NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

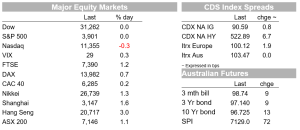

A more positive risk backdrop begins the new week. US equities are higher, the S&P500 up 1.9%, extending a turnaround after dipping into bear market territory intraday on Friday.

https://soundcloud.com/user-291029717/hope-springs-eternal-well-for-today-anyway?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

A more positive risk backdrop begins the new week. US equities are higher, the S&P500 up 1.9%, extending a turnaround after dipping into bear market territory intraday on Friday. Comments by President Biden that removal of China tariffs were under consideration is one oft-cited potential driver, but it should be said the broader news flow appears very much mixed. ECB President Lagarde signalled an end to negative rates in the third quarter.

The positive start to the week for equity markets comes after 7 consecutive weeks of declines. Financials led gains, the sector gaining 3.2% and helped by 7.3% gain for JP Morgan Chase on the back of updated guidance that painted a more positive picture for the near term credit outlook. Gains were seen across industries. The Dow added 2.0% and the Nasdaq was 1.6% higher. European equities were also higher, the Euro Stoxx 50 up 1.4%.

China-sensitive equities were an exception, the Hang Seng losing 1.2%. Concerns about Covid spread and the risk of tighter containment measures were stoked by an increase in recorded cases in Beijing . The city recorded 99 infections for Sunday, up from 61 on Saturday. While the total is still low, the daily increase is one of the biggest since the outbreak started. The case numbers have mostly hovered around 50 a day. On the other side of the coin, there was also news that China plans additional support for the economy, offering $21bn in additional tax relief. The additional tax cuts are worth about 0.1% of China’s GDP and are targeted mostly at businesses. The new announcement takes the government’s total planned reduction in taxes this year to a little above the relief Beijing offered in 2020 when China was first hit by the pandemic

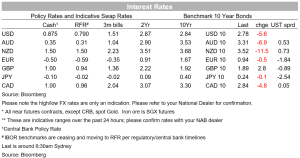

Yields were generally higher. The US 10yr yield was up 8bp to trade around 2.86%, while the two year was 5bp higher at 2.63. European yields were also higher, the German 10yr up 7bp at 1.02%. A stronger than expected showing from the German IFO adding to Lagarde’s comments to set the tone. The IFO rose to 93.0 points in May from a revised figure of 91.9 points in April. That was led by current conditions at 99.5, up from 97.3, painting a picture of resilience rather than recession, though the expectations component remaining mired around 86.9 reminds of the significant headwinds still in play.

ECB President Christine Lagarde added her voice to the chorus of ECB officials pointing to a July rate rise. Lagarde wrote in a blog post that “ I expect net purchases under the APP to end very early in the third quarter. This would allow us a rate lift-off at our meeting in July, in line with our forward guidance. Based on the current outlook, we are likely to be in a position to exit negative interest rates by the end of the third quarter.” Moving out of negative rates appeared to be the immediate intention, with Lagarde adding that the ‘next stage of normalisation’ would depend on whether the ECB sees inflation stabilising at 2% over the medium term. Lagarde emphasised gradualism, optionality, and flexibility; at pains to remind readers that a negative supply shock complicates the monetary policy response. While adding her voice to a July rate rise, the discussion didn’t point to a rapid pace of tightening. Bloomberg reports that ‘irked’ some unnamed colleagues who want to keep open the option of moving faster.

In other central bank commentary, the Fed’s Bostic said that a soft landing was the Fed’s goal but was ‘incredibly hard’ to achieve. He, like most every other Fed official, said he was comfortable with 50bps at the next couple of meetings. He also said that it may make sense to pause in September but that further increases would be on the table if inflation remains too high. BoE Governor Bailey said that the BoE is prepared to raise rates again if needed, but again pointed to the scale of the external shock and that the size of the income shock needs to be taken into account. Locally yesterday, the RBA’s Kent spoke on the evolution of the RBA’s asset purchase program towards QT, reiterating the point that “increases in the cash rate are the tried and tested measure that will do most of the work, including because they can be easily calibrated to evolving economic condition”

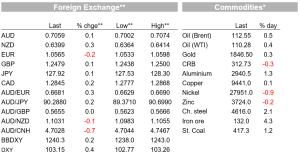

As for currency markets, in keeping with the broader risk positive tone, the US dollar softened against all of its G10 pairs except the yen. The dollar was down 1.0% on the DXY. Gains were led by European currencies, the euro up 1.2% and the SEK and NOK managing larger gains still. The AUD was 1.0% higher, hitting an intraday high of 0.7127 and currently sitting around 0.7102. President Biden’s comments on the potential removal of tariffs on Chinese goods helped the RMB 0.6% higher, the aussie also seeing a boost on the headline.

On tariffs, Biden said “We did not impose any of those tariffs. They were imposed by the last administration and they’re under consideration .” Markets seemed to take the news as indicative of a potential thawing of US-China trade tensions, though it isn’t the first time tariff reductions have been floated. While a cut to tariffs would help soften US inflation at the margin, reports suggest administration officials are concerned about appearing soft on China ahead of November congressional elections. As for the direct implications for the US inflation outlook, analysis by the Peterson Institute puts the effect in the order of 0.25ppt, Chinese import content accounting for around 2% of the CPI basket (See Russ, PIIE).

That wasn’t the only headline to come from President Biden’s presence in Asia . President Biden also unveiled the Indo-Pacific Economic Framework. An initiative including 13 countries including Japan, Australia, New Zealand, South Korea India and seven south-east Asian nations. The framework would have 4 pillars (trade, supply chains, clean energy and infrastructure, and tax and anti-corruption) though has received a lukewarm response in many countries because unlike a traditional trade agreement did not provide US market access. Third, Biden at a news conference for again added ambiguity to the longstanding policy of strategic ambiguity in regards to Taiwan. Biden replied “Yes. That is the commitment we made,” when asked whether he would be willing to use force to defend Taiwan. The White House insisted US policy was unchanged.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.