with active sales of its government bond holdings planned once the cash rate reaches 1%. Finally, in a surprise move, the BoE said it would start to sell down its £20b corporate bond holdings, judging that the relatively small size of the holdings and well-functioning state of the market meant that this could be done with relatively little impact. UK rates were higher by 9-11 bps across the curve, with the market increasing its BoE rate hike expectations (and now putting a small chance on a 50bps increase at the upcoming March meeting). The 10-year rate hit a fresh 3-year high of 1.37% although the reaction in the GBP has been more muted, just 0.2% higher on the day, to 1.3605.

As for European yields, the 2-year German yield, which crossed above the -0.5% deposit rate for the first time since 2015 just days ago, spiked 13bps higher, to -0.33%. 10-year yields were higher by 10bps in Germany, to 0.14%, and as much as 21bps in Italy, the main beneficiary of the ECB’s huge bond buying programme and ultra-easy monetary policy stance. The EUR has experienced a big rally, up by more than 1.1% to 1.1440. Higher UK and European rates have flowed through other markets, with the US 10-year rate 6bps higher, to 1.83%, and the Australian 10-year bond futures yield up by a similar amount. Rate hike pricing for the Fed also lifted slightly to 4.9 hikes priced in 2022 with a 20% chance of a 50bps move in March. In currencies, the stronger EUR has helped the NZD and AUD move higher overnight, with the NZD up around 0.3%, while the AUD has given back its gains following the sharp fall in US equities with the AUD -0.1% to 0.7133

Equity markets have tanked with the NASDAQ so far down 3.2% as we head into the last hour of power, giving back some its recent strong rally, while the S&P500 is down 2.1%. Social media giant Meta (formerly Facebook) reported disappointing results after the close yesterday, notably reporting a decline in daily active users for the first time amidst rising competition from the likes of TikTok, which saw Meta’s share price collapse 26.3%. Given Meta’s chunky 2% weight in the S&P 500, its share price is responsible for around a quarter of the decline in the S&P500 decline. Equities have extended losses over following the ECB’s hawkish turn, broadening the sell-off in tech given concerns around valuations as rates start to rise globally. .

Data has been completely overshadowed by the central bank news. The ISM Services index was slightly better than expected at 59.9 against the 59.5 consensus. Encouragingly US jobless claims were lower last week at 238k against 245k expected and 261k previously, as the impact of Omicron fades. Also important in the UK was the energy regulator, Ofgem deciding to increase the energy price cap by 54%. The energy price cap will increase from 1 April for approximately 22 million customers. Those on default tariffs paying by direct debit will see an increase of £693 from £1,277 to £1,971 per year (difference due to rounding).

Coming up today:

Domestically the RBA SoMP is out, though it may not yield as much attention as previous vintages given Governor Lowe’s extensive comments earlier in the week. Offshore it is all about Payrolls and while headline payrolls will grab the media attention, market focus will likely be on the unemployment rate and average hourly earnings given these are key to interpreting how tight the labour market is and whether inflation pressures will be more persistent then the Fed currently expects. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.