Firmer consumer and steady outlook

Insight

Another choppy night on bond markets with 10yr yields on net little changed and the curve twist flattening slightly.

Key events/headlines

UK: Retail sales ex auto fuel (m/m%), Oct: -0.1 vs. 0.5 exp.

US: Building permits (k), Oct: 1487 vs 1450 exp.

US: Housing starts (k), Oct: 1372 vs. 1350 exp.

BN: Oil Rebounds on Expectations OPEC Will Move to Support Prices

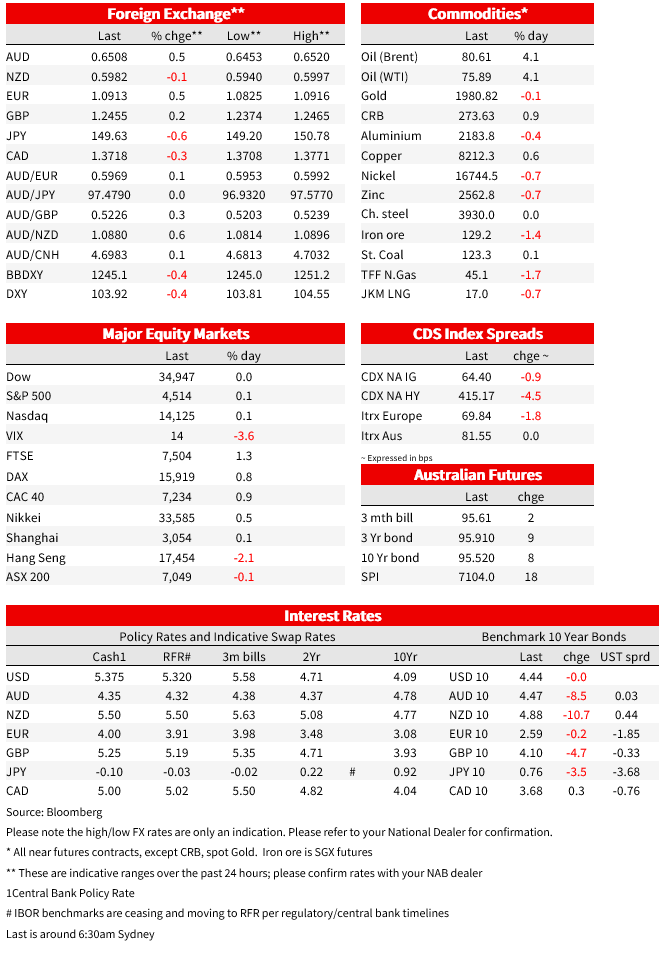

Another choppy night on bond markets with 10yr yields on net little changed and the curve twist flattening slightly. The bigger moves were in oil and the USD. Brent oil rose 4.1% to $80.61 on reports Saudi was talking of extending supply cuts along with potential cuts by others in OPEC+, reversing what seemed to be technical-driven moves on Thursday when oil fell sharply by -4.7% to below $77. The USD (DXY -0.4%) was the other big mover with broad-based based declines: EUR +0.5% to 1.0915; GBP +0.3% to 1.2462; USD/JPY -0.6% to 149.63; and AUD +0.5% to 0.6510. The move in the USD reflects the improved risk tone seen since last week’s softer-than-expected US CPI, falling bond yields, and an increasing amount of Fed rate cuts being priced. The DXY has now retraced almost 3% from the late October highs. The Japanese yen outperformed trading back below 150. The latest CFTC data revealed speculative accounts increased Yen short positioning to the highest level since April 2022.

As for yields the curve twist flattened. The US 10yr was -0.0bps to 4.44%, though it did reach a low of 4.38% before reversing alongside stronger than expected housing construction data. US building permits were 1,487k vs. 1,450k and housing starts also beat at 1,372k vs. 1,350k. 2yr yields saw a larger response to the data with 2yr yields up 4.7bps to 4.89% (low 4.79%; high 4.92%). Fed funds pricing for cuts was pared slightly with 92bps worth of cuts in 2024, down from 98.6bps of cuts on Thursday, but still very much up on the 77.3bps it was at a week ago. Even though oil prices rose, implied inflation breakevens were little changed with the 10yr breakeven -0.0bps to 2.29%. Some of the earlier drift down in yields was partly in sympathy with a soft UK retail sales report with Gilts outperforming – 10yr Gilt yields -4.7bps to 4.10% vs. 10yr German -0.2bps to 2.59%. The ECB’s Wunsch added a few ripples mid-session by saying that the ECB might have to tighten in the case of an oil shock.

Looking at UK retail sales, they did unexpectedly fall in October. Sales excluding fuel slipped 0.1% m/m against expectations for a 0.5% rise. It is unclear what the significance of this is given the consensus looked low in the light of the excessively wet weather seen during the month. The statistician indeed noted the weather effect reduced footfall, as well as the cost-of-living impact. Overall and big picture it does play to the view of a squeeze on household incomes which is helping to slow inflation – retail volumes now at the lowest levels since Covid-19 lockdowns. As in Australia, there is a lot of focus on housing debt and there are an estimated 1.6 million mortgages to be refinanced at significantly higher rates next year. Market pricing implies that the Bank of England tightening cycle is complete and the bank will begin to ease policy from the middle of 2024.

Equity markets consolidated after a week of strong gains. The S&P500 was +0.1% after having risen 2.2% on the week. Interestingly it has been the lower cap stocks that outperformed over the past week with the soft-than-expected CPI print the major driver – Russel 2000 +5.4% and the Equal-weighted S&P500 +3.2%. Positioning has been light amongst the small caps amid outperformance over the past year by large cap tech. It has been a very sharp rally over the past month with the S&P 500 is up 7.6% and Nasdaq up 9.9%.

Finally in Australia, one piece of news worth noting. The QLD government is doubling the first home buyer grant to $30k for new builds. The new grant only applies to buying or building a new home valued under $750,000, and comes into effect on Monday. Interesting the grant can be given in a range of circumstances: “You can also use it for money towards a new home, a unit, a townhouse or even if your parents want to put a granny flat out the back, so it covers the whole range of the spectrum“. The grant comes at a time when there is already evident inflationary pressures in housing construction, while most economists suggest the grant will be quickly reflected within selling prices (see ABC News: Queensland government doubles first home owner grant to $30k for new builds, including granny flats).

This week

Coming up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.