Total spending grew 0.9% in June.

The standout data point overnight was US Retail Sales, which came in well above consensus expectations.

https://soundcloud.com/user-291029717/oil-rising-whilst-putin-sits-tight?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

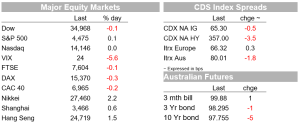

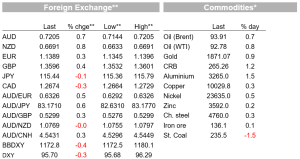

If yesterday’s US and global equity market gains were largely a function of a point for diplomacy on the Russia-Ukraine situation and claims by Russia that it was withdrawing some troops from the Ukraine border following completion of military exercises, the renewed weakening in stocks overnight is linked to claims from NATO’s secretary general that there is no sign of de-escalation by Russian forces on the ground near Ukraine . Weaker risk sentiment hasn’t though offered any support for the USD, currently -0.3% with AUD and NZD the best two performing G10 currencies in the last 24 hours (+0.7). US front-end yields were lower ahead of FOMC Minutes (2-year Treasuries -4bps but 10s +1.5bps) but yields are a tad lower out of the Minutes. The money market had earlier pared back Fed Funds pricing for the March 10 FOMC meeting to 39bps from 41bps this time yesterday. It’s now 37.5bps. The Fed’s Harker and Kashkari have been out aligning themselves with just a 25bps hike next month.

NATO secretary-general Jens Stoltenberg’s assertion that there is no sign of de-escalation by Russian forces on the ground near Ukraine has been accompanied by a warning that the threat from Russia had become a “new normal” in European security (adding that NATO was considering setting up new battle groups in central and SE Europe). If this is indeed the case, it is entirely consistent with one of the take-away (for this scribe at least from a webinar NAB hosted with a leading Australian geopolitical expert yesterday, that Russia’s best interest were likely to be served by “keeping the temperature high”. Those in markets hoping for an early resolution of the Russia-Ukraine situation are prone to be disappointed.

To economic news, and the standout data point overnight was US Retail Sales , which came in well above consensus expectations (headline 3.8% against 2.0% expected, ex-autos 3.3% versus 1.0% expected and core ‘Control Group’ measure a stonking 4.8% (consensus 1.3%). Coming amid the weakest (University of Michigan) Consumer Sentiment reading since March 2009, the expression ‘what watch they do not what they say’ rings particularly true. Certainly the Omicron wave which the US was in the midst of last month, held no fear for consumers. That said, we need to recognise the difficulty statisticians are having seasonally adjusting sales data these days, with traditionally strong December sales pulled forward into November and January benefiting more than it has historically from start of year sales. So January strength need not be seen at least partly in this context, and to the fact US household are still very cashed up from Pandemic relief payments as yet unspent. It nevertheless points, according to our friends at Pantheon Economics, to consumer spending in the order of 5% in Q1 on data to data, and GDP growth in the order of 4%.

Elsewhere on the data front, US industrial production at 1.4% was boosted by the cold weather and a related boost to utility output, with manufacturing output up a much more subdued 0.2% (as expected). The NAHB Housing market Index was unchanged at 82.0, also as expected.

Minutes of the January FOMC meeting released an hour or so ago show Fed officials expect to raise the Fed Funds rate more aggressively than when they last did so between 2015 and 2019, saying “Most participants thought a faster pace of increases… would likely be warranted” compared to the prior tightening cycle due to higher inflation, a strong labor market and stronger growth prospects. The Minutes don’t, however, appear to give an obvious succour to the idea of the Fed kicking off the tightening cycle with a 50-point move (though to be fair this had only really come on to the radar since the January 26 meeting).

In this respect, Philadelphia Federal Reserve President Patrick Harker has been out saying “I am very supportive of starting a process of raising the Fed funds rate, which is our primary tool of monetary policy, starting to raise that, and I would support as early as March a 25 basis point increase in that rate,” Harker said, in an interview with the WHYY radio station program “Radio Times.” Minneapolis Fed President Neel Kashkari has also been out, saying that “If we raise rates really aggressively, we run the risk of slamming the brakes on the economy, putting the economy in recession….my caution to my colleagues and myself is let’s not overdo it.” Neither Harker nor Kashkari are FOMC voters this year.

Also to note on the central bank front, Bank of Canada Deputy Governor Tim Lane said the central bank is “alert” to the possibility that inflation could prove to be more sticky than forecast, and policy makers are prepared to adapt their policies if needed. In a speech, Lane highlighted the importance of agility in decision making, citing how the central bank adjusted policy during its pandemic response as inflation came in faster than expected. Bank of Canada meets March 3 with money markets currently priced for 31bps of tightening.

To markets and US stocks have been busily paring losses in the hour since this note began, the S&P putting on a full 1% (with an hour of trade still to go) and meaning the index is flat on the day as I type as too, roughly, is the NASDAQ. The rally dates exactly to the release of the FOMC minutes, but if that is because they don’t instil greater fear of the Fed kicking off the tightening cycle with a 50-point rate rise, then as noted above events since then, including yet more upside surprises on CPI and PPI inflation prints, render them somewhat redundant.

In bonds, prior to the Minutes, we had seen a ‘twist’ in the US yield curve with 2s some 4.5bps lower but 10s +1.5bos. This has since shifted to a classic bull steepening with 2s -5bps and 10s now flat on the day. Prior to the FOMC Minuets, money market had pared back their pricing for the March 16 FOMC outcome to 39bps of tightening from 41bp, and this has further reduced to 37.5bps since the Minutes. Earlier Wednesday, European bonds were 3-5bps lower at 10 years.

In FX, the USD was about 0.2% lower in DXY terms relative to Tuesday’s New York close, but is currently -0.3%. AUD and NZD are the best two performing G10 currencies, currently both 0.7%, with AUD/USD poking its nose above 0.72 (high of 0.7204) and NZD/USD to just shy of 0.67 (high of 0.6691). When AUD was last above 0.72 a week ago, the air proved to be very thin, so we do need to be a little cautious in extrapolating this latest move up. And finally in commodities, oil has recouped a little of Tuesday’s sharp losses (latter on the seemingly positive Russia news re troop withdrawals), Brent and WTI currently both up a little under 1%.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.