Total consumer spending grew 0.7% in July

Insight

The reaction to the Fed minutes early yesterday morning continued to dominate markets overnight.

https://soundcloud.com/user-291029717/consumers-still-spending-despite-all-the-hike-talk?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

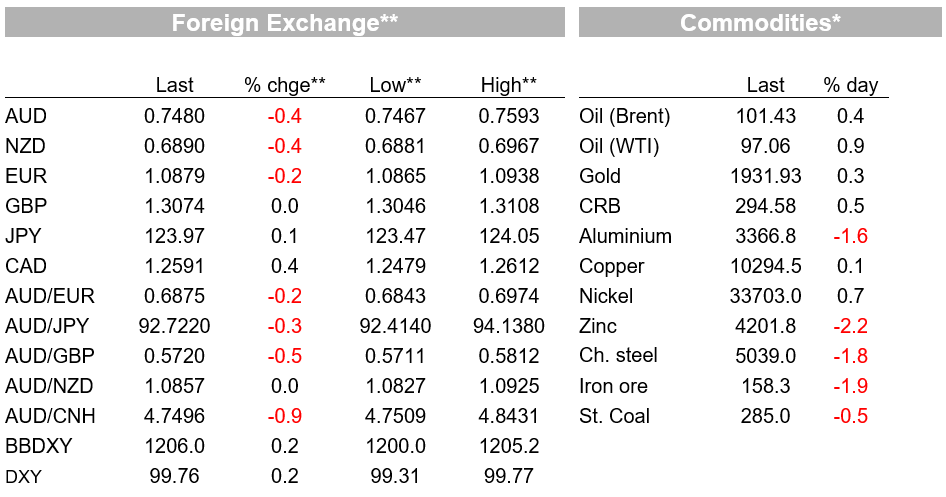

The reaction to the Fed minutes early yesterday morning continued to dominate markets overnight. US 10yr yield resumed a move higher, while ECB minutes revealing “a large number” of members saw the case for immediate steps towards policy normalisation helped European yields higher. Otherwise, there was little news flow of note. The Fed’s Bullard, called for 300bps of hikes, not out of line with his previous hawkish comments. The EU ban on Russian coal, mooted earlier in the week, was agreed, extending sanctions into energy, but there was little reaction in commodity markets. Brent finished 0.4% higher at US$101.43.

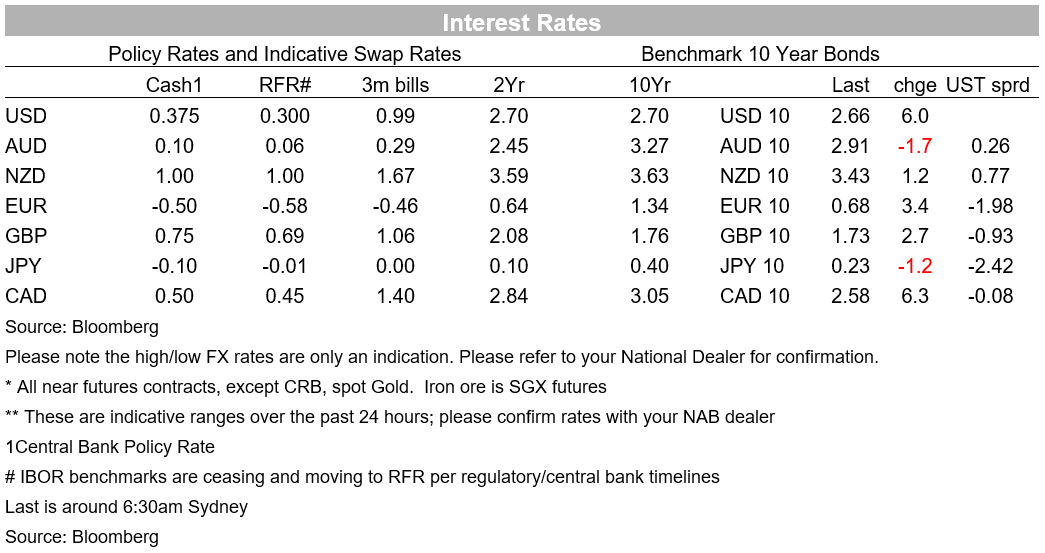

The US dollar was broadly a little stronger. The DXY up 0.2% to 99.79. USD gains were largest against the AUD and NZD, both losing 0.4% against the USD. The aussie settling back below 75c at 0.7480, 2.4% lower than the high of 0.7661 touched briefly after the RBA on Tuesday. Yields were mostly higher globally. US 10yr yields rose 6bps to 2.66%, reaching its highest since March 2019 the 2s10s curve steepening further with the 2yr yield little changed, 1bp lower at 2.46%. European 10yr yields were also higher, up 3bps to 0.68%.

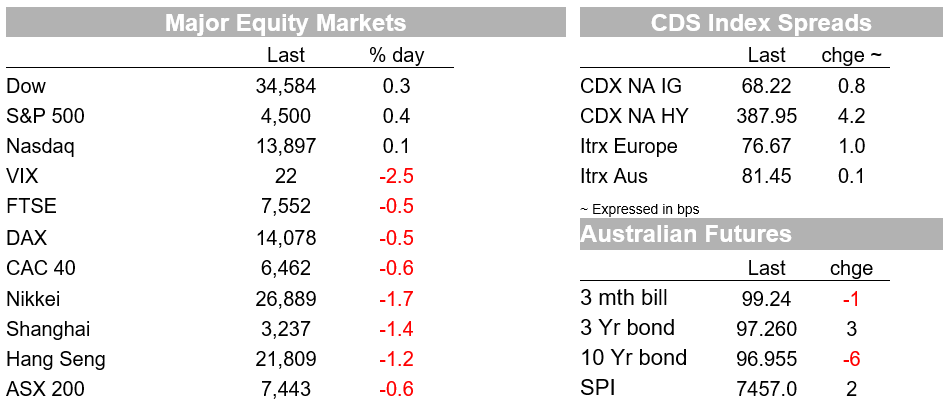

Equities in the US finished higher , turning around in the US afternoon with no obvious news to drive the move. The S&P 500 was up 0.4%, the NASDAQ eking a 0.1% gain. Health care and energy led the gains, while real estate stocks declined. The rally comes after 2 days of losses alongside the move higher in yields following Brainard’s suggestion of a faster and sooner balance sheet runoff. European and Asian equities fared worse. The DAX and FTSE were each down 0.5%, while the Nikkei lost 1.7%.

The ECB minutes helped European yields higher. The account of the March ECB meeting reflected the highly uncertain environment the ECB is facing but showed a pull in a more hawkish direction amid elevated inflation. “A large number of” members viewed that current high inflation “called for “immediate further steps towards monetary policy normalisation” and that “the three forward guidance conditions for an upward adjustment of the key ECB interest rates had either already been met or were very close to being met.” Some members preferred to set a firm date for the end of asset purchases during the summer, clearing the way for a possible rate hike in Q3. Other members argued that “the forward guidance conditions had not yet been met and it was also not obvious whether they would be met soon” preferring a ‘wait-and-see approach’ amid exceptionally high uncertainty.

More commentary from Fed official overnight didn’t do much to move the dial on the Fed’s march to neutral. St. Louis Fed’s Bullard was true to his hawkish self. He noted that “I would like the committee to get to 3-3.25% on the policy rate in the second half of this year” and said he would “lean into ” a 50bp hike at the May meeting. Not surprising given he supported a 50bp move in March. Bullard said that balance sheet runoff wouldn’t be “a reason to hold back on where we think the policy rate should be.” Bullard cited a Taylor Rule to suggest the policy rate is around 300bps too low, and argued that market pricing means that the Fed is not as behind the curve as it looks, “although it would still have to raise the policy rate to ratify the forward guidance.”

Non-voters Evans and Bostic sounded a more moderate tone, appearing on a virtual panel, but still supported shifting policy to a neutral stance. “I think it is fully appropriate that we move our policy closer to a neutral position. But I think we need to do it in a measured way,” said Bostic. Evans, still expecting supply chain drivers of inflation to ‘come off the boil’ said that “ I am optimistic that we can get to neutral, look around and find that we are not necessarily that far from where we need to go.”

There was little in the way of data flow overnight. US new jobless claims fell to 166k in the week to 2 April, against expectations for 200k. In case any more evidence were needed of the very tight US labour market, that’s the lowest since 1968. As for Australian data yesterday, there is also nothing too noteworthy. For the record, the February trade balance came in sharply below expectations at $7.5bn from $12.9 and against $11.7bn expected. That was entirely due to a 12% gain in imports, with exports flat. February was too early for higher commodity prices to feed through to assessed export values, but there was some evidence of higher prices coming through on the imports side in fuel and processed industrial supplies. A broad-based 17% surge in consumption good imports also of note, perhaps an early positive signal of easing supply constraints against a backdrop of still high consumer demand and efforts to rebuild inventories. The more timely Payrolls data for the 4 weeks to 12 March showed a 0.6% decline in jobs, but doesn’t derail our expectations for a strong March print in the official employment numbers on Thursday.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total consumer spending grew 0.7% in July

Insight

Investing and risk management in a world of shifting and unstable cross-asset correlations

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.