Firmer consumer and steady outlook

Insight

After what has been a solid month for equities and bond investors, month end flows have probably play their part in the price action overnight, US equities have lost momentum, UST have led a rise in core global bond yields and the USD is stronger. US and European inflation releases favoured the notion the Fed and ECB are done with their respective tightening cycles.

Events round-up

NZ: Dwelling consents (m/m%), Oct: 8.7 vs. -4.6% prev.

NZ: ANZ activity outlook (net%), Nov: 26.3 vs. 23.1

CH: Manufacturing PMI, Nov: 49.4 vs. 49.8 exp.

CH: Non-manufacturing PMI, Nov: 50.2 vs. 50.9 exp.

GE: Unemployment rate (%), Nov: X.X vs. 5.8 exp.

EC: CPI (y/y%), Nov: 2.4 vs. 2.7 exp.

EC: CPI core (y/y%), Nov: 3.6 vs. 3.9 exp.

EC: Unemployment rate (%), Oct: 6.5 vs. 6.5 exp.

CA: GDP (ann’lsd q/q%), Q3: -1.1 vs. 0.1 exp.

US: Initial Jobless Claims, 25-Nov: 218 vs. 218 exp.

US: Personal income (m/m%), Oct: 0.2 vs. 0.2 exp.

US: Real personal spending (m/m%), Oct: 0.2 vs. 0.1 exp.

US: PCE core deflator (m/m%), Oct: 0.2 vs. 0.2 exp.

US: PCE core deflator (y/y%), Oct: 3.5 vs. 3.5 exp.

US: Chicago PMI, Nov: 55.8 vs. 46 exp.

US: Pending home sales (m/m%), Oct: -1.5 vs. -2.0 exp.

Good Morning

The cool out – The Clash

Overnight US and European inflation data releases favoured the notion the Fed and ECB are done with their respective tightening cycles. After what has been a very solid month for equities and bond investors, month end flows have probably play their part in the price action overnight, US equities have lost momentum while UST yields have led a rise in core global bond yields. The USD is a tad stronger on the day (and well down on the month) with EU FX the notable underperformer. OPEC+ agreed cut in supply but message is unconvincing, leading toa decline in oil prices.

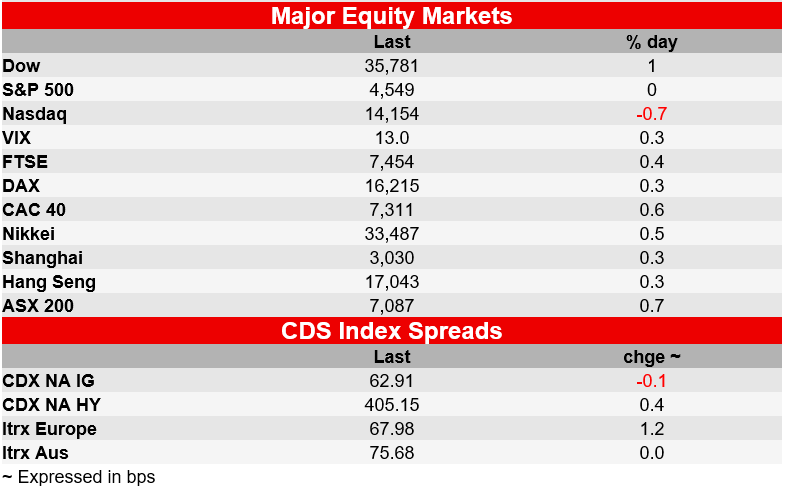

US equities look set to end the last day of November with negative returns, as I type the S&P 500 is down 0.1% and the NASDAQ is -0.79%. The mild sense of risk aversion needs to be put in context in what has been an impressive month for US equity investors, the NASDAQ should end the month up over 10% while the S&P 500 should end the month up over 8%. Thus, taking some chips of the table on the last day of the month would make sense for many, specially for pension funds and long-term investors looking to rebalance their portfolios. European equities closed the month on a positive tone with the EuroStoxx 600 +0.55% while all main regional indices also closed higher. On the month the EuroStoxx 600 gained 6.45%.

It was a busy night of economic data releases, but the main take away was that both US and European inflation are cooling and heading in the desired direction for their respective central banks. In the US, the October core PCE deflator rose only 0.17%mom, pushing the year-over-year rate down to 3.5%, from 3.7% in September. To put these numbers into perspective, back in July the Core PCE was 4.3%, so the decline in recent months has been quite impressive with the 3-month annualised rate now ticking at just 2.2%. Details in the report were also encouraging, the y/y rate for core goods was just 0.3%, down from 4.6% in October last year and given the Fed focus/concern over services inflation, the report also had good news here with core services ex rent (one of the Fed’s in vogue measures) rising just 0.15% taking the yoy rate to 3.9%, its lowest print since March 2021.

Of note too, the US personal income and spending report also revealed a pull back in US consumption, consistent with the idea that the cumulative effect of Fed tightening is finally starting to bite. Real personal spending slowed from a 0.3% increase in September to just 0.2% in October, in line with consensus. But expanding the number to two decimal places, the increase in October spending was just 0.17%, that is substantially lower than the 0.3% average month-to-month increase in the third quarter.

Meanwhile, Eurozone CPI fell to 2.4% y/y in November, which was below 2.7% pencilled in by consensus, this was the slowest annual pace since July 2021. The softer print was well flagged following below consensus readings across the larger European economies. The drop in inflation has prompted investors to bring forward pricing of rate cuts by the European Central Bank. The market is now pricing a 25bps rate cut by April next year.

Looking at other data releases, US jobless claims increased to 218k for the week ending Nov. 25, from 211k a week earlier. That matched the consensus estimate, but the biggest surprise was the surge in continuing claims, which rose 86k. to 1927k. Suggesting the US labour market is showing signs of cooling.

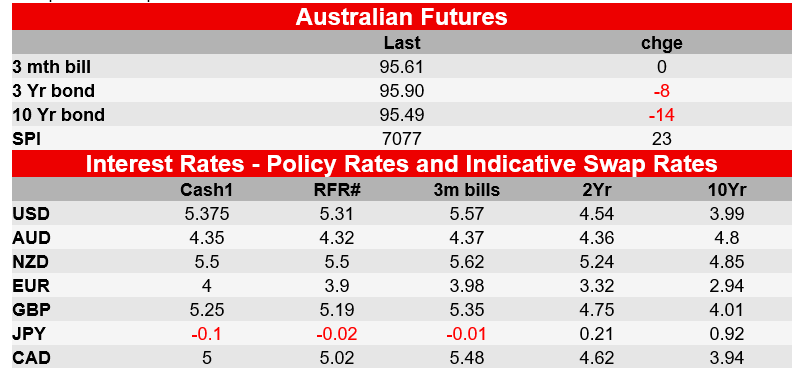

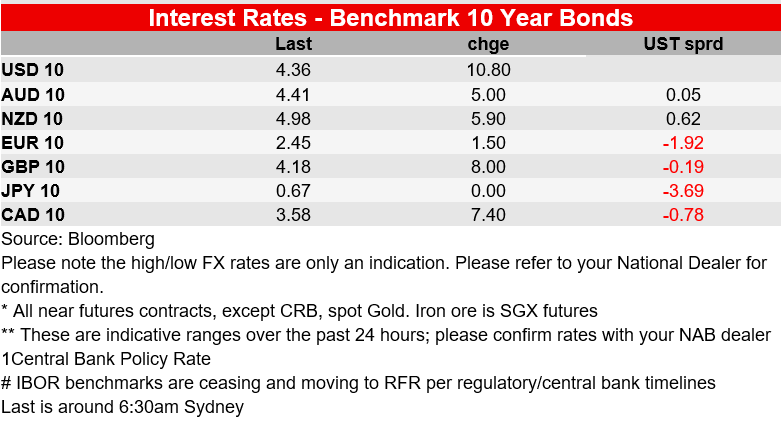

US Treasury yields ticked up overnight, almost in parallel fashion with yield up between 6 and 8bps across the curve. European yields were also higher, although Bunds (thanks to the softer EZ CPI) lagged the move, 10y Bunds up 1.5bps to 2.444% while 10y UK Gilts were 10bps to 4.169%. While month end may have played a part on the move up in UST yields, guarded comments on falling inflation (and thus rate cuts) from several Fed officials, also played their part. San Francisco Fed President Daly said policy is in “a very good place” but, “I’m not thinking about rate cuts at all right now.” NY Fed President Williams said that even with policy at the most restrictive in 25 years staying there is appropriate and “additional policy firming may be needed.” Across the pond BoE MPC member Greene said the risk on rates is still not doing enough.

The market now prices about 125bp of cuts for the Fed by the end of next year. Fed Chair Powell gets to add his voice to the debate via some speaking engagements tonight.

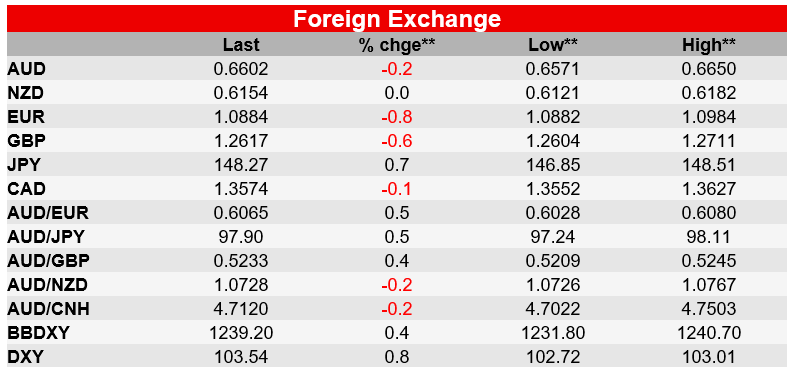

Moving onto FX, the USD is a tad stronger across the board with notable underperformance by European currencies. The DXY and BBDXY indices are up, 0.66% and 0.4% over the past 24 hours, but look set to end the month down close to 3%. After briefly trading above 1.10, the euro is back below 1.09, now trading at 1.0884 with the move lower gaining momentum following the soft European inflation data.

The AUD/USD is down just 0.18% to 0.6603, this after trading down to an overnight low of 0.6571. Overall November has been a good month for the Aussie, up over 4% and close to the top of the G10 leader board. NZD/USD also had choppy price action in offshore trade and is marginally weaker against the US dollar. The Kiwi traded to an overnight low of 0.6120 and now start the new day at 0.6154.

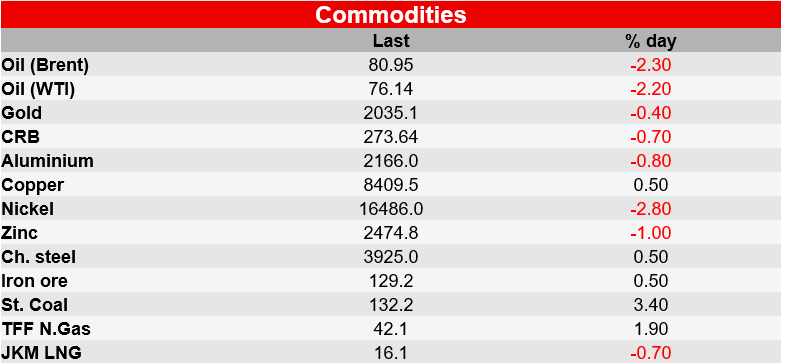

On other news, OPEC+ agreed a new oil supply cutback of 1mb/d, yet crude prices fell (WTI -2.2% and Brent -0.3%) amid a lack of clarity about how these cuts will be implemented. Bloomberg noted that the absence of a comprehensive breakdown combined with the “voluntary” nature of the cuts left market watchers unconvinced.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.