NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Although employment growth disappointed yesterday, and along with wages data from earlier in the week, remains consistent with a rate rise of 25bp by the RBA in June.

https://soundcloud.com/user-291029717/who-can-slow-down-the-slowdown?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

No bounce was forthcoming in US equities after yesterday’s sharp falls as risk sentiment remained under pressure. The market moves paint a picture of a US focus to growth fears. US yields were lower, led by the short end, while the US dollar softened. The dollar depreciated against each of its G10 peers and was 0.9% lower on the DXY. Second-tier US data on the soft side wasn’t helpful.

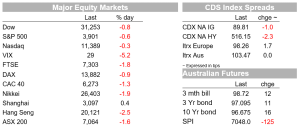

US equities wavered in an out of positive territory in Thursday’s session. The S&P500 closed 0.6% lower after being up as much as 0.6% going into the last hour of trading, the VIX remaining elevated at around 30. Cisco was down 14% after missing earnings expectations. Earlier, Asian and European bourses took their lead from the selloff in US markets on Wednesday. The Euro Stoxx 50 was 1.4% lower, while the Nikkei lost 1.9%.

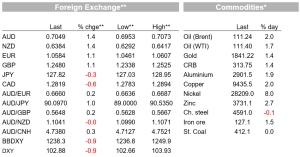

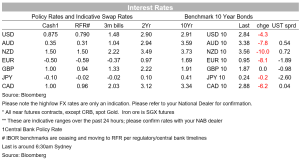

In currency markets, some of the gloss came off the US dollar. Most G10 currencies gained over 1% against the dollar, while the CAD and yen still managed smaller gains. The 0.9% decline on the DXY took the index to 102.88, its lowest level since 5 May. The AUD rose 1.4% after ending yesterday near its intraday low of 0.695. The aussie is currently around 0.705, after hitting an intraday high of 0.7073. US yields were lower and the curve steeper. The 2yr down 6bp to 2.61%, while the 10yr dropped 4bp to 2.84%.

Data flow overnight was very much second-tier, but a couple of US releases came in on the softer side of expectations and did nothing to help the mood. US existing home sales fell 2.4% to 5.75m, the third consecutive decline and further evidence of a response to higher mortgage rates. Prices, in contrast, are yet to roll over, in part because inventory on market remains low. The May Philadelphia Fed Index fell to 2.6 from 17.6, much softer then the 15 expected. That follows a very soft NY Empire State survey. But the detail made for much less gloomy reading than the headline with, among other things, new orders were up to 22.1 from 17.8. Also of some note was an increase jobless claims to 218k, a third consecutive rise. That’s still an historically low number, and its too early to take that as a signal of deteriorating labour market conditions.

Also of some interest were comments from the Kansas Fed’s George, who acknowledged “a rough week in equity markets” but consistent with other recent Fed commentary remained undeterred, saying she is ‘very comfortable’ raising rates by 50bp. George said that she would need to see something ‘very different’ to do more that.

The ECB minutes read as a historical document given the shift we have seen in ECB commentary recently. The tension produced by the limits of central banks’ ability to respond to supply side drivers of inflation was evident. The minutes noted some members viewed it as important to act without undue delay, while others felt that “adjusting the monetary-policy stance too aggressively could prove counterproductive.” Of note was confirmation that a July hike after a June end to asset purchases would be consistent with guidance, with the minutes reiterating that “some time ” meant one week to several months: “the approach did not prevent a timely rate rise if conditions so warranted”

Australian employment data yesterday saw the unemployment rate print in line with expectations at 3.9%, helped by a surprise decline in the participation rate even as employment growth disappointed at just +4k in the month. Although employment growth disappointed, the data is still consistent with a tight labour market and the unemployment rate is the lowest it has been since 1974. In conjunction with the wages data earlier in the week, the data flow looks consistent with a rate rise of 25bp by the RBA in June.

Early in our time zone yesterday Japan’s trade figures showed a slower-than-expected rise in exports. Exports were up 12.5% from a year, slowing from 14.7% in March and short of the 13.9% growth expected. Imports were up 28.2% y/y, also slower than the forecast 35% gain but still enough to see the trade deficit widen to its largest since 2014. The slower exports growth likely reflects some spillovers from China, both due to lower demand and constrained supply of inputs.

In other news, China is reportedly in talks with Russia to replenish its strategic crude oil reserves, taking advantage of discounted Russian oil. That would be a sign of strengthening energy ties between the two countries and could mute the impact of European efforts to limit Russian oil exports. Biden backed Finnish and Swedish bids to join NATO in a meeting yesterday, but Turkey has signalled it won’t support the countries’ membership. The US Senate approved $40bn in fresh assistance for Ukraine.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.