Total spending grew 0.9% in June.

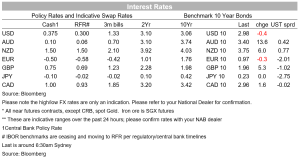

The RBA yesterday increased the cash rate target by 25bp to 0.35% and said it will do what is necessary to return inflation to the band

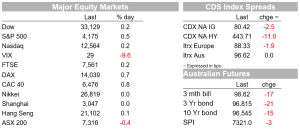

Equity markets were choppy and the USD modestly weaker ahead of the FOMC meeting. Equities ended up higher, the S&P500 gaining 0.5% after moving in and out of positive territory through the day. 9 of 11 sectors were positive, with gains led by energy and financials. European equities also gained, the Euro Stoxx 50 up 0.8%. In currencies, the DXY lost 0.3% to 103.45 as the euro gained 0.2%.

The AUD was the best performing G10 currency, but those gains came ahead of the RBA, gaining from an intraday low of 0.703 to around 0.7090 prior to the RBA decision. The currency spiked higher on the announcement, briefly touching 0.7148 before chopping around 0.711 for the rest of the day and now sitting at 0.7096, up 0.7%.

The US 10yr yield failed to hold above 3% after eking above that number again in our evening yesterday, but is down 1bp to 2.97%. The 2yr yield fared better, up 5bps to 2.77%. 10yr bunds were little changed at 0.97%, after briefly moving above 1.0% for the first time in 7 years. There was more movement in Australian rates, with the 3yr yield up 19bps and breaching 3.0% for the first time since 2014 (more below).

In terms of data flow overnight, JOLTS Job Openings in the US rose to a new record high of 11.5m from 11.3m in March, highlighting still strong labour demand. There are now 1.9 openings per unemployed person. Quits were up 3% in the month to a record 4.5m. Nothing in these data to push back against market expectations for front-loaded policy tightening by the Fed. The March JOLTS numbers were ahead of Payrolls numbers for April on Friday, seen posting another strong monthly gain of 390k alongside a decline in the unemployment rate to 3.5% from 3.6%

Eurozone employment was broadly in line with expectations. The unemployment rate declined to 6.8% in March from an upwardly revised 6.9%, with a 76k fall in the number of unemployed people a slowing from recent pace. The unemployment rate is the lowest since the euro was introduced. The German unemployment rate was steady at 5.0%. Also in Europe, producer prices rose 5.3% m/m in March for 36.8% y/y against expectations for 5.0%/36.3%.

The ECB’s Schnabel said in an interview with German newspaper Handelsblatt that “From today’s perspective, I think a rate hike in July is possible,” adding that “it’s not enough to talk now — we have to act.” Markets currently price in 22bp of tightening by July, and a positive deposit rate by October.

The RBA yesterday increased the cash rate target by 25bp to 0.35% and said it will do what is necessary to return inflation to the band and that “will require a further lift in interest rates over the period ahead ”. A 15bp move was widely expected and well-priced, with a few economists looking for a 40bp move but no one predicting the 25bp move. In the event, the Board seemed more focussed on the quantum of the change than the presentation of the cash rate target level, with Governor suggesting a 25bp move was a signal it was ‘business as usual’ despite the frankly curious choice of cash rate target that puts a large number of options on the table for future moves. Governor Lowe seemed to suggest increments of 25bp was the default for changes in the cash rate, but a 15bp or 40bp move to ‘normalise’ the cash rate target to a rounder number is a possibility somewhere in the cycle.

The post-meeting statement read as somewhat hawkish. Revised inflation forecasts have underlying inflation at 4¾% over 2022 (2ppts higher than at their February forecasts), only edging lower to 3% by mid-2024 even with an assumption of further increases in interest rates. A full forecast update comes in the SoMP on Friday.

Markets were already pricing an aggressive pace of tightening, but saw enough to move further, now pricing a cash rate of 0.73% in June (from 0.56 yesterday) and 2.81% by the end of the year (from 2.61 yesterday). Australian 3yr yields were higher on the announcement, jumping 11bps to 2.98% on the news and closing at 3.01%, up 19bps on the day and above 3% for the first time since April 2014. 10yrs also moved higher, up 14bp to 3.40%. Governor Lowe refused to be drawn on the appropriateness of market pricing in the post meeting briefing but did point to 2.5% as ‘not unreasonable’ for rates to return to over time, suggesting he has something more gradual in mind, even as the path forward depends on the data flow.

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.