Total spending grew 0.9% in June.

US CPI came in a tenth below consensus on both the headline and core rates, leaving yields sharply lower, the USD weaker, and equities higher.

AU: Westpac consumer conf, Nov: 79.9 vs. 82.0 prev.

AU: NAB business conditions, Oct: -2 vs. 1 prev.

GE: ZEW survey expectations, Nov: 9.8 vs. 5.0 exp.

EC: GDP (q/q%), Q3: -0.1 vs -0.1 exp.

US: NFIB small business optimism, Oct: 90.7 vs. 90.5 exp.

US: CPI (m/m%), Oct: 0.0 vs. 0.1 exp.

US: CPI ex food, energy (m/m%), Oct: 0.2 vs. 0.3 exp.

US: CPI (y/y%), Oct: 3.2 vs. 3.3 exp.

US: CPI ex food, energy (y/y%), Oct: 4.0 vs. 4.1 exp.

“yeah, slow, Come on and dance with me, yeah, slow” – Kylie Minogue

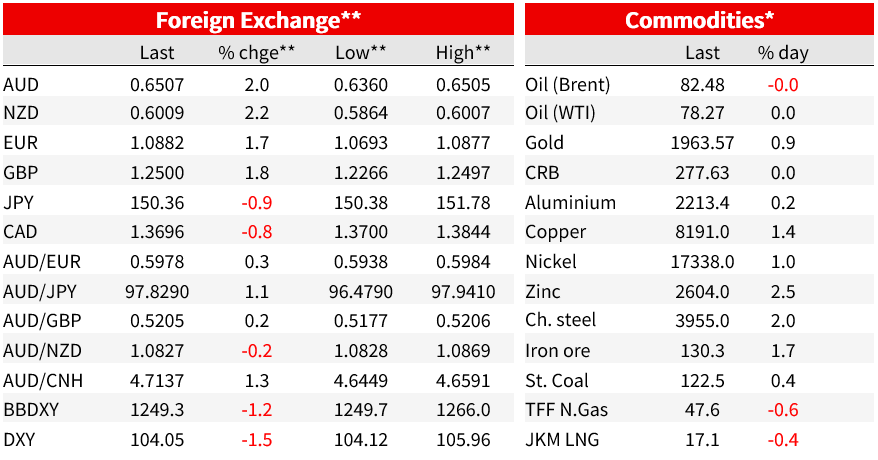

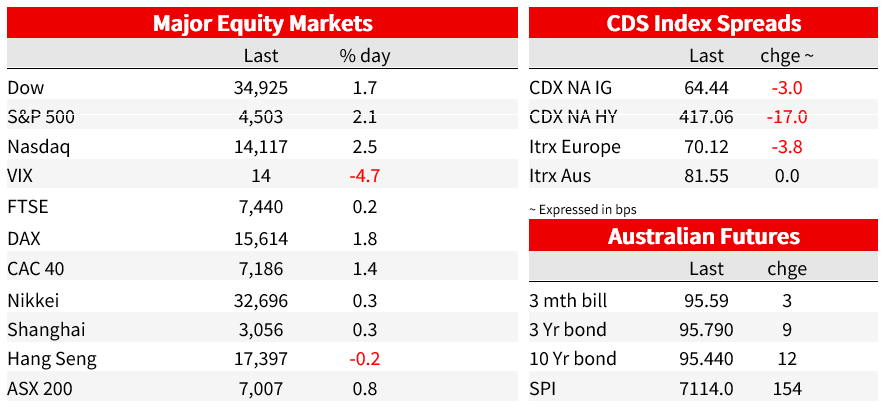

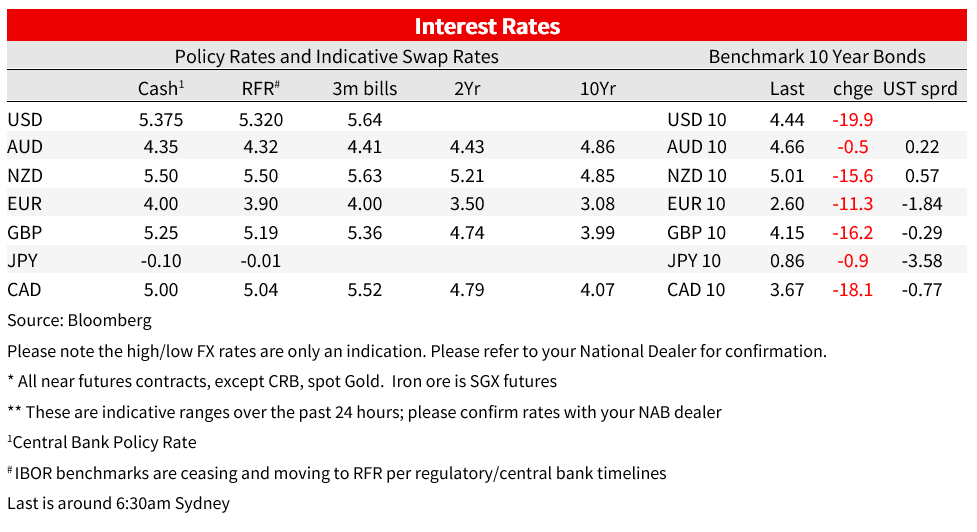

US CPI came in a tenth below consensus on both the headline and core rates. Yields are sharply lower across the curve, led by a 22bp decline in the 2yr to 4.82% and the US dollar is lower. Market pricing removed the remaining small chance of a December hike and brought forward easing with 100bp of cuts now priced over 2024. The US dollar is broadly weaker, down 1.4% on the DXY and equities are sharply higher.

The CPI was unchanged in October against consensus for a 0.1% gain. The headline was weighed by an 8% fall in gasoline prices, but the core, at 0.2% m/m, was also a tenth below consensus. In 3m annualised terms, core inflation eked higher to 3.4%, but the 6m annualised shows an ongoing downtrend at 3.2%. That’s too high but encouragingly does show a gradual disinflating trend looks intact. In contrast, 6m annualised inflation was stubborn around 5% through 2022. Alternate underlying measures calculated by the Cleveland Fed showed similar slowing in October. Median CPI rose 0.3% m/m in October after 0.5% m/m, while the 16% trimmed mean rose 0.2% m/m after 0.4%.

Supporting the slowdown in price gains was a moderation in rents inflation. Rents were up 0.4% m/m in October, resuming their modest downtrend after a surprising pick up in September. Advertised rents point to some further help from this component. Elsewhere in Shelter, lodging away from home slid 2.9% m/m. ‘Supercore’ services, which excludes shelter and food service, was 0.2% m/m, even after a change in methodology to semi-annual adjustment saw health insurance costs swing from declines to a 1.1% m/m increase. As for goods, car prices were lower (new cars -0.1% m/m and used cars -0.8% m/), and other core goods prices were essentially flat for 5th month.

Speaking after the data, Fed officials were cautious, but did little to sway the market reaction. Chicago’s Goolsbee said “progress continues, though we still have a way to go.” For Goolsbee “With goods inflation already coming down and nonhousing services inflation typically slow to adjust, the key to further progress over the next few quarters will be what happens to housing inflation.” Richmond’s Barkin warned he’s “ just not convinced that inflation is on some smooth glide path down to 2%” and cautioned that “Shelter and shelter inflation remain higher than historic levels. So does services inflation.” Absent a government shutdown, there is the November CPI print to come just ahead of the December FOMC meeting.

That note of caution didn’t dampen the market reaction to good news in the CPI. The 2yr yield was 22bp lower at 4.82% and is currently around its intraday lows . The move takes the 2yr back to its levels post payrolls on 3 November. Amid increased confidence that the Fed is done and a pull forward of cut pricing, the curve bull steepened, but only marginally so. The 10yr yield was 20bp lower to 4.44%, its lowest since 25 September while the 30yr was 13bp lower to 4.62%. Markets now price 54bp of cuts by July and 100bp by end 2024, down from 32bp and 74bp a day prior. The move in US rates led global yields lower. German 1oyr bunds were 11bp lower to 2.6%, and 10yr gilt yields slipped 16bp.

The dollar was lower, down 1.4% on the DXY. Declines came against all G10 currencies. The euro was 1.7% higher to 1.0876, its highest since 1 September and the pound gained 1.8%. The Aussie and Kiwi were towards the top of the G10 pack, up 2.0% and 2.2% respectively. The AUD currently sits at it’s intraday high, having just broken above 65c at 0.6505 and back around its pre-RBA level.

Equities gained. The S&P500 was 2.1% higher heading into the last hour of trading. The Nasdaq was 2.5% higher. Gains were broad-based, with Bloomberg noting 95% of names in the S&P500 were in the green. Gains were led by real estate, utilities and consumer discretionary. European shares also got a boost after the CPI data, the Euro Stoxx 50 ending the day 1.4% higher, after being little changed before the data.

In commodities, the International Energy Agency (IEA) said the oil market should return to surplus in early 2024 even if Saudi Arabia extends its production cuts that have tightened supplies this year. The IEA said slowing economic global growth and increased supply should reduce the draw on stockpiles. Brent crude prices were little changed near US$83 per barrel.

In New Zealand, new monthly price indices for selected goods and services that cover around 44% of the consumer prices basket were released yesterday. The new indices complement existing monthly data on food prices and rents and point to still further downside risk to the RBNZ’s Q4 inflation projection of 5.2% y/y from the August Monetary Policy Statement.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.