Total spending grew 0.9% in June.

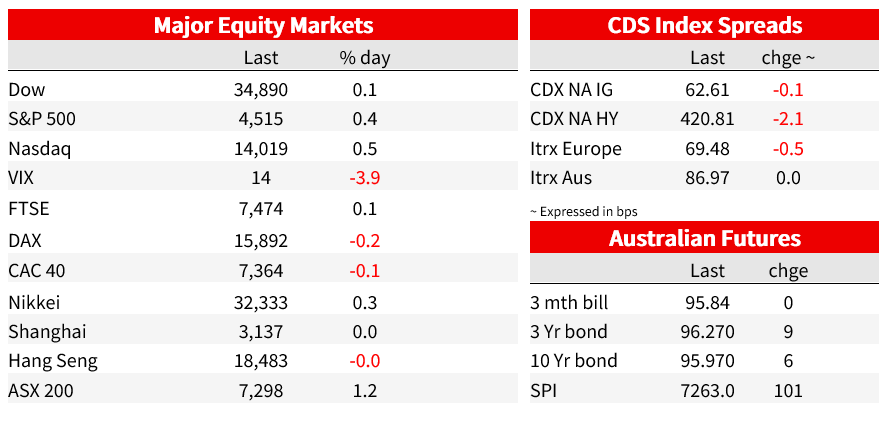

US equities extend their positive run to a fourth consecutive day with softer US economic data fuelling expectations of a Fed on hold over coming months. UST yields edged lower while European yields rose following stronger than expected German and Spanish inflation data releases. The USD lost ground against EU pairs while the AUD is little changed.

Events Round-Up

NZ: Dwelling consents (m/m%), Jul: -5.2 vs. 3.5 prev.

AU: Building approvals (m/m%), Jul: -8.1 vs. -0.5 exp.

AU: CPI (y/y%), Jul: 4.9 vs. 5.2 exp.

EC: Economic confidence, Aug: 93.3 vs. 93.5 exp.

GE: CPI EU harmonised (y/y%), Aug: 6.4 vs. 6.3 exp.

US: ADP employment change (k), Aug: 177 vs. 195 exp.

US: Goods trade balance ($b), Jul: -91.2 vs. -90.0 exp.

US: GDP (2nd est. q/q% ann.), Q2: 2.1vs. 2.4 exp.

US: Pending home sales (m/m%), Jul: 0.9 vs. -0.9 exp.

Good Morning

Too hot and cold,I’m hot, I’m hot, yeah

Too hot, too hot, Too hot, too cold – Kiss

US equities extend their positive run to a fourth consecutive day with softer US economic data fuelling expectations of a Fed on hold over coming months. UST yields edged lower while European yields rose following German (falling less than expected) and Spanish (stronger) inflation data releases. The USD lost ground against EU pairs while the AUD is little changed.

It was a night of hot and cold data releases. In Europe inflation data releases surprised on the upside while in the US downward revisions to 2Q US GDP and related inflation readings, favoured the US moderation narrative.

Inflation slowed less than expected in Germany and rose to a 3-month high in Spain ahead of the Eurozone wide CPI release this evening. Germany’s HICP inflation eased to 6.4%yoy in August, one tenth lower than the previous month, but one tenth higher than expected (6.3%). Meanw

hile Spain (and Ireland) reported 3 tenths increases in the headline reading to a still modest 2.4%yoy reading, but the core reading edged one tenth to 6.1% ( vs 6.% exp.). The EZ wide inflation data release is out tonight (more below), but overnight data releases heightened concerns sticky inflationary pressures will force the ECB hand, notwithstanding evidence of a moderation in economic activity.

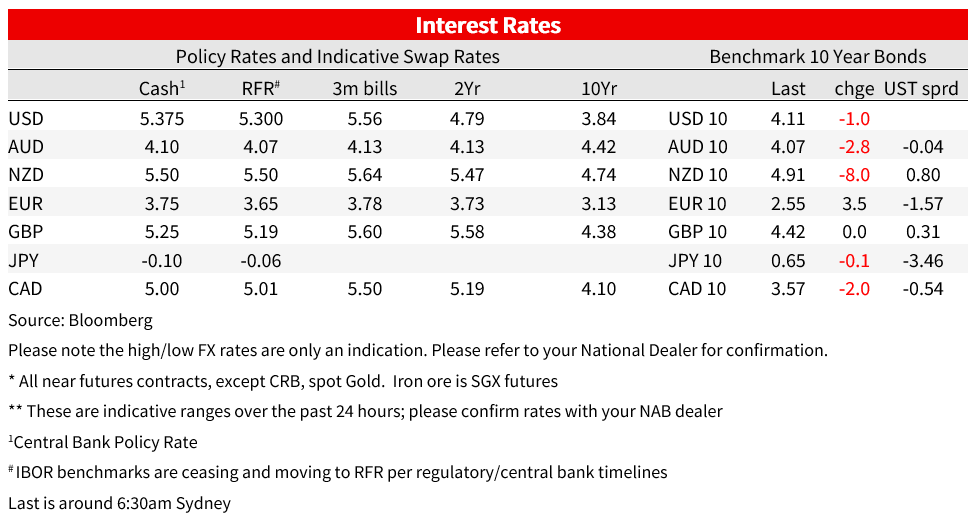

Reaction to the German and Spanish inflation data releases triggered a sell-off in Bunds with the 10y yield initially climbing 8bps, but the moved was paired back into the close with softer US data releases (more below) helping on the back of a move lower in US yields. 10y Bunds closed the day 4bps higher at 2.55% while Italian BTPS were +4 to 4.19%. ECB rate hikes expectations also ticked higher with the September meeting climbing 3bps to 13bps ( so just over 50% probability) while end of the year expectations climbed 4bps to 2

3bps

The second print of US 2Q GDP and related inflation readings surprised to the downside. Q2 GDP growth was revised down to 2.1%qoq (SAAR) from an initially reported 2.4%. Inventories flipped from a 1-tick boost to a 1-tick drag while CAPEX and trade were also revised lower. There were also downside revisions to the GDP deflator, from 2.2% to 2.0%, and core PCE price index from 3.8% to 3.7%.

After opening higher, UST yields traded lower post the US data releases with yields down ~1bp across the curve. The 10y yields now trades at 4.11% while the 2y note is at 4.885%. Market-implied expectations for Fed policy this year ended little changed, pricing in just over 50% chance of a quarter-point rate increase in November.

For the record and ahead of the non-farm payrolls release on Friday, overnight the ADP employment data release provided yet another piece of evidence of a cooling US labour market . The August number revealed an increase of 177k jobs, below the 195k expected and the slowest pace in 5 months. The ADP series is no longer a reliable predictor of what non-farm payrolls will do, but given recent softer than expected US labour market data releases (for instance JOLTs data earlier this week), the overnight release played with the grain of a moderation in labour market tightness.

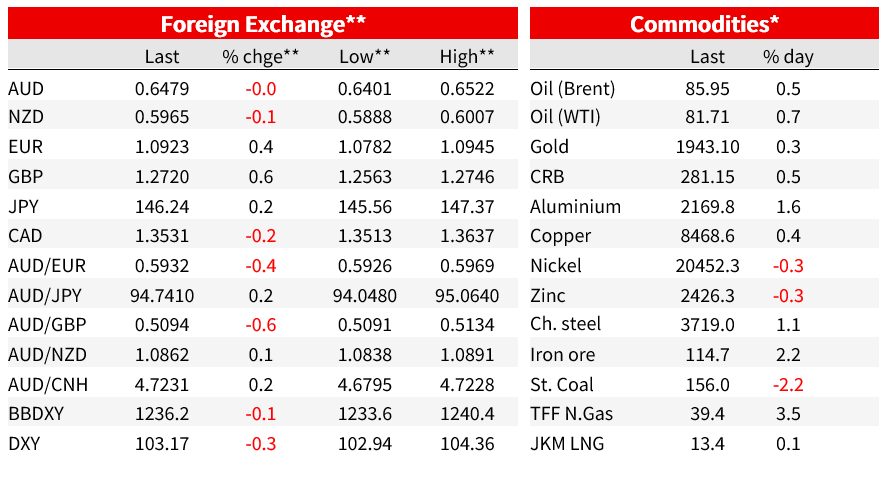

Moving onto FX, the USD was a tad weaker extending its decline to a third day in a row for both BBDXY (-0.16%) and DXY (0.36%). USD overnight softness was mainly due to strength in European currencies with the euro climbing 0.4% to 1.0922 while GBP gained 0.44% to 1.2717 , Euro gains benefited from the uptick in ECB rate hike expectations. USD/JPY is little changed near 146.20 consistent with the subdued moves in UST yields.

The AUD is little changed over the past 24 hours, starting the new day at 0.6475, but of note the pair traded to an overnight high of 0.6522 while yesterday’s lower than expected monthly July CPI only elicited a short-lived pullback . Australia headline July CPI printed lower than expected but in line with NAB’s call. The monthly reading in July is goods heavy, so some caution is needed when interpreting the decline to 4.9%yoy from 5.4%. Excluding volatile items (energy and Food) the decline in annual inflation was more subdued at 5.8% in July, compared to 6.1% in June. Housing inflation was also a mixed picture with some ease in building materials while rents rose 7.6%yoy vs 7.3% previously. Also worth adding that electricity prices rose 15.7%, these numbers include rebates introduced in July, but in August we might get a bigger kick (ex- rebate the number was 19.2%). Overall, the decline in the headline reading is welcome news for the RBA, but we are mindful that bigger price pressures are likely in August and September. For one these readings will be more services heavy and two, the energy/electricity jump is still working its way through. Then one further known unknown is the impact from wage increases on services inflation, thus we remain wary of higher inflation prints over coming months.

NZD/USD spiked above 0.6000 in line with the weaker US Dollar, but the move proved short-lived and the kiwi retraced to be largely unchanged in the offshore session . Yesterday the RBNZ announced than it had sold a net NZ$4 billion during July to build foreign reserves noting also that it wasn’t an intervention. My BNZ colleague Stuart Ritson notes that an updated FX reserves framework was published in January which outlined that an increase in reserves was required. Despite the transaction, the NZD outperformed within the dollar bloc currencies and on the major cross rates in July.

Coming Up:

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.