Online retail sales growth slowed in May following a fairly strong April

Insight

EU considering further measures against Russia overnight which would allow them to impose tariffs and quotas to Russian exports, further disrupting global trade.

https://soundcloud.com/user-291029717/powell-putin-and-prices?utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Risk sentiment remains fragile and is very much being swung around by Russia/Ukraine headlines as well by central banks who seem committed to hiking rates, and who are also noting upside risks to inflation. The main headline overnight was the EU considering further measures against Russia, floating the removal of ‘most favoured nation’ trading status. Such a move would allow the EU to impose tariffs and quotas to Russian exports, further disrupting global trade. Meanwhile there does not appear to be any let-up in tensions with French President Macron believing “the worst is to come” in Ukraine after what was reportedly a 90-minute phone call with Putin. Chair Powell gave his Senate Testimony overnight, re-iterating the Fed’s normalisation plans and giving the first hint that the Fed believes it is behind the curve (see below for more details). The most notable moves for an Australian audience has been the AUD which reached its highest level since November 2021 at 0.7348 and currently trades at 0.7326 (+0.5% over the past 24 hours). In the words of Midnight Oil, the AUD was the King of the Mountain overnight.

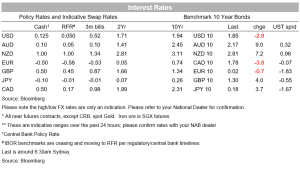

Equities were mixed overnight. Losses were concentrated in Europe with the Eurostoxx50 ‑2.1%, while the S&P500 is currently in the red in its last hour of power and is down -0.7%. Benchmark yields are slightly lower with US 10yr yields -2.9bps to 1.85%. It is worth noting that the moves in nominal yields contrasts will the fall in TIP yields (currently -0.88%) over the past few days with 10yr implied breakevens now at 2.73% compared to 2.47% the day before Russia invaded Ukraine. EURUSD cross currency basis swaps (EUXOQQ1) have eased a little at -25.6bps from -34.6, but there is still a shortage of collateral in Europe . The German 10yr asset swap spread (ASWABUND) is at 73.3bps, its highest since the Eurozone crisis in 2011. The German DMO noted overnight that sanctions were creating a scarcity of certain bonds with repo rates on some bonds reportedly trading as low as ‑5%, implying counterparties were willing to lend cash at deeply negative interest rates to borrow hard-to-find bonds. The German DMO said it would increase the volume of a 2024 maturity bond by €8.5b.

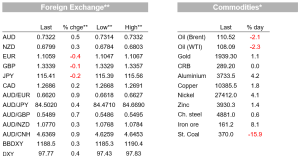

FX markets has seen EUR hit a fresh 18-month low at 1.1034 and is currently down -0.4% at 1.1057. Weighing on the EUR are the likely impact of spillovers to the European economy and the ECB from Russia/Ukraine and also from the energy price shock. The ECB may be the odd one out in terms of central banks reacting to higher inflationary pressures stemming from higher commodity prices, given its greater real activity exposure to Ukraine and Russia, as well as its exposure to Russian gas. ECB officials have been briefing of the need to keep the APP going for longer and pushing out rate hikes into 2023. In contrast, for the US Fed markets are pricing in 5.9 rate hikes for 2022 and fully price a 25bp move at the March meeting. The overall USD DXY is up 0.4% with the driver being the weak EUR (-0.4%) and also a fall in GBP (-0.1% to 1.3345). The AUD is contrast is at its highest level since November 2021 and currently trades at 0.7324. Higher commodity prices the obvious driver. The NZD was also higher overnight by 0.2% to 0.6794.

Powell’s Senate Testimony had the first acknowledgment that the Fed is behind the curve. Chair Powell said the Fed “would have engaged our tools earlier ” if it had realized that the supply-chain pressures would be longer lasting than they anticipated. The Fed will be watching inflation expectations closely in the context of higher commodity prices with Chair Powell noting: “There’s already a lot of upward inflation pressure and additional pressure does probably raise the risk that inflation expectations will start to react in a way that is negative for controlling inflation”. The rest of the Testimony followed yesterday’s House one closer, with Powell noting: “Before the invasion we were planning to make a series of interest rate increases, that is still the case”. The Fed’s Mester (voter, hawk) speaking separately also noted the Ukraine situation “ In fact, it actually adds upside risk that high inflation might continue, and that makes it more important to take action”. Mester also played to the view of the Fed front-loading hikes and then seeing how growth is impacted by Ukraine in the second half of the year.

How far is the Fed being the curve? Very if you read a WSJ piece by Fed watcher Derby. The Cleveland Fed’s Taylor Rules suggests the Fed Funds rate should already be at 3.2% (see WSJ: Derby’s Take: Monetary Policy Rules Point to Fed Being Way Behind the Curve ). Your scribe wrote extensively on these Taylor Rules recently and noted that former-Fed Vice-Chair Clarida who helped design the Fed’s average inflation targeting framework said once lift off occurs “consistent with our new framework, the relevant policy rule benchmark I will consult…is an inertial Taylor-type rule with a coefficient of zero on the unemployment gap, a coefficient of 1.5 on the gap between core PCE inflation and the 2 percent longer-run goal, and a neutral real policy rate equal to my SEP projection of long-run r*”. According to the Cleveland Fed, the inertial rules are consistent with a Fed Funds Rate already being at 1-1.6% (see NAB: Inflation indicators run hot, central banks will tilt to being more hawkish). Moving in the other direction, a few analysts have noted a blog piece by the NY Fed Liberty Street which notes an easing of supply chain pressures since December 2021, but that an appropriate policy response is not clear with DSGE models implying “monetary policy can only achieve faster disinflation at a considerable cost in terms of forgone economic activity”.

Powell wasn’t the only central bank head speaking with BoC Governor Macklem also giving a speech that sounded hawkish. Governor Macklem noted “…inflation is well above our target and with inflation well above our target we are more concerned about the upside risks to inflation than the downside risks”. While the pace will depend on how the year evolves “ …if we have to move more quickly we are prepared to do that. So I’m not going to rule out 50 basis point move in the future.” The other interesting aspect worth highlighting in the context of central banks globally is the emphasis Macklem (and also US Fed Chair Powell) put on inflation expectations: “The lesson from history is that if inflation expectations become unmoored, it becomes much more costly to get inflation back to target.” That suggests we should be watching inflation expectations very carefully for the pace of hikes given the uncertainty around Russia and Ukraine. Finally on the balance sheet, Macklem said QT would be done by allowing maturities to roll-off rather than outright selling (” We do not intend to actively sell bonds.”) and that this would see the balance sheet unwound quickly.

As for commodity prices, they remain under the spotlight given the potential for supply disruptions. Spot Brent crude oil hit almost $128 per barrel overnight although it has since given back those gains amidst speculation an Iranian nuclear deal could be close, which would help release Iranian supply to the market. Brent crude is now down around 2% on the session. Likewise, European natural gas futures hit an all-time high of €200 before falling back to €160. Aluminium prices hit a record high and nickel an 11-year high. Wheat futures surged 15%, taking their gains this week alone to almost 40%, while corn futures jumped another 3%.

Data continues to take a back seat to Ukraine and US Fed developments. For what it is worth the US Services ISM was lower than expected at 56.6 against 61.1 expected in February and from 59.9 previously. Driving the decline in the index were falls in activity (-4.8 to 55.1), new orders(-5.6 to 56.1) and employment (-3.8 to 48.5). Although the employment sub-index is below 50, this likely reflects a shortage of labour rather than shedding given jobless claims fell back 215k from 233k last week. One anecdote within the survey was particularly revealing as to how tight the labour market was: “ The Great Resignation is real: Employees, contractors and consultants continue to quit their jobs and engagements for opportunities that pay more and have more flexible work options. Millions of light industrial jobs remain open in the U.S., with limited interest from job seekers. Severe labor shortages are expected well into 2022. Corporations need to increase wages and salaries to attract talent and get work done. Faster wage growth is expected to lead to increased inflation.” Indexes associated with supply chain issues showed little signs of easing.

As for Australia, two pieces to note yesterday. The first is the trade surplus hit its second highest level ever. Given the surge in commodity prices on the back of Russia’s invasion of Ukraine, the trade surplus will leap to unpreceded levels in coming months. The second is some mixed signalling by the RBA with external RBA-board member Harper shifting the focus back to wages (rather than labour costs), noting wages growth of 4% is needed to drive inflation sustainably at target, assuming 1.5% productivity growth (see MNI INTERVIEW: RBA’s Harper Says Wages Need 4% Growth). While Harper is on the RBA board, we are more mindful of what Governor Lowe said about the RBA’s central case being consistent with considering a rate hike later this year even though wages is only forecast to be 2¾% by end 2022. Dr Lowe also noted recently: “ we do not have a specific definition as to what ‘sustainably in the target range’ means. The actual rate of inflation is relevant as are the trajectory and the outlook. So too is the breadth of price increases and the factors driving them”.

No data domestically. Offshore the focus is on Russia/Ukraine and US Payrolls. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.