Long-term signal vs. Short-term noise

Insight

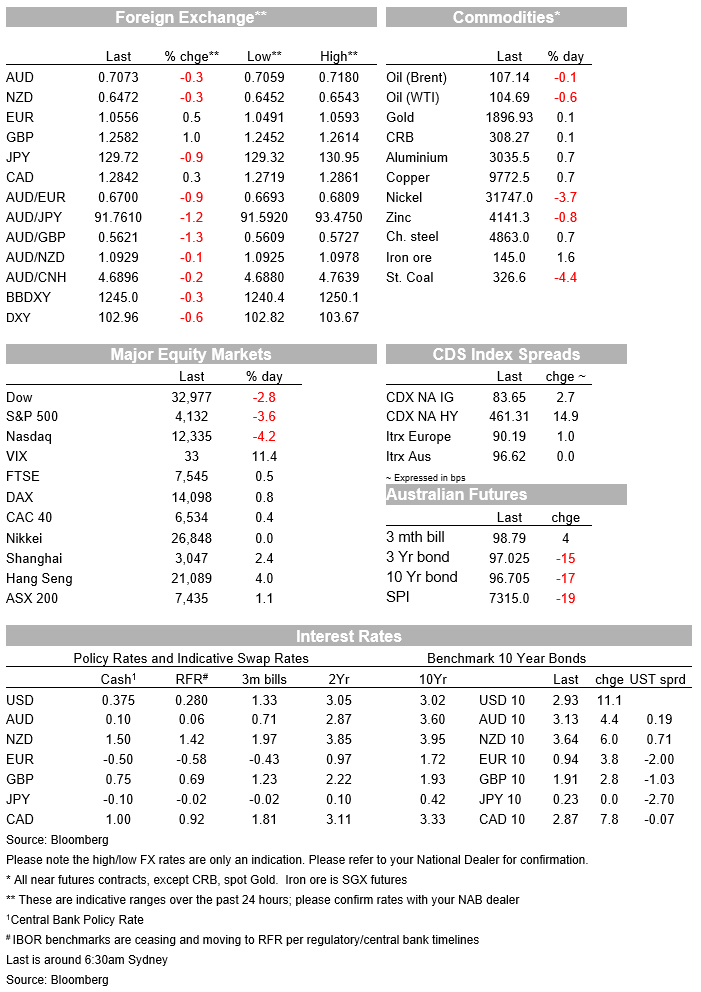

The NASDAQ recorded its worst monthly performance in more than a decade.

It was a nasty end to the month for US equities with a nasty collapse in China’s PMIs on Saturday unlikely to arrest mounting concerns over a global growth slowdown. All this against a backdrop of rising inflation fuelling the notion central banks need to accelerate their policy nomalisation process. Tech stock led a big decline in US equities amid underwhelming earnings reports from major Tech companies with a rise in UST yields an additional headwind. The USD took a breather with European pairs recovering some ground after the Euro Area’s core inflation beat expectations, increasing the pressure on the ECB to normalise its ultra-easy policy setting. Heighten risk aversion (the VIX index close the week above 33) did not help pro-growth currencies with month end flows playing its part in FX dynamics.

Tech stock led a sharp decline in US equities on Friday with declines accelerating into the close, which some commentators attributed technical factors such as hedging activity and trading by leveraged exchange-traded products. Amazon and Apple’s cautious guidance after the former recorded its first quarterly loss in seven years weighed on sentiment. Amazon shares fell 14% on Friday after the company reported sharp declines in online shopping, higher costs from inflation and supply-chain bottlenecks. Meanwhile, (after the bell on Thursday) Apple (shares down 3.7%) warned that China’s Omicron wave alongside the government’s zero covid policy could hinder sales by as much as $8bn in the current quarter.

The NASDAQ index dropped 4.2% on Friday pushing its April decline down to 13.26%, its worst monthly performance in more than a decade. Year to date, the NASDAQ is down 21% in 2022, its worst start to a year on record. Meanwhile, the S&P 500 fell 3.63% on Friday, contributing to its fourth consecutive weekly decline and an 8.8% fall for April, the Dow fell 4.9% in the month.

Meanwhile European equities managed to record modest gain on Friday with the STX Europe 600 index gaining 0.74% on the day, but still down 1.73% for the month. A large portion of the US equity underperformance came after the European close, suggesting Europe might be overdue for a catch up at the start of the new week. That said in April European equities declines were not as severe as their US counterpart, largely reflecting the fact that US equity indices are more tech/growth heavy relative to Europe with the latter more heavily weighted towards industrials and banks. A look at the big US tech companies’ performance helps illustrate this point with Netflix dropping 49% in April. Nvidia down 32% and PayPal -24%. The Wall Street Journal noted the FAANG stocks (Facebook/ Meta Platforms, Apple, Amazon Netflix and Google /Alphabet), collectively lost more than $1trn in market value in April. Very nasty!

A global growth slowdown and rising inflation forcing (most) central banks to accelerate their policy normalisation process are not helping equity sentiment. The rise in core global yields has been a theme of late with data releases on Friday providing another reason for US and EU yields to rise . The UST curve rose in an almost parallel fashion on Friday while in Europe, the move up in yields was led by the front end, flattening the curve. 10y UST yields ended the month at 2.93% (plus 10bps on the day) while 10y Bunds closed at 0.935%, up 4bps on the day with the 2y rate up 6bps to 0.246%.

The Employment Cost Index (ECI), considered one of the most comprehensive measures of US labour costs, was much higher than expected in Q1, reinforcing the market’s heightened inflation concerns. The ECI surged 1.4% q/q in Q1 (1.1% exp.), its largest quarterly increase since the survey was established in 1996, in part due to a jump in benefits payments (such as pensions) . On an annual basis, the ECI is now running at a 4.5% pace while private sector wage growth is even higher, at 5% y/y. The data corroborates the elevated readings coming from other wage measures, such as the Atlanta Fed’s Wage Growth Tracker, which is tracking at 6% y/y.

US personal income rose 0.5% in March, marginally above the consensus, 0.4% while core PCE deflator rose 0.3%, in line with the consensus. On a year-on-year measure, the Core PCE inflation dipped to 5.2% from 5.3%, marking the first decline since October 2020, more of the same is expected with base effect remaining favourable over coming months.

For now, however the market remains focus on the current US inflationary pressures and for the first time this year traders are pricing in close to 50% chance that Fed policy makers in June will raise the funds rate by 75 basis points, following the 50bps hike priced for this week. Of note too, the market now expects the Fed funds rate to rise to 3% by February next year.

Meanwhile in Europe inflation rose 7.5%yoy in April, in line with expectations, the big surprise however came from the core reading, core inflation jumped from 2.9%yoy in March to 3.5%yoy in April versus 3.2% expected. Thus, the rise in European inflation is not just about energy prices, we are also seen a broadening increase in price pressures, increasing the need for the ECB to start its policy normalisation process.

Speaking to Bloomberg TV, ECB Chief Economist Lanes said the question is no longer about hiking, but rather the scale and timing of interest-rate normalisation. The lack of pushback against market pricing for ECB rate hikes from Lane, who is usually considered one of the most dovish members of the committee, is notable. Lane added that the weakening in the euro would be an “important factor” in determining their forecasts . In contrast to recent cycles, where currency strength has been a constraint on policy tightening, EUR weakness is exacerbating inflationary pressures in the current cycle.

In a newspaper interview on Sunday, ECB Guindos said that an ECB rate increase in July is possible but not “likely”, then added that “There’s no reason why” an end to net asset purchases “shouldn’t happen in July,”. Like Lane, Guindos also noted that any decision “will depend on the data and the new macroeconomic projections in June. The ECB meets June 8 and 9.

The markets is now almost fully pricing four 25bps of ECB hikes before the end of the year ( 95bps) with Bank of America and DB calling for four ECB hikes this year.

Moving onto the currency market, the USD took a breather on Friday (DXY -0.6%, BBDXY -0.3%) with European currencies regaining some ground. The EUR rebounded 0.4% to 1.0545, helped by the higher-than-expected European core CPI data, hawkish remarks, as noted above, from ECB Chief Economist Lane. That said, putting things into perspective, the euro remains close to a 5- year low while the USD is close to a five-year high. On a DXY basis, the 4.7% increase in April was the biggest increase since 2015, while the broader BBDXY index’s 4.5% gain was its best since 2012.

With risk aversion in the air (VIX index close the week above 33), pro risk/growth currencies struggled on Friday with the AUD the biggest underperformer, down 0.51% to 0.7061 ( now at 0.7072) and the kiwi not far behind, down 0.49% to 0.6458 (now 0.6468). Looking at the AUD intraday chart, it seems reasonable to suggest month end flows did not help the aussie on Friday night with a notable decline around the London fixing (1:00am Saturday). That said, true to its risk sensitive attribute, the AUD did track the S&P 500 decline, specially the acceleration in the sell-off before the close.

Looking at other fx pairs, after breaking above ¥131 on Thursday night in the wake of the BoJ’s renewed commitment to its Yield Curve Control policy, USD/JPY nudged back below 130 on Friday ( now ¥129.76) and of note too, CNY stabilised on Friday, with USD/CNH edging back down to around 6.64.

News form China over the weekend have not been great with sharp declines in PMIs record in April, specially on the services side. The official non-manufacturing PMI fell to 41.9 from 48.4 in March, well below the consensus forecast of 46 while the official manufacturing PMI fell 2.1 points to 47.4, inline with consensus. The Caixin manufacturing PMI, which is more heavily weighted towards smaller private firms and exporters, declined to 46 from 48.1 (vs 47 expected).

Omciron and the government’s zero-covid policy were the main culprits for China’s activity decline in April, halting industrial production and disrupting supply chains. Lockdown measure remain in place in Shanghai and the market remains concern similar measures could be implemented in Beijing.

A sharp Chinese economic slowdown in the second quarter remains a realistic outcome at this stage and if history is any guide, global hit to growth would follow shortly after . On Friday, Chinese policymakers continue to make more noises about providing support to the economy. A statement from the Politburo on Friday vowed policies to meet the country’s ambitious 5.5% annual growth target while promising to “strengthen infrastructure construction in an all-around way” . For now, however, there has been a lot of talk of promises to support the economy, but concrete measures have not followed and with the country in lockdown, is difficult to see how any support can help activity.

Moving onto other news, the Ukraine war remains another major headwind for risk appetite . In news over the weekend, Bloomberg reported that the EU would propose a ban on Russian oil, to be phased in by the end of the year, although such a move would require unanimous support and some countries, such as Hungary, have been resistant to this point. Meanwhile, the UK’s defence secretary warned that Russia could formally declare war on Ukraine on May 9th, when the country celebrates the end of WWII. A formal declaration of war, rather than the ‘special military operation’ term that Russia has used to date, would enable it to call up reservists and replenish front-line forces, likely signalling it is preparing for a drawn-out conflict.

Key commodities were mostly lower on Friday with gold one exception ( up 1.08%). WTI crude fell 1.19% to 104.69 and for the week it gained 2.57%. Copper eased 0.80% to 4.3780 and for the week it fell 4.46%. Iron ore gained 2.9% on Friday , but fell 2.88% on the week.

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.