Online retail sales growth slowed in May following a fairly strong April

Insight

RBA’s April meeting yesterday left policy on hold at 0.1% but underwent a substantial rewrite to the post meeting statement.

https://soundcloud.com/user-291029717/no-patience-left-at-rba?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

More hawkish messaging from central banks set the tone with yields higher globally and equities lower. The RBA’s April meeting yesterday left policy on hold at 0.1% as widely expected, but the post-meeting statement underwent a fairly substantial rewrite, dropping any reference to ‘patient’ and opening the door to react to data flow ‘in the coming months.’ The Fed’s Brainard talked up a ‘rapid pace’ of balance sheet reduction, wanting policy to get to a ‘more neutral setting this year. The U.S., EU and G-7 are reportedly set to announce a new round of sanctions on Russia today.

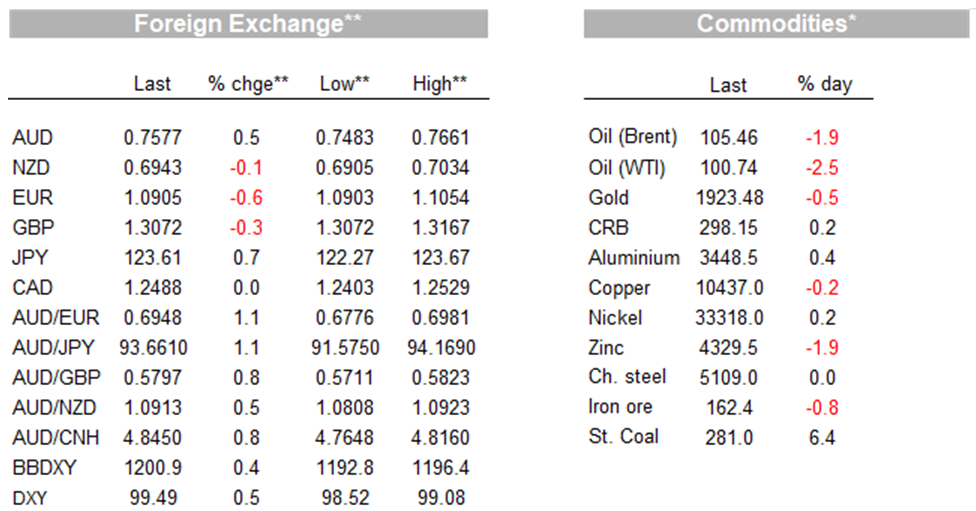

The US curve steepened, with 10yr rates up 16bps to 2.55 , outpacing the still notable move higher in 2yr yields of 10bps to 2.52. The steeping took to the 2s10s out of inversion. Brainard’s comments also supported the USD. The DXY was up 0.5% to 99.49, rising strongly against the euro and yen. The AUD was the only G10 currency to gain against the USD, up 0.6% and boosted by the RBA’s tone shift. Markets were already well ahead of RBA guidance, pricing an aggressive profile of hikes this year and cash rates above three in as little as 18 months’ time, but that didn’t do much to tame the market reaction. The AUD rose as much as 1.6% immediately after the meeting reach 0.7661, the highest it’s been since June last year, before giving back more than half its gains alongside the broadly stronger dollar to end up 0.5% higher, trading at 0.7577. That initial reaction to the RBA was mirrored in rates, with Australian 3yr yields up 15bps in the 30 minutes following the meeting, and trading as high 2.50% through our afternoon.

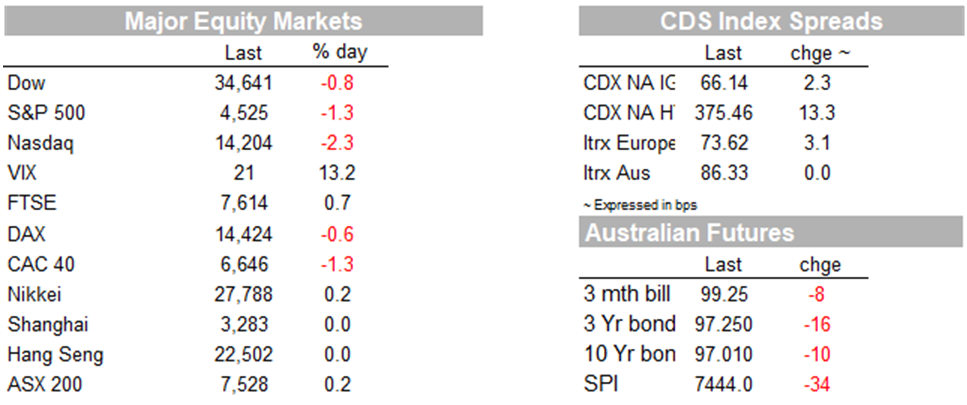

Equity markets were lower. The S&P 500 losing 1.3% and the tech-focussed NASDAQ down 2.3%. Consumer discretionary and IT stocks led declines. Twitter shares bucked the trend, up another 2.1% as the company said it would add Elon Musk to its board. That is after yesterday’s 27% gain following Musk’s disclosure of a 9.2% stake. In Europe, the DAX was off 0.6%, while the FTSE 100 managed a 0.7% gain.

In terms of the news flow, Lael Brainard, who is the next vice-Chair subject to Senate confirmation, underscored the imperative to move rates methodically towards neutral, saying “I think we can all absolutely agree inflation is too high and bringing inflation down is of paramount importance ” while citing upside risks to the inflation outlook. On the balance sheet reduction, Brainard flagged a ‘considerably more rapid pace’ than last time’ and suggested the process could begin as soon as next month. That points to larger caps and a shorter period to phase in the maximum caps compared with 2017–19, when the Fed began by limiting runoff to $10 billion a month before ramping to a maximum of $50 billion a month. Brainard, didn’t signal anything about the appropriateness of a 50bp hike in May, but did suggest that balance sheet reduction would serve the same function as additional rate rises, saying the process “will contribute to monetary policy tightening over and above the expected increases in the policy rate .” Separately, the Kansas Fed’s George said “I think 50 basis points is going to be an option that we’ll have to consider”

The RBA kept rates on hold to nobody’s surprise, but did undergo a substantial rewrite to the post meeting statement. Gone are all forward looking commitments to maintaining highly accommodative monetary policy, in its place remain accommodative. Instead, policies during the pandemic “have supported progress towards the objectives” and “ The Board will assess … incoming information as its sets policy to support full employment in Australia and inflation outcomes consistent with the target.” Importantly, the reference to being patient as it monitors how the various factors affecting inflation in Australia evolve is gone, replaced with something that is much better footed to react to incoming data flow. We see the risks firmly planted to the upside to the RBA’s near-term inflation forecasts and the unemployment rate looks primed to fall below 4 as soon as March. With Q1 CPI due in April 27 and Wages data due May 18, we think that makes June the most likely data for lift off, with meetings very much live from May.

Perhaps adding further clues to the RBA’s thinking, the AFR’s Kehoe, who is often well connected on the RBA’s thinking, wrote that “a series of interest rate rises starting in June now looks to be the Reserve Bank of Australia’s destiny,” with a ‘reasonable’ wages data out of the 18 May WPI and 1 June National Accounts and sufficient to raise rates. He writes that “the RBA will probably start gently with a 0.15 of a percentage point increase to 0.25 per cent”

Outside of central bank news, Russia-Ukraine developments continue. This time sanctions related with the U.S., EU and G-7 set to announce a new round of sanctions today. That will reportedly include a ban on new investments in Russia. The EU has proposed prohibiting imports of Russian coal, as the direction of the sanctions mix creeps into the energy complex. The US is reportedly planning to freeze overseas assets of some Russian banks. Given that backdrop, energy markets were reasonably staid. Brent Oil was down 2.0%, though benchmark gained 6.4%.

The data flow overnight was fairly quiet. The US Services PMI rose 1.8 points to 58.3, broadly in line with expectations for 58.5. That’s not quite the 60+ numbers seen late last year, but is a strong read. Respondents indicated that they continue to be impacted by capacity constraints, logistical challenges and inflation. The employment subindex rose 5.5 points 54 as labour shortages eased on the back of lower COVID cases and relaxed public heath restrictions. That’s in line with the rebound in the employment subindex in the manufacturing survey late last week.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.