Total spending grew 0.9% in June.

A wild ride in FX markets over the past 24 hours

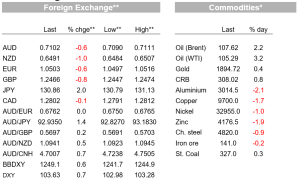

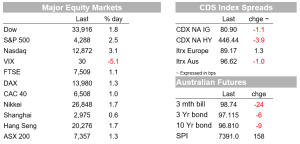

A wild ride in FX markets over the past 24 hours with the USD/JPY blasting through 130 overnight (currently 130.91) after the BoJ doubled down on its 10yr YCC. The USD continued its ascendency with DXY at a 20 year high (+0.6% overnight) with most pairs lower. As for risk events, the German CPI came in higher than expected (7.8% y/y against 7.6% expected) and the Riksbank surprised by hiking 25bps and guiding a further 2-3 hikes this year. European yields were higher in the wake on with the German 10yr Bund +9.9bps to 0.90%. A much weaker than expected US Q1 GDP was largely dismissed as being noise with large detractions from net trade and inventories seeing GDP at -1.4% annualised against +1.0% expected. Equities meanwhile had a stellar night with strong earnings by Meta (+17.5%) after the close yesterday, along with Qualcomm (+9.7%), helping to propel the tech sector higher. The NASDAQ closed up 3.1% and the S&P500 was 2.9% with all sectors in the green. Note Apple reported after the close with mixed earnings with its stock down 1% in extended trading, Amazon is also set to report after the close.

First to the BoJ yesterday. The BoJ doubled down on its 10yr YCC, stating it would now conduct bond buying operations on an ongoing daily basis going forward at a fixed 0.25% yield. Previous YCC interventions had only been ad hoc, when the market was challenging the upper-end of its perceived 0.25% tolerance limit for the 10-year bond rate. The BoJ’s move signals it remains committed to its ultra-easy monetary policy stance, despite the sharp weakening in the Yen. There had been some speculation going into the meeting that the BoJ might either revise its forward guidance or hint at future changes to its YCC policy, but that was very wide of the mark. USD/JPY exploded higher after the announcement and is up a massive 2.1% from this time yesterday and is now trading close to 131 (currently 130.91). Comments by the Finance Ministry of recent moves in the JPY warranted “extreme caution” were ignored and with the BoJ signalling it stands committed to cap the 10-year Japan bond rate at 0.25%, any further increases in US rates will mechanically widen the interest rate differential, likely putting upward pressure on USD/JPY.

Moves in JPY are spilling over to other markets with USD/CNH decisively braking above 6.60 , and is up 1.1% over the past 24 hours, its biggest one-day move since March 2020. USD/CNH is trading at around 6.66, its highest level in 18 months. Except for the CAD, the USD is stronger across the board overnight by around 0.6% on the DXY and briefly traded at a 20-year high, just below 104. The strength in the USD overnight has come despite the strong rise in risk appetite as seen in equities overnight. Likewise the AUD (-0.6%) and NZD (-1.0%) were weaker overnight. Given the AUD and NZD are two of the most risk sensitive currencies, emerging global growth headwinds from China and Europe have seen both come under pressure.

US Q1 GDP disappointed, but was largely downplayed by markets. Headline GDP came in at 1.4% annualised against +1.0% expected, though the details revealed net trade and inventories detracted sharply from growth. Domestic growth components were strong with consumption at 2.7% annualised and investment very strong at 9.2%. While there was certainly noise within the GDP figures and should be downplayed somewhat, it does suggest some flattening off of growth and consumption while strong at 2.7% annualised, missed the consensus of 3.5%. That should put a premium on the PCE real spending figures out later today where the consensus is for real spending to have fallen by 0.1% m/m in March. Buying intentions are also very low levels so the health of the consumer will be watched closely over coming months.

Recession talk also continues with many commentators noting the risk of recession is building – Ken Rogoff the latest to add to that view, noting “the odds of recession in Europe, the US, and China are significant and increasing, and a collapse in one region will raise the odds of collapse in the others. Record-high inflation does not make things any easier”. Even though equities were up strongly overnight on tech, earnings from industrials do suggest global headwinds are impacting. Caterpillar, a bellwether for growth said Chinese demand will be even weaker than previously expected and car companies reported chip shortages continue to constrain. Meanwhile General Electric and Texas Instruments made similar soundings.

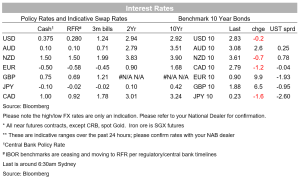

The other surprise overnight was Sweden’s Riksbank hiking rates by 0.25bps. The Riksbank had claimed as recently as February that rate hikes weren’t on the agenda for several years, but in a sharp U-turn overnight it raised its cash rate from 0% to 0.25%. The rationale was all about inflation expectations with the Riksbank noting it “ To counteract the high inflation from becoming entrenched in price and wage-setting, the Executive Board has decided to raise the repo rate from zero to 0.25 per cent”. (see Riskbank: Repo rate raised to 0.25 per cen t for details). While the rate hike was a surprise to economists (only 2/18 surveyed had expected a hike), it was priced at around a 75% chance by markets. The Riksbank also signalled it expects to raise rates another two to three times this year, a similar pace to that expected of the ECB. Sweden’s 2-year swap rate increased 15bps while the SEK has outperformed USD strength with USD/SEK +0.2% against a USD DXY of 0.6%.

European 10-year rates were much higher overnight, by around 9bps in Germany and 14bps in Italy, with the market seeing some read-across from the Riksbank (above) and also on higher than expected German CPI figures. The wider Eurozone figures are out today and yesterday Germany’s headline was 7.8% y/y against 7.6% expected. Meanwhile, Spanish annual CPI moderated to 8.3%, from 9.8% the previous month, helped by a fall in electricity prices (from what were all-time highs). More disconcertingly for the ECB, Spanish core inflation continues to increase, hitting an almost 30-year high of 4.4% y/y. ECB Vice President de Guindos said he thought the peak in European inflation was “very close” although the key question is how quickly inflation will moderate and whether it will settle above the ECB’s 2% target. Meanwhile in the US yields were broadly unchanged with the US 10yr currently trading at 2.83%.

Elsewhere natural gas futures in Europe have fallen almost 10% overnight, reversing the previous day’s spike higher after news that Russia had stopped supplying gas to Bulgaria and Poland. Bloomberg reported that Italian energy company Eni was preparing to open ruble accounts, against European Commission warnings, as a precautionary measure. Oil prices though were higher with Brent Crude +2.2% to $107.62 after reports of Germany dropping its opposition to a ban on Russian oil.

Domestically there is only the PPI and Private Sector Credit, neither particularly market moving. Offshore the focus will be on Eurozone GDP and inflation, and in the US the PCE numbers . Details below:

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.