On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

The key question as yields march higher is how high can they go in this cycle?

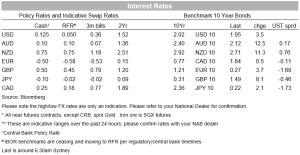

Global yields continued their march higher in what was a quiet night for news. US 10yr yields rose +3.1bps to 1.95%, following the move in UK Gilt Yields (+8.1bps to 1.49%). Bond supply seems to have been a driver in the absence of any other news with a 50yr Gilt issued (£4.25bn, issued at 3bps less than the current 50yr yield). Supply was also seen as a driver of the sell-off in Aussie rates yesterday where the Aussie 10yr yield rose 12.5bps to 2.12%. Also in the background was news of a former RBA Board Member arguing for four hikes in 2022 (see WSJ: Australia Central Bank Likely to Raise Cash Rate Four Times by Year-End ). So far the rise in yields overnight hasn’t affected US equities with the S&P500 up 0.5% as we head into the last hour of power. Solid earnings beats have helped insulate with Harley-Davidson the latest with its shares up 8%. FX moves have been modest with the USD (DXY) edging up +0.2% with the AUD +0.4% to 71.36.

The key question as yields march higher is how high can they go in this cycle? Market proxies for terminal rates have lifted a little, but still remain below where central banks think their neutral rates are – e.g. US 5Y1Y OIS FWD Swaps are currently 1.86%, up from 1.75% on Friday, but below the Fed’s 2.50% longer run neutral dot. Markets are clearly discounting how high rates can go without seeing a significant slowing in the economy. Some flavour of that of course is seen in the curve flattening that has been playing out with US 2s10s at 60.9bps and 7s10s having been on the cusp of inverting at 2.5bps. The UK’s NIESR also plays to that view, noting: “ Recession risks are rising. If the downward momentum that we see for growth were to continue, then a recession could emerge. The risks are clearly there” and “It would only take one more negative shock” (see The Telegraph: Bank of England failures leave Britain ‘just one shock from recession).

As for the near term picture, markets of course are waiting on Thursday’s US CPI where headline is expected to reach new heights of 7.3% y/y and 5.9% for the core.. There is also some talk of MBS convexity hedging that may emerge if yields breach 1.95%, which could help drive yields higher from here. Japan’s also 10-year rate traded as high as 0.21%, getting close to the BoJ’s tolerance limit and traders are contemplating whether the BoJ will soon step in to defend the market. Although equities have been resilient to the rise in yields over recent days, it is worth noting that there has been a more wary tone as far as future guidance with 34 giving negative earnings guidance, while only 13 had given positive guidance according to Fact Set. This likely means equity market sentiment remains fragile.

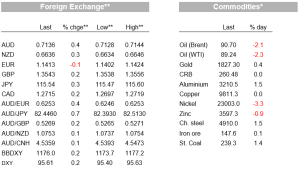

In other news the mood music on the Russia/Ukraine situation sounds a bit more positive , after French President Macron’s meeting with President Putin. Macron said he received assurances from Putin that Russia wouldn’t escalate tensions further around Ukraine and he would withdraw thousands of Russian troops from Belarus after completion of planned exercises. A Kremlin spokesman cast some doubts on Macron’s version and Macron’s office later clarified that the assurances were “conditional” and could change. Still, we’ll take that as a win. Oil prices fell around 3% for the day on the talk of descalation of the Ukraine situation and the resumption of Iran nuclear talks, which could potentially lead to increased supply on any deal. After hitting the $94 per barrel mark late last week, Brent crude briefly went as low as sub-90 this morning.

Meanwhile iron ore prices rose through the $150 per ton mark after China set 2030 as the new deadline for peak-emissions for the steel industry, five years later from the prior 2025 target. This is part of President Xi’s strategy to reduce the impact on the economy from China’s climate change policies. The move likely highlights the need to stimulate the economy given headwinds, buying time to ramp up infrastructure spending in what is a pivotal year for Chinese political. Note iron ore prices had troughed in the low 90s in November and have been on a steady rise since.

In economic news, the US trade deficit for December was slightly lower than expected but for 2021 was still the largest on record, up 27% on the previous year at $859b, another sign of an over-heated economy as stimulus funds sucked in greater imports. The NFIB small business optimism index fell to an 11-month low, close to expectations. Inflation indicators rose to record highs for the survey which dates back to 1986, with 61% of firms reporting increasing average selling prices and 50% of firms saying they boosted wages, given the difficulty in finding labour.

Currencies show modest movements. The AUD has largely tracked sideway at 0.7130s, but is up 0.4% on our strict 24 hour measurement. The AUD did get a lift yesterday from some hawkish soundbites from former RBA Board member John Edwards in which said he expects the RBA to raise rates four times in succession later this year. Other FX pairs were also similarly little moved with the USD DXY marginally higher by 0.2% given higher rates.

Finally, yesterday’s Australian NAB Business Survey shows only a modest impact from the Omicron variant on both conditions and confidence. Business Conditions in January fell to 3 from 8, and importantly is only just below its long-run average of 6. While the activity hit from the omicron variant appears shallow, price pressures are building further. 3m annualised purchase costs and final prices hit record highs. Purchase Costs 3m annualised are running at 11.7%, Final Prices 3m annualised are running at 5.6%. Meanwhile Retail Prices continue to be near series highs at 5.6%. Labour costs (wages bill) is also close to series high at 7.1% annualised. All suggests the RBA is likely to be surprised again on inflation in Q1 and Q2, while there are some signs of wages picking up as well.

Domestically it is quiet with only the W-MI Monthly Consumer Confidence Index. Offshore it is also quiet with the only top-tier piece of data being Chinese Aggregate Financing figures due to be published any day now. Central Bank speak also continues with BoE’s Pill hitting the airwaves, while the Fed’s Bowman and Mester are also on the roster. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.