On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

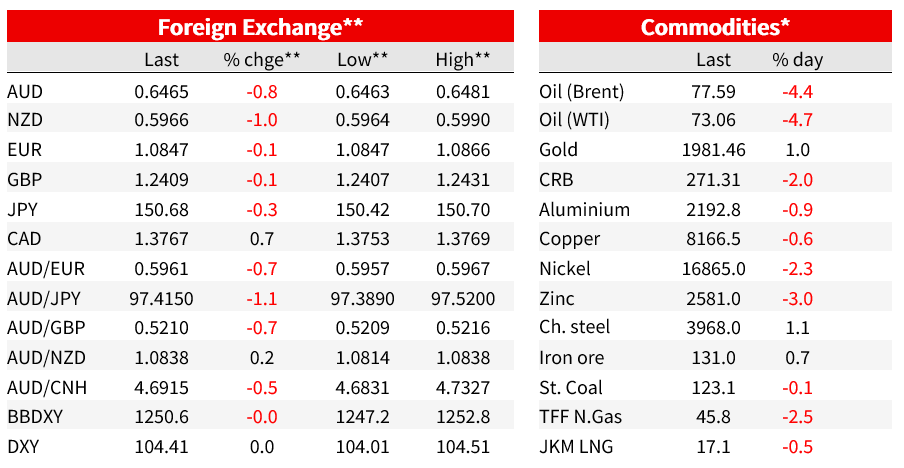

A choppy session with softer-than expected second-tier US data seeing yields fall, while the USD gained smalls and commodity currencies underperformed

Key data/headlines

US: Initial jobless claims (k), wk to 11-Nov: 231 vs. 220 exp.

US: Philly Fed business outlook, Nov: -5.9 vs. -8.0 exp.

US: Industrial production (m/m%), Oct: -0.6 vs. -0.4 exp.

US: NAHB housing market index, Nov: 34 vs. 40 exp.

BN: Oil Plunges to July Low as Algorithms Amplify Supply-Driven Drop

BN: Walmart CEO Sees Potential for Deflation in Coming Months

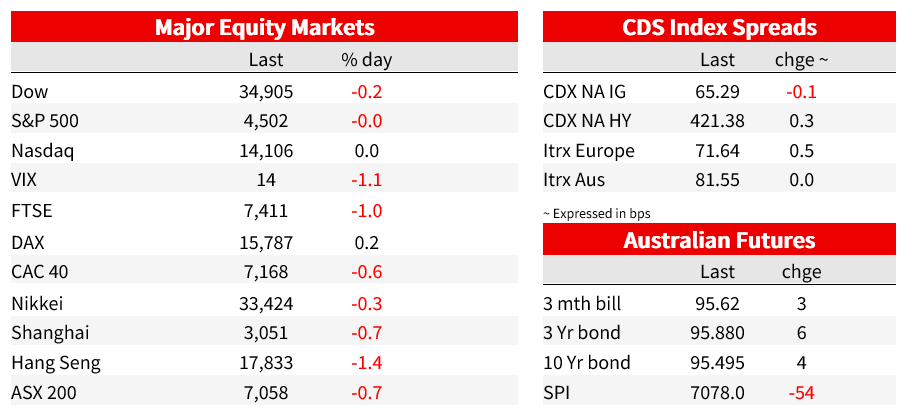

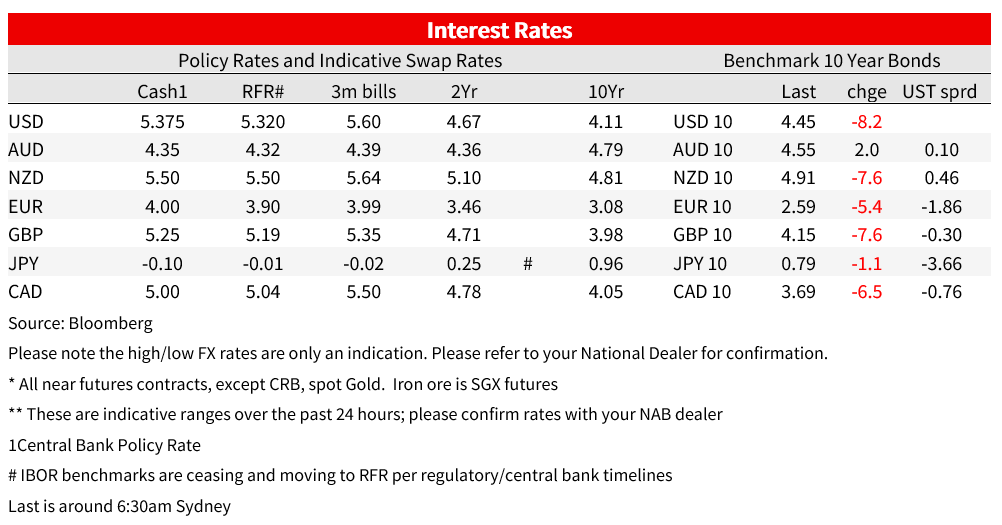

A choppy session with softer-than expected second-tier US data seeing yields fall, while the USD gained smalls and commodity currencies underperformed (AUD -0.8%). The pick of the data was US Jobless Claims which were 231k vs. 220k expected. Yields fell in response and over the past 24 hours the US 10yr is -8.8bps to 4.4% (high 4.54%; low 4.43%), with a similar move seen in 2yrs at -8.1bps to 4.84%. The moves continue to be reflected in real yields. 10yr TIP yield -6.6bps to 2.16% (implied breakeven was -2.3bps to 2.29%). Fed funds pricing has extended cuts with now 99bps worth of cuts priced for 2024, up from 89bps yesterday and well up on the 73bps seen last week. Also catching your scribe’s eye was a snippet from the Walmart CEO warning that “ we may be moving through a period of deflation in the months to come” with those comments sour candy for the stock price with Walmart stock -8.2%. The overall S&P500 into the last half hour of trade is -0.2%, weighed down by energy (-2.4%) with Brent -4.7% to $77.38

First to the second-tier US data. Initial jobless claims were 231k vs. 220k expected and 218k previously (and highest in 12 weeks). Continuing claims 1,865k vs. 1,843k expected and 1,833k previously. Overall the data is consistent with some softening in labour market conditions , though the data itself is volatile and prone to revision and it may be too early to extrapolate trends. Industrial production also printed on the soft side at -0.6% m/m vs. -0.4% expected and 0.1% previously. Importantly though the UAW strike drove a 10% plunge in motor vehicle production, and the strike came to an end on 30 October, and GM and its union just approved a new agreement, so output likely will recover in November. Other data pointed to softness was the NAHB homebuilder sentiment index which fell 6pts to 34, its lowest level this year, suggesting a lack of confidence in the building market against a backdrop of poor affordability. The Philly Fed business outlook index was the only indicator to positively surprise, although it remained in negative territory at -5.9.

The big mover in commodities was oil with Brent -4.7% to $77.38. There wasn’t any data to drive the plunge and Bloomberg headlines noted the failure of key technical support levels with algorithm-driven traders dumped crude holdings after prices dipped below $80 a barrel. Either way the supply situation looks ample with supplies remaining robust despite OPEC+ supply cuts and reduced Russian exports. Yesterday it was reported US oil stockpiles rose to the highest level since August. Uncertainty around Chinese oil demand is also a factor weighing on oil. The trade of the decade it seems has to go to the White House, selling strategic petroleum reserves at the peak and pledging to buyback at $75 a barrel (WTI now $72.85).

In the equities space two articles worth noting. Walmart is down some 8% into the last half hour of trade after the retail giant lowered its expected earnings forecast. It was reported that some unexpected softness was seen in the late bit of October. On the prices side Walmart’s CEO McMillion said “we may be moving through a period of deflation in the months to come,” and “We’re happy about it,”. It appears pricing power is starting to evaportate on the consumer goods side with that likely good news in so far as CPI/PCE reports go and for prospects of Fed rate cuts in 2024. As for the softness in late October, Walmart’s CFO pointed to a number of factors that could explain the weakness, including credit tightening, repayment of student loans and also “anomalous weather” in the back half of October. UK retailer Burberry also saw its stock down 9%, noting weakness in China, but also comparable store sales in the US fell 10%. It seems the luxury outperformance of H1 2024 has well passed.

In FX it has been mixed with slight USD strength and commodity currencies underperforming. The USD DXY is broadly flat over the past 24 hours with USD/JPY -0.3%, EUR -0.1% and GBP -0.1%. Commodity currencies have underperformed with AUD -0.8%, NZD -1.1% and USD/CAD +0.7%. The sharp fall in the oil price is one factor, but weakness was also seen in the Asian trading sessions which seemed to coincide with another weaker reading on Chinese house prices that sent the yuan on a weaker trajectory. The yuan reversed course and the AUD and NZD rose, but fell back. Whether coincidental or not, the stronger yuan has seen sustained following what seems to be improved US-China relations. Presidents Xi and Biden met for hours of talks in San Francisco. After the meetings, President Biden tweeted a series of warm fuzzies including that the meetings “ were some of the most constructive and productive discussions we’ve had”.

There have been several Fed speakers overnight, but nothing market moving. In opening remarks, at the Financial Stability Conference, Fed Mester said that there had been good progress on getting inflation down even as the economy remained relatively strong, but she also noted that “It’s going to take some time to get inflation back down to 2%.” Fed Governor Cook said that she is “attuned to the risk of an unnecessarily sharp decline in economic activity and employment,” but also noted that the continued momentum in economic growth and consumer spending could slow the pace of disinflation. In other news the US Senate has approved a temporary funding measure, averting a government shutdown and delaying a decision on spending until early 2024.

In Australia, yesterday’s October employment was much stronger than expected at 55.0k vs. 24k consensus. With the part rate lifting two tenths, the unemployment rate rose two tenths to 3.7% as expected and unemployment has been between 3.4-3.7% since mid-2022. Our read on the data was that it keeps the RBA on the sidelines in December, but keeps alive another hike in February as is NAB’s call. The recent RBA November SoMP saw the unemployment rate at 3.8% in Q4 2023. The RBA’s Kohler also noted on Monday that their newly created labour market “dashboard suggests that the labour market remains quite tight across a range of dimensions”, and nothing yesterday’s dispels that notion.

Unclear whether Martin Place is background briefing, but the AFR RBA whisperer John Kehoe was out with an opinion piece yesterday making similar remarks to the above: “It won’t increase the cash rate at its December meeting. By February, the central bank will have inflation figures for the December quarter and a new set of economic forecasts.” It could be that the RBA is taking some heart from recent US inflation reads: “ signs that US inflation is falling faster than anticipated – to 3.2 per cent – and the Federal Reserve may be finished its interest rate hiking cycle will also give the RBA some quiet comfort. But the Fed has done more heavy lifting on interest rates and appears to be reaping the rewards with lower inflation. Australia’s higher headline inflation rate of 5.4 per cent gives the RBA less wriggle room for upside inflation surprises.” (see AFR Kehoe: Jobs and wages won’t move the RBA this year).

Finally, there is lots of talk about what the Australian government’s scrapping of about 50 infrastructure projects may mean for state government finances.

Coming up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.