We see our NAB commodity index falling substantially in 2024, despite higher forecasts for base metals and gold.

Insight

It was a busy 24 hours for data flow globally. Yields partially retraced yesterday’s post-CPI bond rally, while equities have held onto gains.

Events round-up

NZ: Card spending total (m/m%), Oct: -0.3 vs. -0.2 prev.

NZ: Net migration, Sep: 7510 vs. prev. 12350

JN: GDP (q/q%), Q3: -0.5 vs. -0.1 exp.

AU: Wage price index (y/y%), Q3: 4.0 vs. 3.9 exp.

CH: Industrial production (y/y%), Oct: 4.6 vs. 4.5 exp.

CH: Retail sales (y/y%), Oct: 7.6 vs. 7.0 exp.

CH: Fixed assets invest., (YTD (y/y%), Oct: 2.9 vs. 3.1 exp.

UK: CPI (y/y%), Oct: 4.6 vs. 4.7 exp.

UK: CPI core (y/y%), Oct: 5.7 vs. 5.8 exp.

EA: Industrial production (m/m%), Sep: -1.1 vs. -1.0 exp.

US: Retail sales (m/m%), Oct: -0.1 vs. -0.3 exp.

US: Retail sales ex auto, gas (m/m%), Oct: 0.1 vs. 0.2 exp.

US: PPI ex food, energy (m/m%), Oct: 0.0 vs. 0.3 exp.

US: PPI ex food, energy (y/y%), Oct: 2.4 vs. 2.7 exp.

US: Empire manufacturing, Nov: 9.1 vs. -3.0 exp.

It was a busy 24 hours for data flow globally. Overnight, US retail sales fell less than expected and PPI showed a larger fall than expected. US yields were higher, partially retracing some of their sharp falls yesterday, but with the data providing more fodder for the growing confidence in a soft landing, equity markets held onto their gains and the US dollar was only modestly higher. Elsewhere, UK inflation fell slightly more than expected, Japanese GDP was soft, and retail sales provided some room for optimism from Chinese Activity data. San Francisco Fed’s Daly, speaking with the FT, refused to rule out another interest rate increase.

US retail sales fell 0.1% m/m in October, less than the 0.3% expected. That was on the back of a s maller decline in gas sales than expected, down only 0.3% despite a near 6% fall in prices. The control group, which feeds more directly into consumption data, was in line with expectations at +0.2% m/m, and there were small upward revisions to the September data. Strength in real consumption through the third quarter always looked unsustainable, but this is suggestive of still positive consumption growth heading into the holiday season.

On PPI, the headline fell 0.5% (-0.1% expected), weighed by energy and especially gasoline prices, but the core was also lower, unchanged vs +0.3% expected. A 0.7% fall in trade services margins offset gains elsewhere and suggests some squeeze on margins is supporting the disinflation process as the demand and supply balance improves. The Empire Manufacturing Survey was stronger than expected at +9.1 vs -3.0 on the headline sentiment measure, but that masked a soft underbelly. The subindexes mostly were weaker than the headline sentiment measure, with orders, employment, and the workweek down, though shipments rose.

A couple of hours ago, The FT published an interesting interview with San Francisco Fed’s Daly. She said that a further deceleration in inflation was “very, very encouraging,” said the risk of a significant slowdown or steep rise in unemployment had lessened, but warned against declaring victory to early, wanting to avoid a ‘stop-start’ mentality that would be disruptive and makes it difficult for people to plan. Asked about her approach to rate cuts next year, she drew a distinction between easing and normalising “ At some point, we won’t want to be sufficiently or very restrictive, we’ll want to be bringing policy to a more normal path because we think the economy is in train to be normalising”

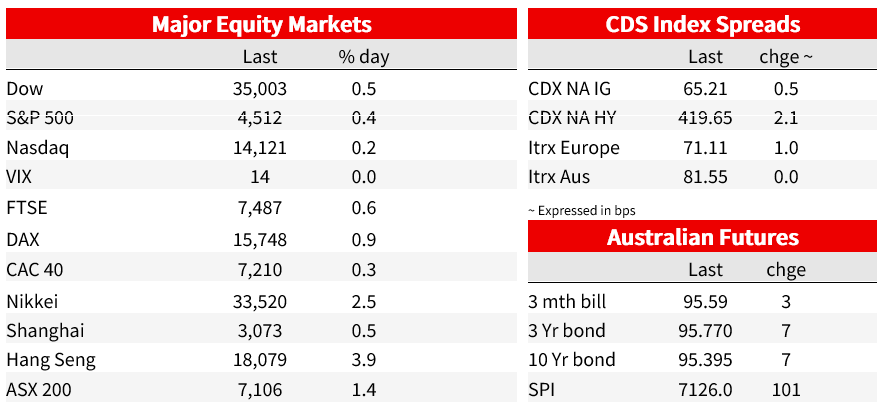

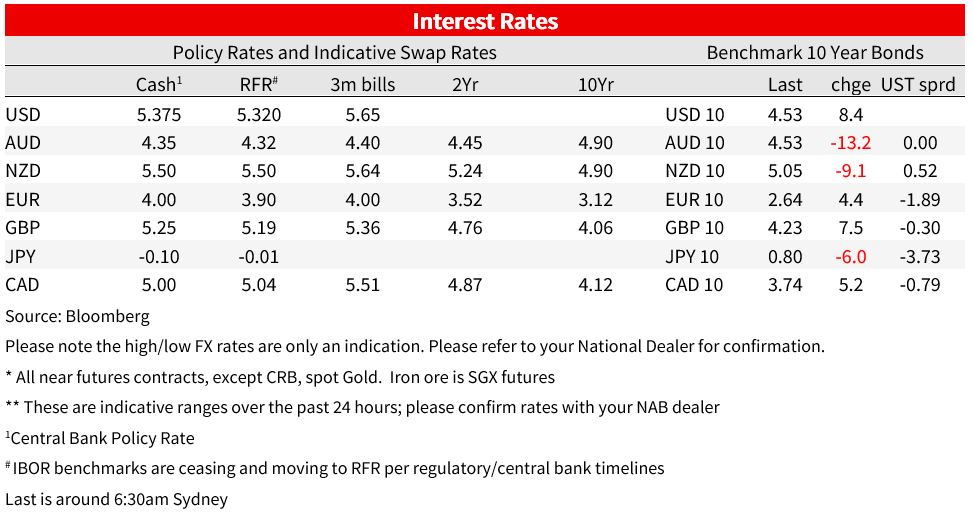

US yields are higher with signs of resilience in the consumer despite more good news on the inflation front out of the PPI , but importantly in the context of the sharp fall in yields the prior day. US 10yr yields are 8bp higher to 4.53%, still 11bp lower than pre-CPI, while 2yr yields were 8bp higher to 4.91%, 12bp below pre-CPI levels. The data was supportive of equities, which held onto yesterday’s gains and are currently tracking in the green. The S&P500 up around 0.4% and above 4500. Solid earnings for Target were a support, with fewer markdowns and better inventory management supporting profits even as sales slid.

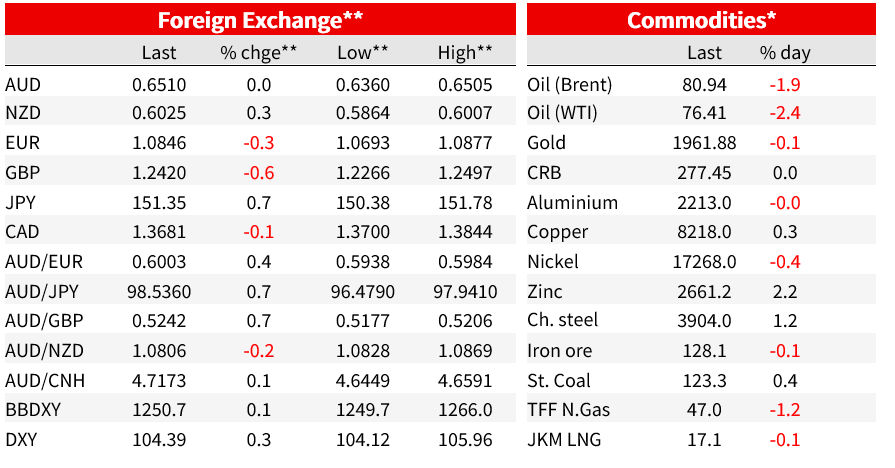

In currency markets, the USD was 0.3% higher on the DXY. The euro fell 0.3% lower, with larger gains coming against the yen and the pound. The AUD was little changed at 0.6510, a net positive surprise out of Chinese data providing some support at the margin. USDJPY gained 0.7% to be back above 151. Japanese GDP surprised lower at -0.5% q/q vs -0.1% expected. The misses came across consumption, investment and inventories while prior Q2 data was also revised lower. Overall, it supports the BoJ’s cautious approach. Japanese 10yr yields were 6bp lower at 0.80%. GBP slid 0.6% to 1.2420, weighed by a downside surprise on inflation.

UK inflation slid to 4.6% from 6.7%, below expectations for 4.7%. The fall was driven by base effects from energy and a fall in household energy tariffs. Electricity, gas and other household fuels swung from adding 0.5ppt to year-ended headline in September to subtracting 1.1ppt in October. But c ore inflation also slowed to 5.7% from 6.1 and services inflation slowed to 6.6% from 6.9%, each a tenth better than expected and boding well for faster improvement than the BoE though. With UK yields having moved the prior day in the global repricing following US CPI, UK gilt yields were higher alongside higher global yields, with 10yr gilts up 8bp to 4.23%. A cut is near 90% priced for June, pulled forward from August at the start of the week.

Chinese activity data yesterday provided a small net upside surprise. That was led by Retail Sales, up 7.6% y/y vs 7.0% expected, with Industrial Production coming in 4.6% vs 4.5% expected. Retail sales growth accelerated from 5.5% in September, flattered by base effects as many cities were in lockdown a year ago, but also suggestive of a pick-up in consumption momentum. Investment growth remained subdued, with YTD fixed asset slowing to 2.9% y/y from 3.1% (3.1% expected). The PBoC left the 1yr MLF rate at 2.5%, as widely expected.

In Australia yesterday, Q3 WPI growth was in line with consensus on the quarterly at 1.3% q/q but a little higher over the year at 4.0% y/y (Consensus 3.9%). While upward revisions mean the y/y rate could be tracking marginally above the RBA’s year-end forecast for 4.0%, There data was broadly in line with the November SoMP assessment. The quarterly outcome was the largest in the 26-year history of the WPI, but it was no surprise given the large contribution from the award wage increase and a one off pay level adjustment for aged care workers. Of some note and explaining the y/y beat, updated seasonal factors that resulted in upward revisions to wages growth estimates over the first half of 2023. Overall, nothing to trouble RBA pricing, with nothing priced for December and about 45% of a hike priced by February. CPI and GDP data will be key ahead of the February meeting.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We see our NAB commodity index falling substantially in 2024, despite higher forecasts for base metals and gold.

Insight

Online retail sales growth slowed to almost flat in March

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.