Total spending grew 0.9% in June.

News of Russia’s decision to cut gas supply to Poland and Bulgaria triggered a 30% jump in EU gas prices at the open before eventually settling 10% higher.

Markets remain very volatile and after big declines in the previous day, US and EU equities managed a small rebound overnight. Russia stops gas supplies to Bulgaria and Poland, triggering a big jump in European gas prices at the open, but EU commission reassurance limited the jump to just 10%. The euro hits a five-year low, helping the USD reach a 5y high, AUD and NZD show resilience amid a volatile market environment.

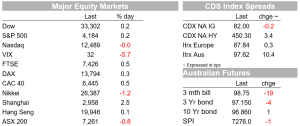

Equity market volatility has remained elevated with the VIX index closing the NY session at 31.6. After big declines in the previous day, EU and US equity markets rebounded overnight, but it is hard to get too excited and claim a sustained turn around in sentiment is in the offing . Risk asset in general still need to navigate the consequences from what looks to be an increasingly more aggressive policy tightening by many central banks and now the RBA also looks likely to join this camp next month ( more below), China’s zero-covid policy remains in place and the prospect of a protracted Russia Ukraine conflict does not bode well for the energy prices and energy supply for Europe in particular.

So, against this uncertain backdrop, the S&P 500 ended the day up by 0.21%, after trading in and out of positive territory and at one point up over 1.5% intraday . The NASDAQ also had a wild night, but in the end closed the day little changed, -0.01%. The tech heavy index remains in bear market territory and on the day was not helped by Alphabet 2.3% decline on disappointing sales reported after the bell yesterday. In contrast, Microsoft’s share price rose almost 8% after posting stronger revenue and earnings. After the bell, Meta Platforms (Facebook)reported strong user numbers, lifting its share price by 13% and helping extend gains in US equities in aftermarket trading.

Meanwhile in Europe, the Stoxx 600 Europe Index closed 0.7% higher, reversing early losses of as much as 1%. Early in the session, EU equities gapped lower amid concerns over Russia decision to halt gas flows to Poland and Bulgaria. The EU commission was quick to respond, saying Europe was prepared for it while reassuring that there is enough fuel in storage for the weeks ahead. This reassurance helped with the turnaround in sentiment. Of note as well Mercedes-Benz AG gave automakers a boost by rising after reporting better-than-expected earnings.

News of Russia’s decision to cut gas supply to Poland and Bulgaria triggered a 30% jump in EU gas prices at the open before eventually settling 10% higher. Despite the 16% increase over the past two days, gas futures remain almost 70% below their peak early last month. Poland and Bulgaria have been preparing for a cut in gas supply from Russia, now the big question is how Italy and Germany, the big EU gas buyers from Russia will deal with the Moscow’s demand to pay in roubles with contract deadlines by the end of May, so there is still a bit of time for a resolution and or more clarity from the . EU commission guidelines in terms of what would constitute an acceptable workaround.

There is a lot at stake here, Russia supplies about 40% of gas to Europe with a big portion of this going to Germany and Italy. Overnight, German economic affairs minister Habeck said the German economy could shrink 5% if Russian gas was halted. Meanwhile the FT reckons a rough and ready estimate of the value of Russian pipeline gas exports to Europe is about $120bn of revenue. If Russia forfeited eight months of the income via stoppages, it would shave 5.3 % off forecast GDP, which is expected to drop sharply in any event.

The above figures play to the view that some sort of compromise is likely and partly explain the rebound in EU equity sentiment recorded overnight. The problem here is that logic has not been a good guide to Russia’s action so far this year, so the risk of big EU recession remains very elevated..

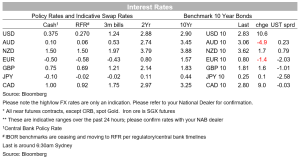

Thus, not surprisingly, the euro remains under downward pressure amidst broad-based USD strength and an intensifying energy crisis on the continent. The EUR fell as low as 1.0515 overnight, its lowest level in more than five years, although it has since recovered slightly to around 1.0557 . The counterpart to EUR weakness has been continued USD strength, with the DXY index rising another 0.6% overnight and briefly hitting a five-year high. Expectations of aggressive Fed tightening and fragile risk sentiment remain supportive drivers of the USD.

Ahead of today’s BoJ meeting, the JPY has given back some of its gains from the past few days following the rebound in US Treasury rates. After briefly probing below 127 yesterday morning, USD/JPY is back above 128. The stabilisation in the CNH has helped support the AUD and NZD , although the kiwi is still down around 0.35% relative to levels this time yesterday while the AUD is essentially unchanged at 0.7126.

Yesterday the AUD got a small and brief lift from the stronger than expected Australian Q1 inflation print . Headline CPI came in much stronger than expected, at 5.1% y/y (4.6% exp.) while the all-important trimmed mean core inflation measure was 1.4% higher on the quarter (3.7% y/y), miles above the RBA’s most recent 0.8% forecast. With the RBA’s preferred core inflation measure now well above the top of its 2-3% inflation target range, the market has swiftly moved to bring forward RBA tightening expectations, with 22bps now priced in for the May meeting (implying a certain chance of a 15bps move and a ~30% chance of a 40bps hike). NAB now expects the RBA will raise the cash rate target by 15bps at next week’s May Board meeting. Further 25bp increases in June, July, August, and November will take the cash rate target to 1.25% by year’s end

US rates have rebounded overnight, in sympathy with the recovery in equities. The US 10-year rate is 10bps higher on the session, at 2.82%. In contrast, European rates were flat to slightly lower as the market modestly pared back its ECB rate hike expectations amidst mounting tensions with Russia. Notably, the Italy-Germany 10-year spread increased to its highest level since mid-2020, at 178bps, as the market braces for less ECB bond buying support ahead.

Some slightly more positive headlines have emerged around China’s Covid situation, although investors remain wary. Shanghai said it would allow some limited movement for those in areas where there is no community transmission of the virus. New daily Covid cases in Beijing remain below 50, although the market remains concerned that the city could be put into a growth-damaging lockdown in the coming weeks. The global experience has been that Omicron is exceptionally difficult to snuff out, even with lockdowns.

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.