Total spending grew 0.9% in June.

The current debate in Markets is whether the Fed would be willing to let the economy slip into recession to tame inflation.

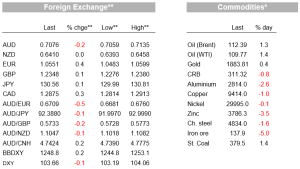

Another wild ride in markets on Friday with the US10yr yield closing at 3.13%, while the S&P500 fell ‑0.6% for its fifth consecutive week of decline. The USD was mixed with the narrow DXY -0.1%, while the broader BBDXY was +0.2%. A mixed US payrolls report did little to assuage views of a hot labour market, though average hourly earnings did come in one-tenth softer than expected. Fed officials speaking post the data came across as hawkish and signalled a willingness/need to take policy into restrictive territory. Meanwhile the weekend press is filled with bearish commentary galore. This week gives little reprieve. The US CPI will be key for the inflation pulse, but could be downplayed if moderation is shown given ongoing supply chain pressures stemming from Russia/Ukraine and China’s zero-COVID policy. Note several companies on Friday issued profit warnings on both sales and supply (e.g. Adidas and Under Armour).

As for Friday’s Payrolls, it was a mixed report and did little to assuage the view of a hot labour market. Headline payrolls beat at 428k vs. 380k expected and the unemployment rate was unchanged at 3.6% (3.5% expected). The prior two months of job gains though were revised down by 39k, leaving the 3m average at a still strong 523k. Meanwhile average hourly earnings were one tenth softer than expected at 0.3% m/m (vs. 0.4% expected), but the prior month was also revised higher by one tenth which left the annual rate at an as expected and still high 5.5% y/y. In three month annualised terms average hourly earnings growth is starting to slow (currently 3.7% from the 6% pace last year), but it is too early to be definitive. Fed Chair Powell recently described the labor market as “tight to an unhealthy level ” with the ratio of job openings for every unemployed person sitting at 1.9, so on net this data does little to change that view.

Fed talk in the wake of payrolls highlighted more aggressive action is likely, though most Fed speakers did not see themselves as being significantly behind the curve. Bullard re-iterated his view that a rate closer to 3.6% was needed in coming quarters (“I want 3- 3½ expeditiously, then at that point we can see where we are. Then we can still if inflation expectations are still going the other way”), while Barkin didn’t rule out a 75bp hike if needed (see: Bullard: Is the Fed ‘Behind the Curve’? Two Interpretations; and MNI: Fed’s Barkin Says Hikes Not On Set 50BP Course). As for how far behind the curve the Fed may be, the Fed’s Bullard noted “credible forward guidance means market interest rates have increased substantially in advance of tangible Fed action…and the Fed is not as far behind based on this definition. ” Governor Waller and Kashkari also made a similar points in their remarks.

Important for markets is the current debate on whether the Fed would be willing to let the economy slip into recession to tame inflation. Recently departed ex-Vice Chair Quarles said that “ this is an institution from top to bottom that knows that the one great sin that will be remembered by everyone 50 years later is if you let inflation get out of control. And my young security guard did not remember what the unemployment rate was in 1971. He knew that Arthur Burns let inflation get out of control and that will drive the commitment of the committee…”. Quarles’ words are all the more pertinent given he was speaking alongside Bullard and Waller. (2) Kashkari also noted separately that “ if they [supply chains] don’t unwind quickly or if the economy really is in a higher-pressure equilibrium, then we will likely have to push long-term real rates to a contractionary stance to bring supply and demand into balance” (see Kashkari: Policy Has Tightened a Lot. Is It Enough?).

The S&P500 fell 0.6% on Friday and is now -14.6% away from its peak. Investors are no doubt trying to work out where the Fed put is in this cycle. With inflation high, the put is likely lower than where it was previously. Additionally with financial conditions being a key transmission mechanism for monetary policy, equities may need to fall to tighten financial conditions sufficiently (a point repeatedly stated by former NY Fed President Dudley). On equity market sentiment, the WSJ has one interesting article, noting option volumes in single stocks recently hit the lowest level since April 2020 and that flows into inverse ETFs (i.e. short equity ETFs) are their highest in a decade (see WSJ: Market’s 2022 Slide Has Already Changed Investor Behavior). Meanwhile BofA analysis finds although retail money has just started to flow out of equities, it is still very small relative to inflows seen during the pandemic.

Meanwhile Adidas and Under Armour reported weak sales with China’s zero-COVID weighing on results. Adidas said its sales shrank by 3% worldwide, while profit from continuing operations fell 38%. In Greater China, sales collapsed by 35% in the first quarter. Under Armour also reported a 14% drop in Asia-Pacific Sales. Chinese Premier Li Keqiang warned on Saturday of a “complicated and grave” employment situation amid zero-COVID. China’s restrictions are also hitting commodity markets with industrial metal prices all weaker despite tight inventory levels. Copper was -0.8% on Friday and -3.6% on the week, zinc and aluminium were also down on the week at -8.2% and -6.1% respectively. Saudi Arabia has also reportedly cut oil prices to Asia due to waning demand. Oil prices though on Friday rose, gaining around 1.5%, with the market concerned about tight supply and the EU’s proposed ban on Russian oil imports. It is unclear whether the EU ban will go ahead, but G7 leaders are set to pledge to ban the import of Russian oil.

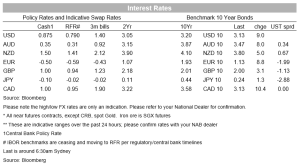

Global yields meanwhile continued to march higher with the US 10yr +9bps to 3.13%, and over the past week the 10yr has risen by 19bps. The 10yr is now within striking distance of the 2018 peak of 3.26%. The lift in the nominal yield has been more than fully reflected in real yields with the 10yr TIP yield at 0.26% after having risen by 28bps over the past year. The implied 10yr inflation breakeven in contrast is at 2.86% having fallen by 7bps over the past week. Curves meanwhile continue to bear steepen with 2s10s at 38.5bps. In Europe the German 10 year Bund yield rose to the highest since Aug 2014 at 1.13%, while Italian BTP spreads are above 200bps for the first time since April 2020. ECB rhetoric was hawkish with the ECB’s Villeroy saying it was “reasonable ” to take the deposit rate, currently -0.5%, back above 0% by the end of the year. The market, emboldened by the ECB’s shift in stance, now expects the first hike in July and another 3.5 hikes by year end. The hawkish ECB comments helped the EUR stabilise ending at around 1.0550.

Across the channel, the possibility of recession is high in the UK. BoE Chief Economist Hugh Pill spoke Friday, noting “just to be clear about it, over the next 18 months, the squeeze in real income is a very large squeeze, reflecting the very large shock to the economy .” The corporate debt market is also adding to a cautionary tale with a measure of risk in the sterling junk bond sector, which comprises mainly local borrowers, rising above 500 basis points this week, the highest since November 2020. GBP currently trades at 1.2340, having fallen 2.0% over the past week to be the worst performing G10 currency pair. The AUD meanwhile was down on Friday (AUD -0.1%) but managed to be one of the few currencies positive over the week up 0.2% against the USD. The USD indexes meanwhile remain at 20 year highs given the weakness in EUR (1.0555) and Yen (USD/Yen 130.50) and GBP (1.2362). Troubles in crypto land point to an ongoing message of caution. Bitcoin fell below $35,000 Saturday, along with a host of other cryptocurrencies.

Finally in Australia, last Friday’s RBA May SoMP was broadly in line with the messaging from Governor Lowe on Tuesday of “further increases in interest rates will be necessary over the months ahead ” and of the cash rate lifting to around 2.5% over the next few years. The forecasts in the SoMP though highlights the risk that the RBA front loads its hiking cycle given core inflation is only forecast to get to within the 2-3% band by mid-2024 at 2.9% y/y, at which point wages growth is forecast to be running at 3.7% y/y. Governor Lowe last Tuesday seemingly indicated a preference for 25bp moves, but a sharp acceleration in wages data in the WPI on 18 May could push the RBA to a supersized 40-50bps, as could a higher-than-expected CPI print on 27 July. We calculate the RBA is expecting 0.7% q/q for WPI and 1.3% q/q for Trimmed Mean CPI.

Quest domestically with nothing scheduled. Offshore the only thing item of note is China’s Trade Balance:

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.