Firmer consumer and steady outlook

Insight

US Consumer Sentiment fell further than expected to be at its lowest level since August 2011 and with consumer confidence so low, the risk of recession is rising.

https://soundcloud.com/user-291029717/one-day-when-fears-eased-for-a-bit?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Equities bounced on Friday, though given their heavy falls earlier in the week US stocks still finished the week in the red. Helping drive more positivity was news that Shanghai was planning to start easing COVID restrictions this week as well as some consolidation in yields after their relentless rise. Perfect grounds for a squeeze, but the overwhelming sentiment remains bearish with markets starting to shift focus from inflation concerns to recession fears. The S&P500 rose 2.4%, but was down by the same amount for its sixth consecutive week of decline. Since peaking last year it has fallen by 16.1%. You have to go back to 2011 to find another six week period of declines. Yields rose with the US 10yr +7.1bps to 2.92% and on the week, are down -21bps. Fed talk remains hawkish despite the yield moves.

While Shanghai provided some positivity for markets, it is not clear when China will pivot to living with Covid. The mayor of Shanghai said the city was aiming to start an “orderly opening-up ” by May 20th, which provides some light for global supply chains. The first stage of this process has been unveiled over the weekend, with supermarkets, department stores, hairdressers, and pharmacies, to be gradually reopened from today. However, whether Shanghai can remain lockdown free (and whether Beijing can avoid it) is another matter. One ominous sign was China on the weekend announcing it has relinquished the rights to hosting the Asia Soccer Cup in mid-2023. Given 10 stadiums had already been constructed or renovated for the competition, it may suggest some fear amongst policy makers that China will struggle to pivot towards living with COVID.

The negative impact of the zero-COVID policy on China was clearly visible in Chinese credit data for April . Aggregate financing was 910.2bn, well short of the 2,200bn expected by markets, and was its lowest level since February 2020. The fall in aggregate financing is a natural consequence of enhanced restrictions and illustrates how hard it is to stimulate an economy that is still running a zero-COVID policy. A further update on the health of China’s economy will be seen in today’s activity figures, with Retail Sales, Industrial Production and Fixed Asset Investment all out. There is also talk that the PBOC might cut its medium-term financing rate today, but the mooted 10bps reduction suggested by some economists is hardly going to move the needle for the economic outlook.

US Consumer Sentiment fell further than expected, down a sharp -9.4% to 59.1 (consensus 64.0), to be at its lowest level since August 2011. Declines were broad based for all demographic groups. Notably buying conditions for durables reached its lowest reading since the question began appearing on the monthly surveys in 1978. The same plunge is being seen in the home-buying index which has plummeted over recent months to be at its lowest level since 1982 – significantly higher mortgage rates and elevated prices the likely factors. These sentiments are being felt in the equity market with the Dow Jones Home Builder Index now -29.8% from its peak along with the S&P500 Retailing sub-index at -30.9%. Encouragingly for the Fed though, inflation expectations were broadly steady with he importantly 5-10yr expectation remaining at 3.0%, having been in a range of 2.9-3.1% over the past 10 months.

With consumer confidence so low, recession risk is rising. A Bloomberg survey of economists showed the probability of a US recession within the next year was seen at 30%, up from 27.5% in April and double what was polled three months. The current chair of Goldmans Blankfein has also added his voice to the debate, noting that “It’s definitely a risk,” and “ If I were running a big company, I would be very prepared for it. If I was a consumer, I’d be prepared for it, but it’s not baked in the cake.” Financial conditions are tightening, and while not at high levels, the Goldman’s gauge is up 2.2 percentage points over the past year with there only having been three periods when conditions tightened faster – namely 2001, 2008 and 1984.

Fed speak meanwhile remains hawkish. The Fed’s Mester while supporting two further 50bp hikes in June and July, noted that if by September “…inflation has failed to moderate, then a faster pace of rate increases may be necessary”. The market should be in no doubt of the Fed’s resolve to lower inflation, with Mester noting: “ the FOMC will be aiming to calibrate our policy to bring demand better in line with supply, thereby putting inflation on a downward trajectory toward our 2 percent goal”. (see Mester: The Great Recalibration of U.S. Monetary Policy ). Not widely reported on because it came out last Thursday after the close was an interview with Fed Chair Powell where he also took a hawkish line, taking some sugar coating off a soft landing, noting “whether we can execute a soft landing or not, it may actually depend on factors that we don’t control” (see Powell: interview transcript with Marketplace ). Hawkish rhetoric appears to be working with the 10yr implied inflation breakeven falling 12.7bps over the past week to 2.74%.

Across the pond the ECB also has turned modestly hawkish with the ECB’s Hernandez stating on Saturday the the ECB will likely decide at its next meeting to end its stimulus programme in July, and raise interest rates “very soon” after that . European political news continues to suggest sizeable headwinds with the FT reporting the EU was optimistic it could convince Hungary, with financial incentives, to sign up to a proposed Russian oil embargo. Hungary, alongside Slovakia and the Czech Republic, has been holding up the planned oil embargo, even though the EU has offered it a longer transition period to phase out Russian oil imports. Oil prices jumped 3.8% on Friday, with Brent at $111.55. Tensions with Russia do not appear to be abating anytime soon with and both Finland and Sweden confirmed they would apply for NATO membership.

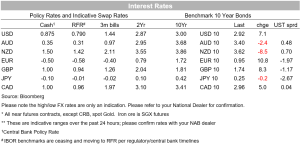

As for FX, Friday saw some retreat of safe-haven trades as risk rallied. Commodity currencies rallied over 1% with the AUD +1.1% to 0.6940; USD/CAD -0.9% to 1.2929; USD/NOK -1.1% to 9.77; and NZD +0.5% 0.6276. The USD which had reached a 20-year high on Thursday on a DXY basis fell -0.3% with gains in both GBP (+0.5% to 1.2262) and EUR (+0.6% to 1.0412). The EUR though did fall to as low as 1.0350 at one stage, bouncing once broader risk sentiment turned. USD/Yen while increasing 0.6%, mainly reflected the rise in US yields with the US 10yr +7.1bps 2.92%. Over the past week the AUD has been the worst performing G10 at -1.9% and reflects that while sentiment turned higher on Friday, sentiment overall likely remains fragile.

Australia: Wages data for Q1 the focus in a week that also sees Employment for April and the RBA May Meeting Minutes. For wages we pencil in 0.7% q/q and 2.4% y/y (consensus 0.8/2.5). An upward surprise would show wage pressures having been more prevalent than the RBA thought in May, increasing the risk of a supersized 40-50bp rate hike in June. NAB’s 0.7% q/q wages forecast is broadly in line with the RBA’s May SoMP and is consistent with a 25bp move. As for labour market data, we see the unemployment rate declining from its current 4.0% (3.95 unrounded) to 3.8% on the back of a 40k employment gain in April (consensus 3.9/30k). The RBA May Minutes might also give further details on the RBA’s shift to hiking rates and whether supersized rate hikes are on the table.

Offshore:

There is nothing of note domestically. Offshore the focus will be on Chinese activity figures (see above for details). The US also has the Empire Fed Manufacturing Survey, while the Fed’s Williams is in a moderated discussion at an event hosted by the Mortgage bankers Association in New York.

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.