We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

The UK's unemployment rate fell to it's lowest level since 1974 and along with a further pickup in average earnings growth, now see money markets pricing 125bps of BOE rate hikes by December.

https://soundcloud.com/user-291029717/china-reopening-americans-shopping-brits-working?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

The positive vibes from our APAC session extended overnight supported by mostly solid US data releases. US and EU currencies have enjoyed a decent rebound, notwithstanding a decent move in core global bond yields. ECB’s Knot opened the door to a 50bps rate hike if inflation risk worsened while Fed Chair Powell reiterates urgency to bring inflation down, no matter how painful. EU currencies lead gains against the USD while AUD trades back above 70c.

Hopes of an ease in Shanghai restrictions lifted sentiment during our APAC session yesterday with regional indices and US equity futures turning positive. Chinese tech stocks led the gains amid expectations Beijing could dial back some of its clampdown on the industry. These positive vibes extended into the overnight session, supported by a number of positive economic reports across the US, Europe and UK.

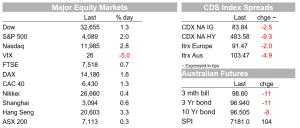

The Hang Seng closed 3.27% higher, China CS1 300 was 1.25% and then overnight regional EU equity indices close up between 0.70% and 1.60% with the Stoxx 600 index gaining 1.22%. Meanwhile in the US, the NASDAQ has led the gains, up 2.76% while the S&P 500 closed 2.02% higher.

Yesterday Shanghai reported no new Covid-19 infections in the broader community for a third consecutive day, hitting a crucial milestone needed for authorities to ease restrictions. A positive development, but China remains without an effective covid vaccine so it remains to be seen what exactly these ease in restrictions will look like and mean for activity . Worth noting too that it hasn’t been all good news as new outbreaks are also occurring like in Tianjin and Guang’an, while another district in Beijing has gone into lockdown after a new cluster of infections was found.

Sticking with the covid news, New York City raised its alert level from medium to high amid increasing pressure on the health care system. The guidance now is that face masks are worn in all indoor settings and crowded outdoor settings.

As for the overnight data releases, US April retail sales rose 0.9%, very close to the consensus, 1.0% while sales ex-autos rose 0.6%, a bit above the consensus, 0.4%. Revisions however were very strong with the March data now showing a 1.4% gain (previous 0.5%). In April, headline sales were flattered by a 2.2% increase in auto sales while gains in the core number were broad based. Notwithstanding the increase in prices, the use of savings and credit are helping maintain a strong US consumption pattern.

US industrial production also came in much stronger than expected, rising 1.1% m/m in April. Bucking the trend however, the NAHB index of homebuilder sentiment and activity fell to 69 in May from 77, well below the consensus, 75 . Higher US mortgage rates (up over 200bps since last September) are finally weighing on homebuilders sentiment. More of the same likely to come.

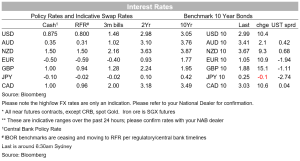

Meanwhile, the UK’s unemployment rate fell to 3.7 % in Q1, the lowest level since 1974 . There is no doubt the UK labour market is tight with still unremitting growth in the demand for labour , reflected by vacancies (Feb-Apr) up to a new record of 1.295m, for the first time since records began, there are fewer unemployed people than job. There has also been a further pickup in earnings growth, headline average earnings (incl bonuses) jumped from 5.6% (revised up from 5.4% to 7.0% (f/c 5.4%). The latter has been an issue for the BoE, noting a desire to see an ease in wages/earnings growth. Money markets now price 125bps of BOE rate hikes by December, equivalent to five quarter-point hikes at every policy decision this year.

We have had a few speakers overnight, but Fed Chair Powell has been the highlights. Powell repeated his hawkish remarks noting that inflation needs to fall in convincing way and that there could be some pain involved as “growth has to move down” for inflation to come down . Adding a bit more fuel to his hawkish remarks, Powell reiterated 50bps hikes are on the table adding the Fed ‘won’t hesitate’ to hike rates above neutral if needed.

Meanwhile in Europe, overnight ECB Knots said he supports a quarter-point increase in July but a 50bps hike may be justified if data show inflation worsening. Money markets priced in 106bps of tightening by December after the comments, compared to 86 bps at the end of last week.

The hawkish remarks from Fed and ECB speakers played into the bear flattening in core global yield curves as the increase in rate hikes expectations drove an increase in yields led by the front end. 2y Gilts rose 20nps to 1.416% while 2y and 5y UST yields climbed 13bps to 2.701% and 2.954% respectively. Meanwhile 10y bunds rose 10bps to 1,04% while 10y UST yields gained 9bps to 2.986%.

Moving onto FX, EU currencies led the gains against the USD overnight with the euro rallying 1.05% to 1.055, boosted by ECB Knots remarks while GBP gained 1.32% to 1.2493 with most of the gains coming after the strong labour market data. The AUD continued its recent ascendency, up for a third day in a row, overnight the pair found some resistance around the 0.7040 mark and now trades at 0.7029 (up 0.62% over the past 24 hours). The NZD caught the risk sentiment tailwind, driving up to about 0.6375, before falling back to 0.6355, modestly higher than the NZ close.

In other news, talks between Russia and Ukraine to end the war are on hold with both sides blaming each other for the stalemate. Russia said Ukraine has “practically withdrawn” from the negotiations, while Kyiv blames Moscow for failing to compromise. Meanwhile, the Biden administration is poised to fully block Russia’s ability to pay US bondholders after a deadline expires next week, a move that could bring Moscow closer to the brink of default.

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.