NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Inflation and related central bank thinking remains by far the bigger influence on market sentiment

Well in Russia actually, where French President Macon is sitting down with Russian president Putin (and which, judging by the photos on the BBC’s website, is at either end of a very long board room table inside the Kremlin – not much scope for kissing there). At the same time US President Biden and German Chancellor Olaf Sholz are meeting in Washington.

While diplomacy is in motion, markets seem prepared to proceed on the basis that military action inside Ukraine is a tail risk not base line view, hence risk sentiment has begun the week on the front foot, showing gains of almost one percent in the key European equity indices (Eurostoxx 50, FTSE 100, CAC40 and Dax all up 0.8%) while US stocks are showing small gains with an hour or so of New York trade still to go. The key European benchmark gas price is down about 5% to EUR 77.50 per Mwh – compared to EUR180 at its (brief) peak last year, but still almost four times what it was a year ago.

For now at least, inflation and related central bank thinking remains by far the bigger influence on market sentiment, in which respect ECB President Christine Lagarde has been addressing the EU parliament overnight, where she spoke of the intent to adopt a ‘gradual’ approach to policy adjustments and stressed the highly data dependent nature of any such action. This though doesn’t rule out a significant formal ‘tilt’; from the ECB when it sits down with new forecasts in March and where revised guidance on its Asset Purchase Programme (APP) following the end to the Pandemic Emergency Purchase plan (PEPP) at the end of Q1, seems likely.

Recall that late last year, the ECB suggested the APP would step up to EUR40bn a month in Q2 before tapering to 30bn in Q3 and 20bn in Q4, with no assurance it would then end. Now, the speculation is whether they will draw a line under the APP in Q3 or perhaps as early as Q2, then opening the door to a lift-off in rates from the current -0.5% floor in H2 2022 and possibly as soon as Q3. On the weekend, Dutch central bank governor Klaus Knot was the first Governing Council member to opening advocate for a first rate rise before the end of this year.

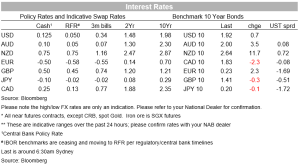

Eurozone bond markets continue to take on board the discernible shift in rhetoric that came out of last week’s ECB Governing council meeting (and the various ‘source’ stories that quickly followed). This is showing up more or Eurozone peripheral bond yields – the relatively bigger beneficiaries of ECB bond buying to date – with 2-year Spain and Portugal up 5-6.5bps and Greece 17.5bps (while at 10 years, Greece is up 22bps). German 10-year Bunds have added another 2bps to 0.22%, bringing the year-to date change to 60bps and 72bps up on their record low of -50bps last August). This, incidentally, is a very similar in magnitude to the back-up we have seen in US 10-year Treasuries over the same period, while Bunds have risen by more than Treasuries so far this year. A message that only in the last few days is no longer being lost on the EUR/USD exchange rate. Treasuries show a 0.5bp rise at 10-years (having been just shy of 1.94% earlier in the night) and 2bp fall in the 2-year.

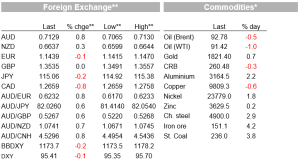

EUR/USD has actually given back a (very) little of last week’s post-ECB gains at the start of the week, suggesting that some consolidation of those gains is the order of the day – at last ahead of Thursday’s US CPI release or news out of the Putin/Macron meeting. The AUD in contrast has recovered a good chunk of last Friday’s losses , to be the best performing G10 currencies Monday, currently +0.8% at 0.7130, closely followed by CAD. No other G10 currency is up by more than 0.25% on last Friday’s New York close (and meaning the AUD/ND cross has pushed back up to 1.0736, albeit still beanth last week’s post-June 2021 high of 1.0771. Of some encouragement to the AUD has been China’s return to the fray after last week’s LNY holidays with, as yet, no weakening in the CNY from pre-holiday levels, while benchmark Shanghai stock indices put on gains averaging 1.5% on their first day back.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.