Online retail sales growth slowed in May following a fairly strong April

Insight

Lots of central bank speak from Fed, BoC, ECB and BoE today

https://soundcloud.com/user-291029717/bond-sell-off-on-hold-ahead-of-us-inflation-numbers?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

There’s a smorgasbord of central bank comments from US, Canadian, Eurozone and UK officials to consume below, during what has been a positive night for risk sentiment ahead of tonight’s all-important US CPI numbers. Main board equity indices are up over 1% everywhere in the world, Treasury yields are lower at 10-years (downward pressure aided by a strong Note auction) and the USd is slightly softer with AUD and NZD vying for top spot on the G10 scoreboard, currently up 0.5% and 0.6% respectively on Tuesday’s New York close.

Before summarising the night’s central bank speak, in what has been a Wednesday lacking major economic data beyond yesterday’s softer W-MI Australian Consumer Sentiment survey and where rising cost of living pressures and expectations for higher rates this year outweighed the easing of Omicron-related disruptions to activity, a story that caught your scribes eye last night was from Maersk, the world’s largest container shipping company responsible for almost a fifth of the world seaborne container traffic. The CEO , announcing the $1.8bn acquisition of US inland distribution firm Pilot Freight Services, said she expects supply chain bottlenecks to only last until June and gradually ease thereafter, aided by reduced demand for goods as people return to work and spend more of services like travel and entertainment. We can but hope this transpires and brings lower goods price inflation in its wake, though they’ll be scant evidence of this when the US publishes latest CPI inflation numbers tonight, where both headline and core prints are seen higher in year-on-year terms than December.

To central bank speak, and starting with the Fed, Atlanta Fed President Raphael Bostic repeated his (dot plot) forecast for three rate hikes this year but admits he’s veering towards a fourth and that while he sees the Fed moving only in 25-point increments, says the incoming data will determine ‘whether 25 basis points or 50 basis points are appropriate’. He says we’re at the cusp of seeing inflation ease and sees core PCE inflation down to 3% by the end of the year. Bostic doesn’t get an FOMC vote this year. Meanwhile Cleveland Fed president Loretta Mester, who does vote in 2022, sees inflation above 2% in both 2022 nd 2023. She says that faster rate rises and balance sheet reductions than prior cycle are appropriate and that while she doesn’t see a compelling case for a 50bps rate rise in March, doesn’t want to take anything off the table. She also notes that some FOMC members see the need for rates to get to above neutral (whether that includes herself, she doesn’t say).

North of the 49th parallel, Bank of Canada Governor Tiff Macklem says in a speech that the future path of interest rates will depend in large part on whether businesses ramp up investment, noting productivity growth is vital to non-inflationary growth, more so than ever he says with inflation currently well above the BoC’s target (here, here). Like Mester remarks about some FOMC members, Macklem notes that it’s possible ‘rates may even need to go above neutral’. He warns of the need for multiple rate increases but that the central bank is not on auto pilot, taking a decision at each (meeting) point in time.

Over in Europe, Bank of England chief economist Huw Pill (do love that name), considered to be on the dovish side of the MPC spectrum, says he worries about taking unusually large steps on policy, seeing smaller rises as restraining market bets on (policy) activism, but that he wouldn’t rule out bigger rises in all circumstances. On the BoE’s balance sheet, he says that a 1% Bank Rate is not an automatic trigger for the active sell-down of bonds acquired through the QE programme.

Finally on the European continent, ECB Governing Council Isabel Schnabel continue to mark herself out as one of the more hawkish members. While being non-committal on her policy preferences, she says that while she sees inflation moving (back) towards 2% in the medium term, policy optionality is more important than ever. While needing to minimise the risks of both acting too late and acting too early, she notes that besides supply shocks, the ECB has to assess the strong developments in the labour market and their implications for medium term inflation. The March ECB meeting is building to be as – or quite possibly more – important for markets than the Fed. The ECB is on March 10, the FOMC decision six days later.

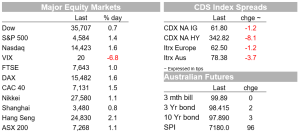

In markets, US equities have come into the last hour of NYSE trade stronger, the tech. sector leading the way (led by a rebound for Facebook – sorry Meta – of more than 5%). The NASDAQ is currently up almost 2% and the S&P500 1.4%. This follow a good day for European stocks (Eurostoxx 0 +1.8%) in turn following good showing on APAC bourses stocks where indices finished the day up by between 1% and 2%.

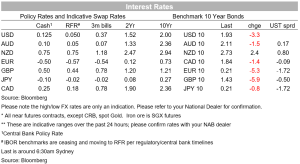

Helping US stock markets sentiment has been a pull back in 10-year US treasury yields, already off their 1.97% Tuesday high in front of the 10-year Note auction, which cleared 2.3bps through its pre-auction yield. It’s currently at 1.92bp, down 4bp on the night (having been as low as 1.91%). Front-end yields haven’t ceded ground though, 2s currently little changed at 1.344%. European yields also fell back, with 10-year Bunds and Gilts both down 5bps and Italy by 10bps.

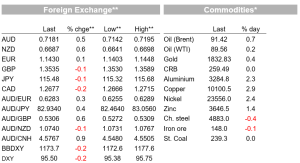

In FX, the slight pull back in US longer end yields and positive risk sentient has seen the USD slipping, DXY -0.15% with EUR/USD up by the same amount. NZD and AUD have fared best among major currencies in the past 24 hours, currently +0.6% to 0.6690 and 0.5% to 0.7185 respectively.

Finally all hard commodities are in the green, who copper, aluminium and nickel all up over 25, while oil is a touch firmer, Brent crude up 58 cents at $91.35 a barrel.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.