Online retail sales growth slowed in May following a fairly strong April

Insight

Risk sentiment craters (S&P500 -1.3%) as the Russia/Ukraine situation has no sign of ending

Risk sentiment dived overnight with no clear catalyst. Financial news media pointed to satellite imagery of a 65km line of Russian military vehicles advancing on Kyiv, while the previously announced NATO response force to eastern-NATO countries was enacted with French troops now stationed in Romania (NATO Secretary General Stoltenberg reinforced “our commitment to Article 5, our collective defence clause, is iron-clad” ). Instead it appears the stress seen in money markets on Friday is flowing through to bond markets, as well as a sharp paring back of central bank hike expectations. A squeeze for collateral is also evident given the high proportion of EUR in Russia’s FX reserves that are now unusable due to sanctions. Some money market stress is there (but is not extreme) with US FRA/OIS 1m is at 19.4bps, its highest since September 2020. Central banks so far do not appear to be overly concerned with the US Financial Stability Oversight Council (headed by Treasury Secretary Yellen) noting the US financial system was functioning “in a normal manner ” and they would continue to monitor the situation. If stress did emerge stemming from Europe trying to accessing dollars then standing US dollar swap lines could be activated.

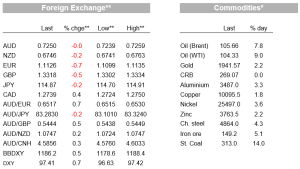

One uncertainty is the unknown to which Russia was a source of US dollars to markets with that provision obviously hampered by sanctions. Global companies and countries are either disassociating themselves from Russian companies voluntarily, or being prevented from trading due to sanctions, including for oil which is putting stress on oil markets. Brent oil rose 7.8% to $105.66 with reports Russia is offering oil at a $15 discount to Brent. The WSJ notes key European financers to commodity trade houses have already begun curbing financing for commodities, as are Chinese banks. One Indian oil buyer has also said while it was willing to buy Russian oil, it wanted Russia to take responsibility for transporting the oil because some shipping companies are hesitant to load Russian crude (see WSJ: Russia Scrambles to Maintain Oil Sales, Lifeblood of Economy ). In this vein the IEA agreed on Tuesday to release 60 million barrels of oil from global reserves, but realistically this isn’t going to do much given it is equivalent to around 12 days of Russia’s exports. Another factor adding to a tight crude market is OPEC itself producing below targeted levels for various reasons.

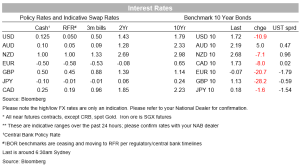

The sharp turn in risk sentiment is evident in the bond market with a massive rally in global rates . Benchmark 10-year yields have fallen in the order of 20-30bps across Europe (France -24bps, Germany -21bps and UK -28bps). This puts German’s 10-year rate back into negative territory. This has spilled over into US Treasuries, with 2 and 10-year rates down in the order of 11-12bps, the 10-year rate falling below 1.7% at one stage and currently trades at 1.72%. Central bank pricing has also been pared sharply given some stress in money markets and the likelihood of higher commodity prices weighing on demand. Markets now price hikes from the US Fed at 4.7 hikes for 2022 from 6.3 last week. Notably a March rate hike is now 92% priced for a 25bps move, compared to a 40% chance of a 50bps move last week. Pricing for the BoE has also fallen to 4.1 more hikes in 2022 compared to 5.6 last week. BoC which meets tonight has a hike 79% priced

Meanwhile closer to home similar themes are playing out with RBA pricing now at 4 hikes in 2022 from 4.7 last week . Yesterday’s RBA meeting gave no hint of an earlier move. Unsurprisingly, Russia’s war in Ukraine is a major source of new uncertainty. As was the case last month, the view remained that the pick-up in wages was likely to be gradual, meaning the RBA has time to be patient to assess how the various factors affecting inflation evolve. That said we think it’s important that the final paragraph now refers to growth in labour costs being at a rate consistent with inflation sustainably at target, rather than just wages being consistent with target. To us, this pivot creates optionality for a somewhat higher interpretation of wages pressures than the WPI is currently suggesting (the WPI excludes superannuation and other bonus payments and measures a constant sample of jobs so doesn’t fully capture higher earnings from newly created positions or higher labour market churn) should inflation persist at higher levels than the RBA is expecting/or broaden and/or supply-side pressures prove more intractable. These are live risks in the next 1-2 quarters but may resolve in the back half of the year.

As for FX, European currencies remain under pressure. EUR fell below 1.11 for the first time in nearly two years and GBP is down to just over 1.33. Those two were the major drivers of USD strength with he DXY up +0.8% overnight. SEK and NOK are also weak, but the other majors are all well contained, plus or minus 0.3% against the USD in overnight trading and over the past 24 hours. The AUD made a charge towards 0.73 last night, but is back to around 0.7250.

Economic data of course remains a sideshow to the market’s focus on Ukraine developments. For the record. The US Manufacturing ISM was 58.6 against 58.0 expected. There was no further easing of supply side pressures in this survey. New Orders rose, the Prices Paid Index remained elevated, and Supplier Deliveries which measures slower deliveries rose. The German CPI data showed a small upside surprise, with the headline rate rising 5.5% y/y against 5.4% expected. Canada GDP in Q4 was strong and at 6.7% annualised was better than the sub-6 reading assumed by the Bank of Canada, thereby supporting a rate hike tonight. China PMI data unexpectedly showed a lift for the manufacturing and non-manufacturing indices, possibly supported by the government’s easing measures, although the level of the indices remain consistent with sluggish growth by China’s standards.

Q4 GDP figures dominate domestically Offshore focus will remain on Russia/Ukraine and on Fed Chair Powell who is speaking to the House. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.