Online retail sales growth slowed in May following a fairly strong April

Insight

Geopolitical tension lifted overnight with President Putin formally recognising the two Ukrainian breakaway regions of Donetsk and Luhansk and signing aid and cooperation agreements.

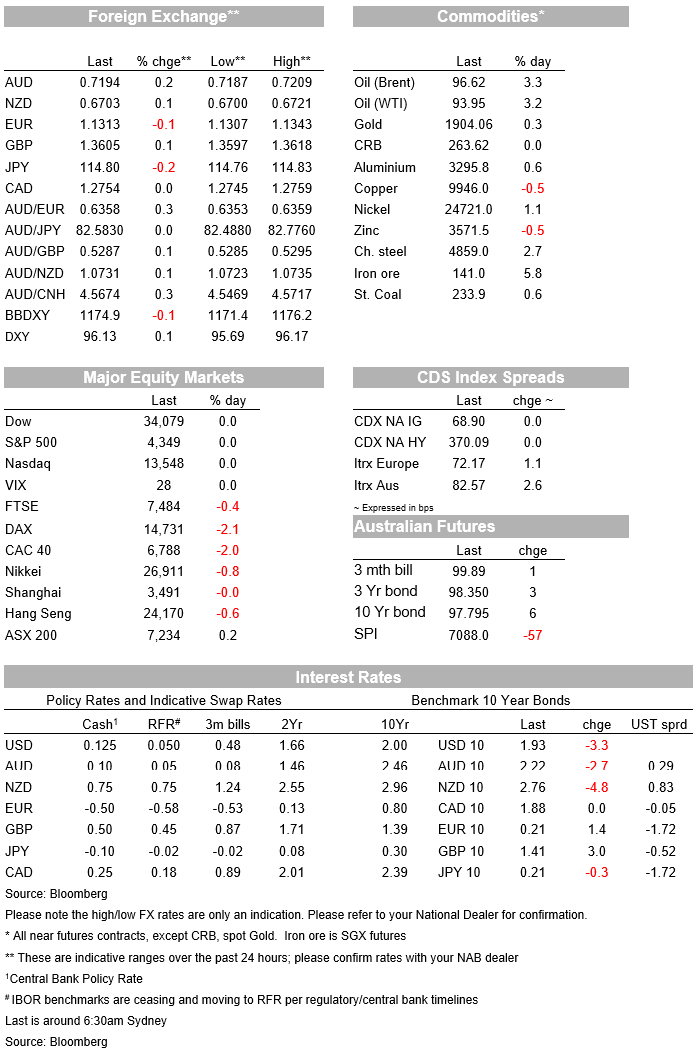

Geopolitical tension lifted overnight with President Putin formally recognising the two Ukrainian breakaway regions of Donetsk and Luhansk and signing aid and cooperation agreements. The real fear now is the leaders of the two breakaway regions formally invite Russian troops onto the ground in the disputed regions. Risk sentiment has soured, but the public holiday in the US has likely limited what would have been a sharper market reaction. European stocks were lower prior to the headline of Putin recognising the regions with the Eurostoxx 50 -2.2% and more importantly EuroStoxx futures are -3.8%. S&P500 futures closed before the above headline and were -1.2%. US Treasury futures imply a 1-2bp move lower in the US 10yr yield which yesterday was at 1.93%. The bigger reaction has been in commodities with Brent Oil +3.3% to $96.62. FX has given up the moves it had in Asia yesterday with EUR ‑0.1% after having been up some 0.6% and currently trades at 1.1309. Risk havens have appreciated with USD/Yen -0.3% to 114.77 and USD/CHF -0.6% to 0.9159. The AUD (+0.2%) and NZD (+0.0%) have been remarkably resilient – commodity prices a likely factor.

The proposed Biden-Putin summit which provided some relief to risk sentiment in Asia yesterday evaporated overnight with Russian authorities stating early on Monday that there were no concrete plans for such a summit. Risk sentiment soured pretty quickly as the news broke early overnight with several other incidents also weighing, including: (1) the Russian military reporting it had destroyed two Ukrainian armoured vehicles and killed five Ukrainian personnel inside Russian territory, while and Ukrainian authorities denied the allegations; and (2) the leader of the breakaway Donbas region asserting (without evidence) that Ukraine had launched an offensive and would be welcome to financial and military assistance from Moscow. President Putin also foreshadowed a decision on whether to recognise the two breakaway regions. In the past hour President Putin has formally recognised the two breakaway regions and has also signed aid and cooperation pacts. The developments make the Donbas region a potential powder keg.

Front and centre of fears is the real potential that the two regions invite Russian military forces to protect them against Ukraine (similar to what was seen in the two Georgian breakaway regions of Abkhazia and South Ossetia). The US Secretary of State has previously said that formal recognition of the region by Russia “ would further undermine Ukraine’s sovereignty and territorial integrity, constitute a gross violation of international law, [and] call into further question Russia’s stated commitment to continue to engage in diplomacy to achieve a peaceful resolution of this crisis” and importantly would necessitate a “swift and firm” response from the US and its allies. We are none the wiser of what such a response that would be, and whether formal recognition of Donetsk and Luhansk could be the fuse that sees a wider Russian incursion into Ukraine. Russian equities have fallen sharply with MOMEX -10.9% and USD/RUB is +2.9% to 79.58.

Economic data has taken a backseat to geopolitical developments. The most notable piece was the Markit PMIs for the Eurozone which surprised to the upside for the services sector at 55.8 (52.1 expected), while manufacturing activity was broadly as expected at 58.4 (58.7 expected). Importantly, the PMIs continue to sound alarm bells over the inflation picture with the Markit write-up noting; “Average prices charged for goods and services rose at the sharpest rate yet recorded by the survey as firms increasingly sought to pass persistent higher cost inflation on to customers. A record high rate of inflation in the service sector was accompanied by a near-record rate in manufacturing”. In terms of activity, the overall composite index was hit a five month high, illustrating that activity has rebounded sharply after the Omicron peak and governments have started to ease restrictions. (see Markit PMI press release for details).

Even with the US holiday there was still some Fed speak with Governor Bowman noting she remained opened to a 50bp hike in March – “I, as all of my colleagues will as well, will be watching the data closely to judge the appropriate size of an increase at the March meeting”. On inflation, Bowman said she expected current levels of “uncomfortably high inflation ” will persist through the middle of this year and that there was a substantial risk that high inflation would continue beyond that. Markets have pared pricing for a 50bp hike in March to a 24% chance after several Fed speakers on Friday seemingly backed a more gradual 25bp approach. Bowman’s views along with Bullard’s last week, suggests that if the Fed lifts by 25bps in March, there will be a few formal dissenters who wanted 50bps – an echo of the BoE’s most recent meeting.

Coming up today:

Fairly quiet domestically with only RBA Assistant Governor Kent speaking on the RBA’s open market operations. Offshore it is relatively quiet with the German IFO and the US’ Markit PMIs the most notable. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.