Total spending grew 0.9% in June.

Risk sentiment was hammered on Friday with sharp falls in stocks and a large rally in bonds

https://soundcloud.com/user-291029717/oil-keeps-increasing-aussie-rises-above-the-confusion?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Risk sentiment was hammered on Friday. The initial headline behind that was in Asia on Friday when Russia attacked a Ukrainian nuclear facility, with some worried about the potential for nuclear fallout. That risk was evidently overblown, but importantly risk sentiment failed to rebound. European markets were clobbered with EUR -1.1% on Friday and the EuroStoxx 600 -3.6%. For the week EUR is -2.9% and Eurostoxx is -7.0%. Bonds rallied with US 10yr yields ‑11bps to 1.73%. Over the week real yields have moved by more than nominals, meaning breakevens have lifted with the US 10yr breakeven at 2.70% from 2.56% last week. Commodity prices have soared, Brent Oil was up 6.9% to $118 a barrel on Friday and over the week Brent is 21% higher, along with a host of other commodities. Some signs of funding stress remain, perhaps linked with commodities, with FRA/OIS 1m at 35.25 and its highest since April 2020. Data continues to take a back seat, though the beat in US Payrolls (678k against 423k expected) did help steady US equity market sentiment with the S&P500 -0.8% compared to the -3.6% mauling for the Eurostoxx600.

Newsflow since Friday remains net negative . Russian President Putin said Western sanctions were akin to war, but in context it was not as alarmist as the headline would have you believe. What Putin said would be a declaration of war would be a no fly zone, of which the Ukrainian authorities have been lobbying for. President Putin has also threatened the statehood of Ukraine post-invasion, stating: “If they continue to do what they are doing, they are calling into question the future of Ukrainian statehood” “And if this happens, it will be entirely on their conscience. ” Meanwhile the US is working with Poland to free up Russian-made aircraft for Ukraine. So far there does not appear to be a clear exit ramp for either Russia, Ukraine or for the Western imposed sanctions that are roiling commodity markets. Some distressed debt investors though are reportedly buying the dip given dollar-denominated Ukraine bonds are currently trading at 22 cents in the dollar and Russian bonds at 17 cents in the dollar. (WSJ: Investors Start Buying Ukraine, Russia Bonds).

Global growth fears abound given the surge in commodity prices, with ‘stagflation’ again rearing its head in what must be akin to a horror move for a central bank. The IMF has warned “the ongoing war and associated sanctions will also have a severe impact on the global economy ”. A key question for markets is how do central banks respond to higher inflation and the possibility of slower growth ahead. One hint of that was in Powell’s Senate Testimony on Thursday when Senator Shelby asked Powell whether like Volcker he was “…prepared to do what it takes to get inflation under control, and protect price stability”. Powell’s answer was “And I hope history will record that the answer to your question is yes”. When prompted gain Powell’s answer was “Yes.”. (see video of Shelby and Powell). The Fed’s Evans re-iterated the new Fed view of them being behind the curve, with Evan’s stating “I have said ‘wrong-footed’ [on policy], and I think that’s the right term. It happened very quickly”.

In that context the Fed’s Evans wants to get closer to neutral by the end of the year – “If we were to do 25 basis points at each meeting, which may be more than I think is essential, but if we did it at each meeting, we’ll end the year at 1.75% to 2%…That is close enough to neutral that we could take quick action if it were necessary. Or we could stick or we could back off if that is what the case was .”. Such a profile would mean the Fed hiking 7 times in 2022. Markets currently price 5.7 rate hikes in 2022. It is also worth noting it isn’t only commodity driven inflation. Former Treasury Secretary Summers recently published a working paper noting “housing will make a significant contribution to overall inflation in 2022, ranging one percentage point for headline PCE to 2.6 percentage points for core CPI” (see NBER: The Coming Rise in Residential Inflation ). It is worth noting in this context of the Fed fighting against inflation, the curve flattening that is occurring in markets. The US 2/10s curve sits at 24.9bps, having fallen by 6bps on Friday. And the 2s5s is at 15.5bps. Meanwhile the Eurodollar adjusted rate is inverted from September 2023.

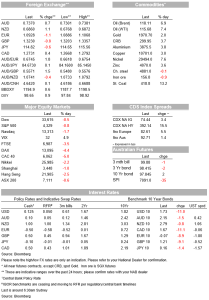

Key commodities continue to march higher. The Bloomberg commodity index hit a fresh 7½-year high on Friday, bringing its gain on the week to 13%, its biggest weekly increase since the inception of the index in 1960. Commodity price increases have been broad based. On the week, Brent crude oil was 21% higher, nickel 19%, aluminium 15%, zinc 12%, and copper 8%, while in terms of soft commodities, wheat futures were 60% higher on the week and corn 15. Much of the move in commodities stem from traders steer clear of Russian exports for fear of falling afoul of sanctions, even if energy isn’t sanctioned. Short of an end to hostilities, there doesn’t appear to be much on the horizon to temper the rally. The Iranian nuclear deal has been held out as one possibility, though Russia has said it wanted written guarantees that Ukraine-related sanctions won’t prevent it from trading broadly with Tehran under a revived pact. It is also worth noting such a deal would do little to dent a shortage of oil with Russian exports amounting to around 5m barrels a day, compared to Iran possibility bringing back 1m barrels a day. The White House has also said it is considering a ban on Russian oil imports.

In FX it remains a story of ongoing weakness in the EUR on the back of concerns about the impact of Russian sanctions and surging energy prices on the Euro area economy. The EUR broke below 1.10 for the first time since mid-2020, falling 1.3% on Friday to 1.0930. The GBP was caught in the downdraft, falling 0.9%. The USD was stronger by default, up some 0.9% on the DXY and 0.6% on the broader BBDXY with the index hitting an 18-month high on Friday. It has of course been a completely different story for AUD and NZD, which have been benefiting from the tailwind from fast rising commodity prices. The AUD was up 0.7% on Friday with the NZD also up a strong 1.1%. Over the week the AUD is the best performing currency up 2% and the NZD is up 1.7%. In contrast, the EUR has fallen by 3% over the past week and the AUD has gained some 5% against the Euro over the week.

The EUR is likely to remain under pressure ahead of the ECB meeting on Thursday (see coming up for details). As for European exposure to Russian debt Fitch said it expected the direct impact of the Russian crisis should be manageable for European banks. Fitch noted that for Societe Generale and UniCredit, the two European banks with the largest exposure to Russia, even a full write-off of their Russian subsidiaries would only reduce their capital ratios by 40bps and 15bps respectively and leave both well above regulatory minimums. Meanwhile President r Putin on Saturday signed a decree allowing Russia and Russian companies will be allowed to pay foreign creditors in rubles as a way to stave off defaults while capital controls remain in place.

Finally, the details on US Payrolls which were much stronger than expected at 678k against 423k expected and helped to settle US equities after the large negative lead from Europe. Note the whisper number was probably higher given the high frequency Homebase data had been consistent with a 600k print. There were also favourable upward revisions to the prior two months of +92k. The unemployment rate also fell be more than expected to 3.8% from 4.0% (consensus 3.9%). Average hourly earnings though were softer at 0.0% m/m against 0.5% expected, though details revealed a very noisy read on an industry basis which may suggest the softness was just volatility in the data. The report of course makes little difference for the Fed.

Only ANZ Job Ads domestically. Very quiet offshore as well with all focus still on on Russia/Ukraine. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.