A private sector improvement to support growth

Insight

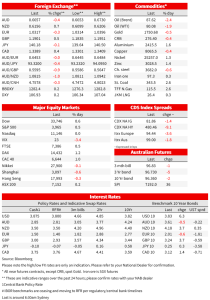

Latest Fed speak from Boston Fed President Collins, suggests 75bps is still in play for December, noting markets price around 52bps for the December meeting.

Friday was a dull day as far as data or news events were concerned. Treasury yields though did rise following hawkish commentary from the Fed’s Collins, who seemingly put a 75bp hike back on the table for December (“But 75 still is on the table, I think it’s important to say that as well”; markets have 52bps priced). The 10yr rose 6bps to 3.83%, while there was a sharper 8bps lift for 2yr yields to 4.53%. The lift in nominals was entirely reflected in reals with the 10yr TIP yield up 8.3bps to 1.57%, while the implied inflation breakeven fell -2.6bps to 2.27%. US 2/10s curve inverted further to -71.0bps, its most inverted in forty yields. The fall in breakevens partly reflected the sharp fall in oil prices with WTI -2.4% on a combination of China demand concerns, and reduced oil capacity through a US pipeline. Across the pond European debt markets saw a smaller rise in yields despite hawkish ECB commentary, with the first TLTRO repayment smaller than expected (€296bn vs. 600 expected). Equities rose in choppy trade with the S&P500 +0.5%, though did fall -0.7% over the week. The USD was firmer with higher rates giving support (DXY +0.2%) with most pairs weaker, including the AUD -0.4% to 0.6657. GBP was one exception, up 0.5% to 1.1901.

As for the week ahead, its relatively quiet with the US out for Thanksgiving on Thursday (equity and bond markets close), while markets also close early on Friday with many likely taking a long weekend too, not to mention the World Cup. Instead, markets are likely to focus on Chair Powell’s upcoming speech on 30 November on “on economic outlook and the US labor market” at Brookings. Could Powell use this again to push back against market pricing for cuts in 2023 and the lift in equity markets over recent weeks? Note flows data suggest nearly $23bn went into global equities over the latest weekly reporting period, the largest in 35 weeks. While markets price a Fed Funds Rate of 5.07% by mid-2023, they are also pricing in 41bps worth of cuts in 2023. One hint perhaps came from Bostic who spoke on the weekend, and while saying he saw a further 75-100bps worth of cuts, also pushed back against cuts (“…if unemployment rises uncomfortably — it will be important to resist the temptation to react by reversing our policy course until it is clear that inflation is well on track to return to our longer-run target of 2%”). In Australia it is also quiet with only Governor Lowe speaking on Tuesday on “Price Stability, the Supply Side and Prosperity”.

First to Fed speak which seemed to be the catalyst for the lift in yields. Boston Fed President Collins suggested 75bps was still in play for December – note markets price around 52bps for the December meeting. Colins noted: “But 75 still is on the table, I think it’s important to say that as well.” That comment by itself sounds hawkish, but Collins overall was more cautious and also expressed confidence that policymakers can tame inflation without doing too much damage to employment (see Collins: Parsing the Pandemic’s Effects on Labor Markets for details). Instead, it was likely that comment coming after a bevy of Fed Speakers during the week that added a hawkish hue to it. Recall the Fed’s Bullard on Thursday stating the appropriate zone for the Fed Funds rate could be in the 5-7% zone (see Bullard: Getting into the Zone).

The Fed’s Bostic also spoke on Saturday and while the sound bite was certainly less hawkish than Bullard (“If the economy proceeds as I expect, I believe that 75 to 100 basis points of additional tightening will be warranted”), he also pushed back aggressively on the Fed cutting in 2023 unless inflation was on track to return to 2% (“On the other hand, if economic conditions weaken appreciably — for example, if unemployment rises uncomfortably — it will be important to resist the temptation to react by reversing our policy course until it is clear that inflation is well on track to return to our longer-run target of 2%”). (see Bostic: From Academia to the FOMC: The Journey of One Fed President). Note Chair Powell is scheduled to speak on the economic outlook and the US labour market at Brookings on 30 November.

The big move on Friday and over the week was oil prices. WTI was down some -2.5% and it has fallen by more than 10% over the past week. The near-term outlook for oil has deteriorated with contango emerging (upward sloping curve) with uncertainty around China’s demand given surging COVID cases. Some traders also noted reduced capacity of Shell’s Zydeco oil pipeline which connects oil pipelines in Houston and Port Neches. As for China’s Covid surge, China recorded its first official death from the virus since May with a 87-year old man dying in Beijing. Analysts continue to cite low vaccination rates among the elderly as being a big hurdle to re-opening; only 66% of those aged 80 and above are fully vaccinated, and only 40% have had a booster. Beijing has surged residents in its most populous district (3.5m people) to stay at home on the weekend and on Monday. Chongqing is also reported to be under defacto lockdown. The press have taken a more hawkish approach to zero-Covid since mid-last week, noting China isn’t relaxing or “lying flat.”

ECB speakers were also out in force on Friday. ECB President Lagarde repeated the mantra that the policy rate might need to head into restrictive territory to drive inflation back down to target, even given the rising risk of recession, “withdrawing accommodation may not be enough”. Bloomberg reports that momentum is lacking for another aggressive 75bps hike next month and the ECB may step down to a 50bps hike, according to its sources, as long as this month’s inflation reading doesn’t produce another upside surprise. The ECB Minutes which are out this week will be parsed closely for any discussion of QT with the ECB’s Knot stating the sooner QT begins, the lower the peak inflation and terminal rate will be. Also on Friday the first TLTRO repayment came in lower than expected at €296bn against €600bn expected. The lower repayment probably explains why European yields were resilient to the rise in global yields (German 10yr -0.6bps to 2.01%).

Finally data was very second-tier on Friday with only US existing home sales which fell 5.9% m/m. Since January existing home sales have fallen by around 32%.

A private sector improvement to support growth

Insight

Online retail sales growth accelerated 1.1% in April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.