Online retail sales growth slowed in May following a fairly strong April

Insight

It has been a wild night in markets. After initially enjoying a broad and solid risk on move with equity markets rising and core global bond yields falling alongside a broadly weaker USD

Events Round-Up

NZ: REINZ house sales (y/y%), Oct: -34.7 vs. -10.9 prev.

JN: GDP (q/q%), Q3: -0.3 vs 0.3 exp.

CH: Industrial production (y/y%), Oct: 5.0 vs. 5.3 exp.

CH: Retail sales (y/y%), Oct: -0.5 vs. 0.7 exp.

CH: Fixed assets investment (y/y%), Oct: 5.8 vs. 5.9 exp.

UK: Unemployment rate (%), Sep: 3.6 vs. 3.5 exp.

UK: Wkly earnings ex-bonus (3m/y%), Sep: 5.7 vs. 5.5 exp.

GE: ZEW survey expectations, Nov: -36.7 vs. -51.0 exp.

US: PPI ex food, energy (y/y%), Oct: 6.7 vs. 7.2 exp.

US: PPI final demand (y/y%), Oct: 8.0 vs. 8.3 exp.

US: Empire manufacturing, Nov: 4.5 vs. -6.0 exp.

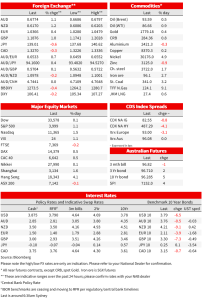

It has been a wild night in markets. After initially enjoying a broad and solid risk on move with equity markets rising and core global bond yields falling alongside a broadly weaker USD. Early this morning we have seen a partial reversal on these moves following reports Russian missiles crossed into NATO member Poland, killing two people. Poland has convened a security meeting, rattling markets. Equities reversed earlier gains only to recover shortly after, the USD has remained on the back foot with AUD and NZD top of the leader board while European currencies giving back some of their overnight gains. 10y UST yields are tad lower at 3.78%, after trading in a 10bp range.

According to Polish media outlets, two people have been killed at a grain processing facility in Przewodów, a Polish village about 10km from the border with Ukraine. The Pentagon said that they couldn’t corroborate the nature of the explosion, but media outlets have reported a senior US intelligence official confirming Russian missiles have crossed into Poland, a NATO member, killing two people.

A Polish government spokesman said top leaders were holding an emergency meeting due to a “crisis situation.”. Meanwhile as I am typing there are Twitter reports suggesting the missiles may have come from a rocket shot down by Ukraine Armed forces.

As per above, the news flow remains very hazy, but of course if the Polish attack was the results of a stray/shot down missile, it could certainly ease concern over a major escalation in the Russia -Ukraine war involving NATO.

For now, what we can say is that the news has dented what was a fairly solid risk on session. Following losses of +/- 1% in US indices Monday, US equity futures traded with a positive tone during our APAC session yesterday with the Hang Seng yet again leading the gains within regional equity indices. Investors chose to ignore the softer than expected China activity readings, probably judging that the weakness in the economic readings were yet another reason to expect Beijing to provide more support to its beleaguered economy.

Indeed, after an underwhelming economic message from the Party Congress (more focused on security and reliance than growth), there has been a clear shift in focus with President Xi leading initiatives to ease covid restrictions (more targeted approach) alongside more robust support to the property sector. Thus, against this backdrop, the softer October readings (Retail sales -0.5% y/y vs 0.7% expected and down from 2.5%. Industrial production 5.0% y/y vs 5.3% expected and 6.3% in September. Fixed asset Investment 5.8% YTD Y/Y vs 5.9% expected and 5.9% last) were mostly ignored. Clearly, investors are now more focused on the outlook than the weaker economic figures.

A softer than expected US PPI added momentum to the risk on move during the overnight session, fuelling the notion that US inflationary pressures are easing. The core measure (ex food and energy) rose 6.7 y/y the lowest since July last year, and 0.5 percentage points below consensus. The headline figure fell to 8.0%, its lowest level in over a year, after peaking at 11.7%.

In another positive news, the New York Empire State manufacturing gauge rose 13.6pts to 4.5, the first positive reading since July. This is the first of the regional manufacturing indices and follows a run of weaker ISM manufacturing figures. Not long ago, we were righting headlines that good US economic data were not good news, given a rise in activity would make the Fed’s job harder to bring inflation to heel harder. For now, the investors focus is on the softer CPI and PPI prints, but a resilient US economy does mean inflation will take longer to head back down to 2%.

On company news, Walmart beat estimates, boosted its outlook and announced a massive buyback. Walmart’s success is partially a function of high-end consumers trading down alongside a shift to groceries from general merchandise. So as my BNZ colleague, Jason Wong notes, rather than being a gauge of economic strength, Walmart’s strong result could be a sign of economic weakness, with the company’s reputation as a low-cost retailer and high inflation seeing consumers spend more on food and less on other goods and services.

Of note too, regarding inflation regarding inflation, Walmart’s CFO said the company sees prices rising more than 3% over the next year, which tops the Fed’s 2% target. Fed Vice Chair Lael Brainard just yesterday said the central bank won’t relent until it reaches its 2% target.

Looking at equity markets in more detail, the S&P 500 is recovering again, currently trading around 0.9% after opening with gains of 1.80% following the PPI news and then falling 1.90% intraday on the Polish news. The NASDAQ now trades around 1.80%, after initially opening with gains of 2.65%. Earlier in the session European shares closed in positive territory with the Stoxx 50 up 0.71%.

Global bond yields are lower overnight, initially as a softer than expected US PPI print further soothed some of the fears about the inflation pipeline – although the bond rally was arguably well in train ahead of the release so PPI may have been a marginal contributor. The 10Y UST was briefly below 3.8% a couple of times overnight. However, the 2Y/10Y UST curve has flattened through -57bp again, nearing the lows for the cycle. Comments from a bevy of Fed officials – including Harker, Fed and Bostic offered variations on theme that inflation might be easing but rate hikes were still coming.The Russian-Polish missiles news also contributed to the volatility in the rates market, 10y UST now trade at 3.7977%, after trading to an intraday high of 3.84% and a intraday low of 3.7547%.

The positive vibes from equities fuelled by an ease in US inflationary pressures weighed on the USD. The USD took a dive on the PPI release, which saw big gains in all the key majors, before reversing course . European currencies have been the big mover overnight, the euro is up 0.4% to 1.0362, but initially gains saw the pair briefly trade to an overnight high of 1.0474 with the Polish news sending the pair down to 1.0280.

. UK labour market continued to show signs of a tight labour market, despite the economy heading into recession, with chronic job shortages, not helped by a lack of immigration, and rising wage inflation. There were hints of the economic slowdown starting to bite, but still early days, with the unemployment rising only 0.1 percentage GBP has had a similar if not wilder price action. The pound now trades at 1.1874, up 1% over the past 24 hours, but this after trading to an overnight high of 1.2028 and a low of 1.1796point off its multi-decade low to 3.6%.

The AUD (0.6775) and NZD (0.6172) sit at the top of the G10 leader board, up 1.10% and 1.2% respectively. The NZD and AUD saw no backlash from the weaker China data and have powered on up, adding to last week’s strong gains. The polish news didn’t weigh too much on the antipodean with both now trading close to their overnight highs.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.