Online retail sales growth slowed in May following a fairly strong April

Insight

US yields higher with Jobless Claims lower than expected

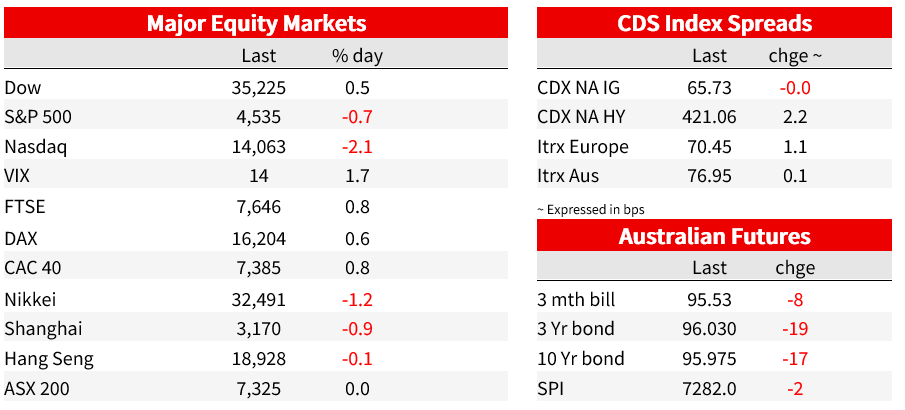

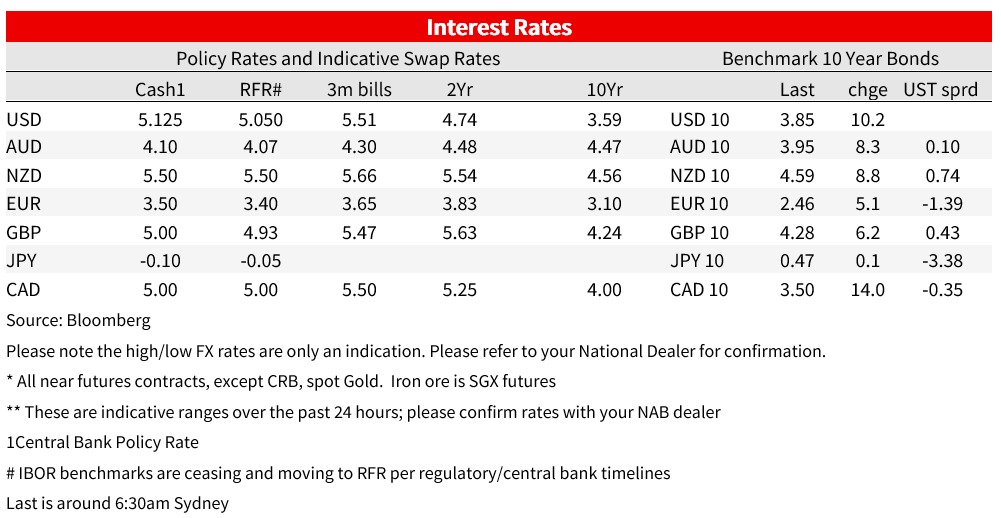

Still too strong labour market data has seen yields rise in Australia and the US, while key earnings misses post-close yesterday by Netflix (-8.4%) and Tesla (-9.7%) weighed on equities. Overnight it was US Jobless Claims that surprised, coming in at 228k vs. 240k expected and 237k previously, and is the lowest reading in two months. That is also for the week of 15 July, which covers the payrolls reference week, setting up expectations for another strong payrolls print as indicated by high frequency Homebase data. Also out was the Philly Fed Survey which saw the prices received index surge to 23.0 from 0.1, taking the index back to its highest level since January 2023. US Treasury yields rose in the aftermath with the 2yr yield up 7bps initially, before paring back and is up 6.6bps to 4.83% over the past 24 hours. The 10yr rose by more, up 8.9bps initially and over the past 24 hours is up 9.8bps to 3.85%. In Australia the 3yr bond future has moved by 17bps, with 6bps of that occurring overnight. Looking to next week’s FOMC meeting, markets are 96% priced for a 25bp hike, and see a 38% chance of a follow up hike by November. Thereafter markets price in 140bps of cuts by the end of 2024.

Equities were mixed with the S&P500 (-0.7%) and NASDAQ (-2.1%) both down, but the Dow up +0.5%. Disappointing earnings results by Netflix (-8.4%) and Tesla (-9.7%) post-close yesterday have weighed heavily. Semi-conductors were also weaker after TSMC (-5.0%) said it expects revenue in 2023 to be down 10%, a larger percentage drop than the low-to-mid single digits it forecast three months ago; the Philadelphia semiconductor index fell -3.6%. Other interesting anecdotes from TSMC company were that there was a sluggish economic recovery in crucial markets, particularly China, which has led to subdued demand for chips in smartphones, servers and cars. TSMC customers are exercising caution in managing their inventories to avoid getting overstocked. On the positive side AI chip demand is outpacing its ability to supply them. It said it is working as quickly as it can to build its capabilities in advanced-chip packaging (see WSJ: TSMC Delays Start of First Arizona Chip Factory, Citing Worker Shortage for details).

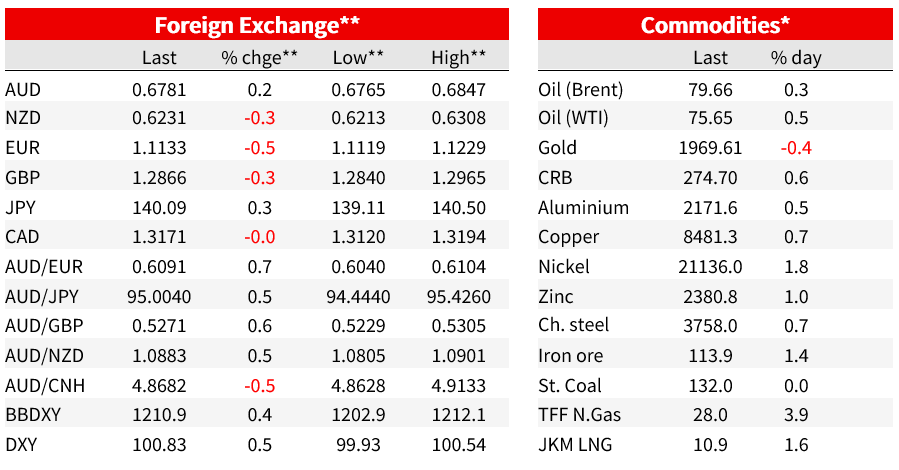

Currency markets saw broad USD strength (DXY +0.5%), while a strong Australian employment report yesterday and PBoC moves to push back against Yuan depreciation pressures, has seen the AUD higher (AUD +0.2% to 0.6779). Yesterday, the PBoC set the yuan reference rate at the largest premium since November, stepping up its campaign to support the beleaguered currency. In addition, it raised the macro-prudential adjustment parameter for cross border funding to 1.5 from 1.25. This is a multiplier that determines the upper limit of outstanding cross-border financing an institution can have, making it easier for domestic firms to raise funds from overseas markets, another tool that works at the margin to support the yuan. The yuan has sustained the recovery seen after PBoC’s actions, with USD/CNY below 7.18 from the prior 7.23 level. The NZD didn’t managed to hold onto the yuan-inspired strength with the NZD -0.3% to 0.6233. Other majors were EUR -0.5%, GBP -0.3% and USD/JPY +0.3%.

As for the Aussie jobs yesterday , employment rose 32.6k in June, beating expectations for +15k (NAB +10K). The result follows a very strong May print of +76.5k and leaves trend employment at 39k per month. The unemployment rate fell a tenth to 3.5% (unrounded it was even lower at 3.4666% just marginally above the cycle low of 3.4% in October 2022). For the RBA, this should reduce fears of a greater deterioration in the labour market than forecast that surfaced in the July Board Minutes, and reinforces NAB’s view that the RBA is not quite done yet. The RBA clearly has the opportunity to take out a little more inflation reducing insurance without worrying about unemployment rising significantly and NAB sees the RBA hiking two more times over coming months (for NAB’s coverage of the data, please see AUS: Employment growth double expectations, still a long way from the RBA’s pre-conceived 4½% NAIRU).

Overnight data was mixed, with the highlight being US Jobless Claims coming in lower than expected (228k vs. 240k consensus and 237k previously). As noted above the data was for the week of 15 July, which also covers the payrolls reference week, setting up expectations for another strong payrolls print as indicated by high frequency Homebase data. There are also reasons to be cautious in over-interpretating the fall back given shifting seasonals. Other data out included the Philly Fed Manufacturing Survey which was very mixed. The headline was weaker than expected at -13.5 vs. -10.0 consensus and -13.7 previously. But the measure looking at future conditions was much more positive with the future general activity index jumping to 29.1 from 12.7, its highest reading since August 2021.

One area worth watching was prices received where the index climbed to 23.0 from 0.1, with the index being at its highest level since January 2023. A special survey question showed that 58% of firms indicated higher labour costs over the past three months and 30% of firms plan to increase wages and compensation by more than originally planned this year (see Philly Fed: July 2023 Manufacturing Business Outlook Survey for details). Also out overnight was US existing home sales which fell 3.3%, continuing the theme of a lack of activity in the resale market due to low inventory, and this lack of supply driving buyers to the new home market.

Coming up:

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.