Online retail sales growth slowed in May following a fairly strong April

Insight

Risk sentiment rallied on Friday with a better than expected US retail sales print and positive earnings from Citigroup lifting equities

https://soundcloud.com/user-291029717/a-good-friday-but-a-crunch-week-for-europe?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

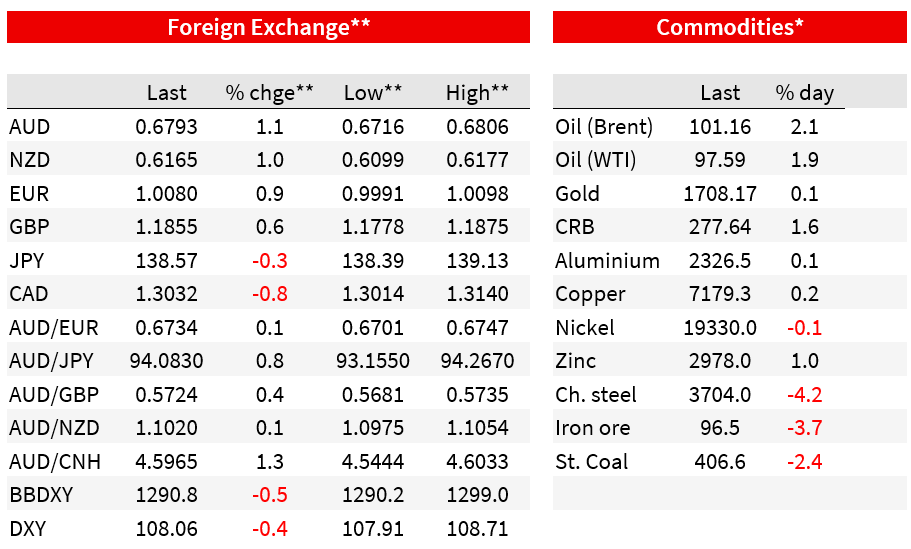

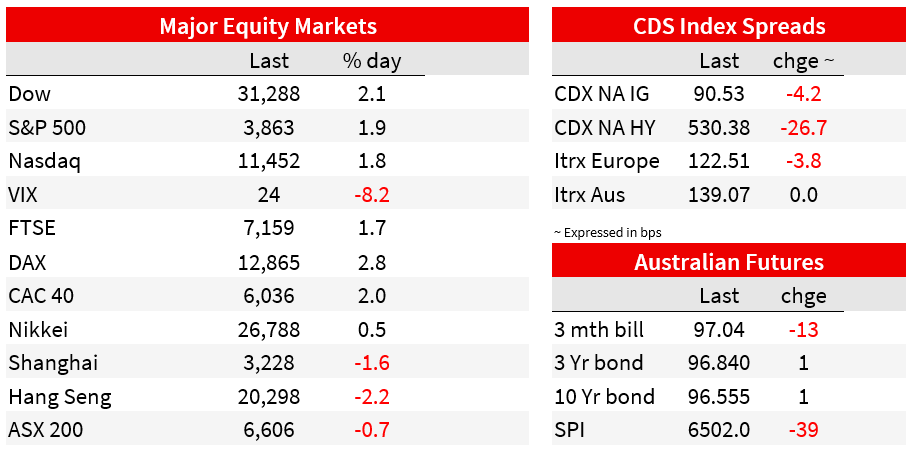

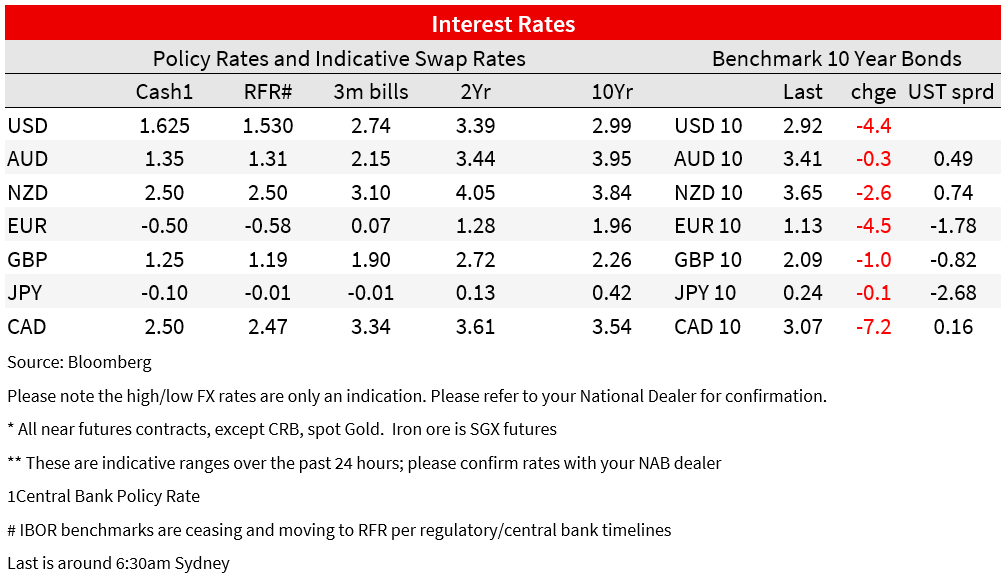

Risk sentiment rallied on Friday with a better than expected US retail sales print and positive earnings from Citigroup lifting equities, all likely exacerbated by positioning . A fall in 5-10yr inflation expectations out of the University of Michigan Survey to 2.8% from 3.1% also saw markets further reduce their pricing for a 100bp hike from the Fed, which was reinforced by the Fed’s Bostic who backed a 75bp hike after having been open to it. The S&P500 rose 1.9%, though for the week it is still down -0.9% and is around -19% away from its early January peak. Yields fell with the US 10yr -4.4bps to 2.92%, and with 2yr yields little changed the 2s10s curve inverted further to -21.3bps. Despite the positivity recession risk is very much alive with the Atlanta Fed GDP Now at -1.5% annualised for Q2, while markets continue to price the Fed overdoing the hiking cycle with 56bps of cuts price in 2023 after a peak of 3.54% in February 2023. The USD fell amidst the risk positive environment with the DXY -0.4%, but is +1.0% for the week.

The catalyst for the spike in equities appeared to be Citigroup with its shares up 13.2%. Citigroup beat expectations with earnings per share of $2.19 vs. 1.68 expected, though note profit is still lower than last year’s $2.85. Revenue rose a bigger-than-expected 11% in the quarter to $19.64 billion, more than $1 billion over estimates, driven by interest income and strong results for trading and institutional services. Overall Citigroup noted it saw little evidence so far that a recession is imminent, with the CEO noting: “while sentiment has shifted, little of the data I see tells me the U.S. is on the cusp of a recession. ” Overall though the profit reporting season has been lacklustre with FactSet noting that 7% of companies had reported so far for Q2 with 60% beating on EPS, below the usual beat of 77%. Earnings for non-financials in particularly highlight cost pressures as seen in reports by Delta and Fastenal.

The other factor driving positivity was a better than expected US Retail Sales print with core control at 0.8% m/m vs. 0.3% expected. The prior month though was revised lower to -0.3% m/m against 0.0% initially reported. A lower than expected inflation expectations read out of the University of Michigan Survey also added. The 5-10yr expectation fell to 2.8% from 3.1%, just below the 2.9-3.1% range seen in the preceding 11 months. The Fed’s Daly said the inflation expectations print was a “a good thing ” combined with comments by Bostic (see below) saw pricing for a 100bp hike in July fall to 19%. As for overall consumer confidence this was little changed at 51.1 from 51.0 and remains near all-time lows and at levels consistent with a recession. Also inflation related, import prices excluding petroleum fell ‑0.4% m/m, perhaps showing signs of the stronger USD flowing through.

It wasn’t all rosy in terms of data though, and recession risks are still alive. Manufacturing Production was weaker than expected at -0.5% m/m against -0.1% expected, and the prior month was also revised lower to -0.5%. Following the data the Atlanta Fed GDP Now tracker was updated with Q2 GDP still expected to be well negative at -1.5% annualised (see Atlanta Fed GDP Now for details). A technical recession thus still seems a high possibility, but it is a strange one with the profit reporting season so far showing that while firms are preparing for a slowdown, there is little hard evidence outside of housing and consumer/business confidence so far. Also out on the data front was the NY Empire Fed Manufacturing Survey. While current conditions were positive, forward expectations were disastrous and at levels worse than at the height of the pandemic.

Fed commentary reinforced expectations of a 75bp hike in July. The Fed’s Bostic noted he supported a 75bp hike, after having said “everything is in play for future policy decisions” after the CPI figures, noting that “moving too dramatically I think would undermine a lot of the other things that are working well.”. The Fed’s Daly also said her “most likely posture” was a 75bps hike later this month. Closely watched Fed whisperer Nick Timiraos also penned a weekend piece that seemed to suggest a 75bp hike was all but certain (WSJ: Fed Officials Preparing to Lift Interest Rates by Another 0.75 Percentage Point). Market pricing for a 100bp hike fell to 19% on Friday from as high as 63% on Wednesday.

More important Fed commentary in your scribe’s opinion was Bullard’s hawkish comments. Bullard noted the Fed may need to raise interest rates to higher levels this year than previously anticipated given the broadening out of inflation (“inflation is proving to be broader and more persistent than we would have thought even 60 or 90 days ago ” and that based on rents core PCE probably hasn’t peaked at this point), nominating a rate of between 3.75-4% by the end of the year, from his comments around 3.5% previously. That would imply around 225bps of hiking at the next four Fed meetings, meaning the Fed after hiking by 75bps in July, would continue to hike 50bps a meeting to the end of the year. Markets continue to price the Fed overdoing the hike cycle with 56bps of cuts priced for 2023 after peaking in February 2023 at 3.5%. Meanwhile the latest WSJ survey of economists 46% of economists surveys said the Fed would overtighten (see WSJ: As Fed Tightens, Economists Worry It Will Go Too Far).

In FX the USD was broadly weaker on Friday amidst the improvement in risk appetite. The DXY fell -0.4%, but is still up 1% over the past week and close to 20-year highs. A day after falling below parity, the EUR rebounded 0.9% to 1.0080 while USD/JPY eased back from 24-year highs to 138.60. The AUD was stronger on Friday +1.1% amidst the weaker USD, but was still -0.9% over the week and ended around 0.6793. My FX colleagues lowered their AUD forecasts on Friday, seeing an extended period below 0.70 with a realistic range of 0.65-0.70 with the Aussie now not seen durably above 0.70 until September June 2023.

Elsewhere the focus continues to be on China where two headwinds are becoming more evident. China’s zero covid policy is taking much needed momentum out of the economy. Q2 GDP fell -2.6% in the quarter (-2% expected) with the annual growth rate slipping to just 0.4% y/y. The government’s 5.5% annual growth target is now widely considered to be out of reach and given the zero-covid policy stimulus is unlikely to gain much traction. According to the FT there are currently 31 cities in full or partial lockdown, equivalent to around 247.5m people. The other headwind is the property sector amid people boycotting mortgage repayments for partially completed dwellings. Financial markets are pricing in pain ahead with a bond sold by China’s second-largest builder falling to 82 cents in the dollar, while equity prices for Chinese developers are down 10% on the week. The likely weak growth trajectory for China is one reason we are pessimistic about the outlook for global growth and, by extension, the AUD and NZD this year.

Australia and NZ – RBA speeches, NZ CPI:

Offshore – Nord Stream Gas; ECB; US Earnings; Global PMIs:

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.