On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

US equities start the new week in a positive mood, the USD has remained under pressure and after initially edging higher, longer dated UST yields edge lower supported by a well-received 20y Bond auction.

Nothing to note.

US equities start the new week in a positive mood, and after initially edging higher, longer dated UST yields edge lower supported by a well-received 20y Bond auction. The USD has remained under pressure, softer across the board with NZD and AUD consolidating gains seen during our APAC session yesterday. Oil prices are up again and so too iron ore.

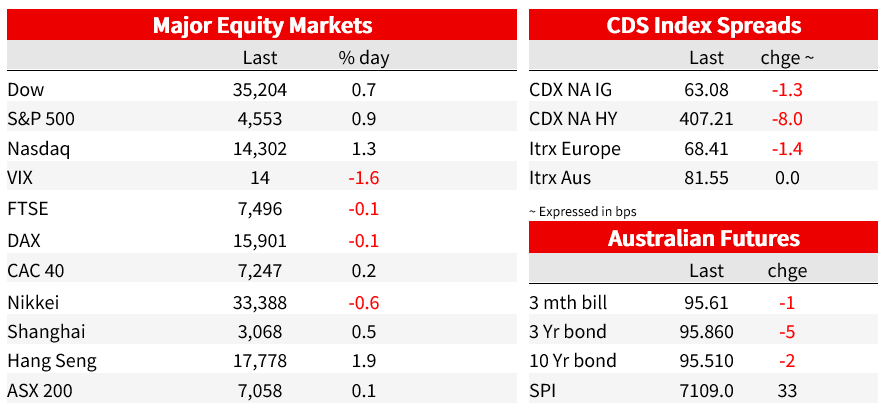

US equities have started the new week with a spring in their step with the S&P 500 edging towards its highest level since August . As I type the index is +0.83% with the IT sector leading the gains, up 1.38% while Utilities is the only sector in the red, down 0.31%. Meanwhile the tech-heavy Nasdaq 100 was on pace for a 22-month high, up 1.2%. In company news Microsoft rallied to a record while Nvidia climbed in the run-up to its earnings. Earlier in Europe, the Eurostoxx 600 closed 0.10% and yesterday the Nikkei reached a 33-year intra-day high before closing down 0.6%. Japanese stocks have advanced almost 30% this year, underpinned by strong company results, a weak Yen and progress on corporate governance.

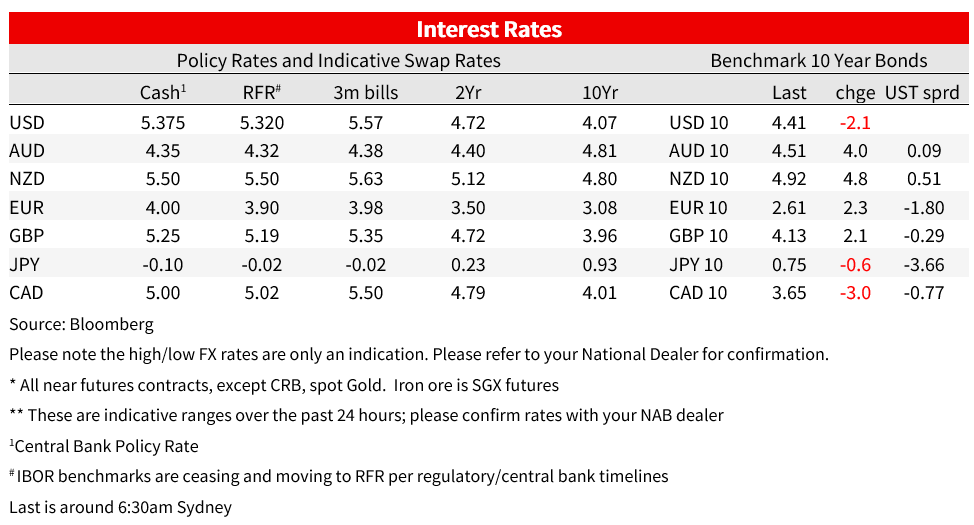

Longer dated UST yields initially traded higher, but a well-received 20y bond auction triggered a reversed in course with longer dated yields ending the day down around 2bps . The 10y Note eased 2bps to 4.42% while the 30y Bond declined 2.5% to 4.56%. After soft demand recorded in the previous 30y Bond auction, the solid result for the 20y Bond auction alleviated concerns over a lack of appetite for debt during a holiday-shortened week (the auction drew yields of 4.78%, compared with the pre-sale level of 4.79%). Earlier in the session, European bond yields moved higher with yields on 10-year bunds up 3bps to 2.62%. Italian bonds outperformed following Moody’s decision to revise its outlook to stable from negative. The spread between 10-year Italian BTPs and German bunds has tightened from 208bps to 173bps since mid-October amid improved risk sentiment.

Sticking with Europe, Bloomberg notes that Germany is exploring a drastic overhaul of its federal budget for this year , including relaxing restrictions on net new debt, following last week’s ruling by the country’s top court. Governing Council member Wunsch said in a Bloomberg interview that the ECB may have to raise borrowing costs again if the markets pricing for easier policy undermines the bank’s policy stance. Wunch, a known hawk, expressed concern that the current easing in financial conditions might make policy too easy. This as markets have removed any last vestiges of hikes in the last couple weeks to price cuts through 2024.

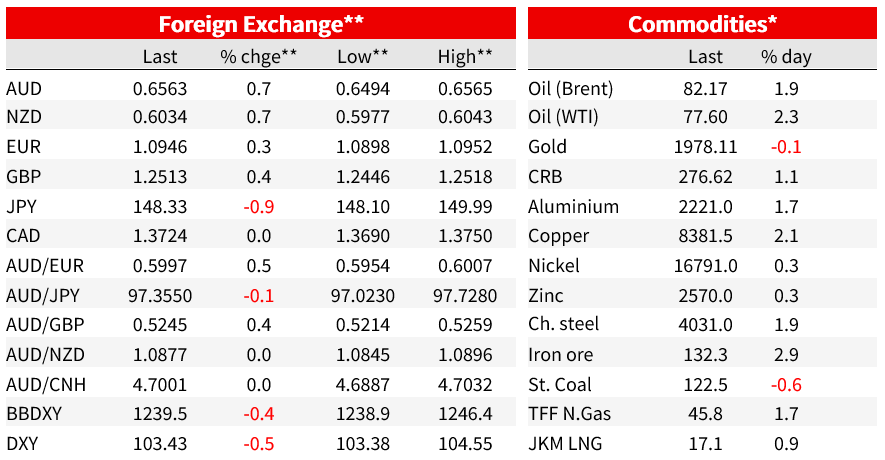

The USD extended its recent decline, falling for the sixth day in the past seven. Both the DXY and BBDXY are down 0.4% over the past 24 hours with much of the decline recorded during our APAC session yesterday. CNY/CNH started the new week in a positive mood supported by a stronger than expected PBoC fix. Yesterday USD/CNH fell from 7.22 to 7.1648 with the pair closing at its lows. Overnight, Bloomberg reported Chinese regulators are drafting a list of 50 developers eligible for a range of financing. The list, which includes both private and state-owned developers, is intended to guide financial institutions as they weigh support for the industry via bank loans, debt and equity financing. After dismal property figures in October showing decline in prices and sales, Beijing has been on a new drive to support the sector with some positive signs seen in the performance of some property shares, as well as iron ore (up another 2.9% to $132.2). The currency (CNH and CNY) is now showing some impetus too with USD/CNH break below 7.20, suggesting the pair now has room to head towards 7.11 over coming days.

Other Asian currencies also made inroads against the USD with JPY a top G10 performer over the past 24 hours . JPY is up 0.8% with USD/JPY starting the new day at ¥148.31, the currency usually shows a great deal of sensitivity to movements in 10y UST yields, but recent dovish comments from the BoJ have hindered its ability to perform, notwithstanding a backdrop of lower UST yields. The 10y US-JN sovereign spread suggests USD/JPY should trade closer to ¥147 rather than ¥150, but now it seems the currency is taking notice.

Yesterday’s CNH appreciation and consolidation during the overnight session boosted both the AUD and NZD . Yesterday, as CNH was heading towards 7.16, the AUD made a swift move from around 0.6512 to above 0.6550 and then overnight edged a little bit higher again to start the new day at 0.6563. Positive risk sentiment, higher energy and iron ore prices and a broadly weaker USD are all favourable tailwinds for the AUD. NZD starts the new day above 0.60, yesterday’s NZD move higher lost momentum ahead of technical resistance in the 0.6055/60 region which has corresponded with the highs on several occasions over the past 8 weeks. A break above this level would confirm an evolving higher trading range.

Lastly and as noted above, oil prices have continued to rally. Brent crude prices increased 2.8% and are now back above $82 per barrel. Opec+ is expected to consider extending production cuts when they meet in Vienna on Sunday . In addition to iron ore, copper and aluminium also had a Monday, up 1.9% and 1.8% respectively.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.