Coming in for landing in a heavy cross wind

Insight

Markets are opening up to headlines that ‘Putin puts Russian nuclear forces on ‘special alert’.

Todays podcast

Risk rallied on hard on Friday. If a key reason for this was because sanctions announced by the US and Europe fell short of what they might have been, then it is hard to see the rally surviving the early part of the week after the EU, US, UK and Canadian governments agreed to the exclusion of at least some Russian banks from the Swift global payments system, and sanction the Russian central bank , which the EU has just said means banning all transactions with them. And, if markets were trying to draw comfort from an assumption that President Putin’s ambitions begin and end with the invasion of the Ukraine and installing a puppet government, then that line of thinking is also being exposed as potentially naive (e.g. Nina Krucshcheva, Nikita Khrushchev’s great grandfather, writing in Project Syndicate at the weekend, references Stalin and Mao Zedong in relation to Putin’s ‘ego driven obsession with restoring Russia’s status as a great power…specifically the orthodox Christian Kingdom of ‘Rus, comprising Russia, the Ukraine, Belarus and the ethnic Russian area of Kazakhstan’). She concludes noting that Stalinism didn’t die until Stalin did, Maoism the same. Markets are also opening up to headlines that ‘Putin puts Russian nuclear forces on ‘special alert’. On a more positive note, are increasingly signs that Putin is not carrying the will of the Russian people with him in this (mis)adventure. Already this morning we have heard from Norway’s that its Sovereign Wealth Fund – the world’s largest – is to divest from all Russian assets. In the spirit of ‘every little helps’, so too has the NSW government.

A change of view from, importantly, Germany alongside Italy means that the US, EU, UK and Canada were able to agree at the weekend to exclude ‘some’ Russian banks from the Swift global payments/settlement system. Reference to ‘some’ suggests that for the time being, it may not be the intent to prevent certain transactions taking place, presumably in relation to oil and gas supplied from Russia in to the EU, but that remains to be seen. While not entirely clear as yet exactly what it means in practice, Russia’s central bank (CBR) has been sanctioned with the intention of denying it unfettered access to its ($643bn worth) of FX reserves. If successful, then Russia becomes impotent in defending the Rouble (assuming it can still be traded following the Swift decision). This is the first time in history that a G20 country has seen its banks excluded from Swift; Iran, Venezuela and North Kora being the only three examples since its inception in 1973.

Whether or not oil and gas will continue to flow from Russia to the EU (and can be paid for), what we did learn on Friday is that China has lifted its ban on the importation of Russian wheat (previously banned on phytosanitary, or plant disease, grounds). Does this tell us that China will now be a buyer of last (or first) resort of Russian energy and other commodity products if current buyers no longer can or will? What we do know an as per the attached report, is that the oil market was already extremely tight prior to Russia’s invasion of Ukraine, and while OPEC+ meets this week and where it would have been expected to ratify the 400,000 barrels per day of increased production from March (agreed back on February 2) remember Russia is the biggest “+” in OPEC+.

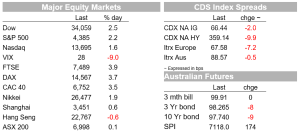

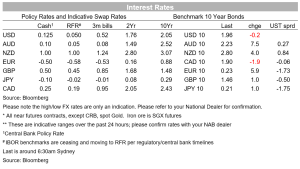

Friday saw US (and global) equity market extend the sharp turnround seen in the US market on Thursday afternoon , with gains exceeding 3% in all major European indices and the S&P500 and Nasdaq finishing with gains of 2.25% and 1.6% respectively, meaning that both benchmark US indices had an ‘up’ week, unlike all others and where the Hang Seng (-6.4%) was the world’s worst performing.

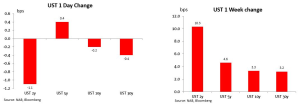

Bond markets in contrast were relatively muted , with only small small moves across the entire US Treasury curve, though were higher on the week in bear flattening fashion (2s +10bps, 10s +3bps). US Fed Funds futures ended Friday ascribing about 25% chance to the Fed lifting rates by 50bps on March 16 (at one point last week it was as slow as 10%). Fed hawks Bullard and Waller were out still gunning for 100bps of tightening by July (see below). Jay Powell might have something to say on the matter when he testifies to Congress this week.

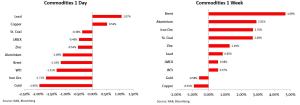

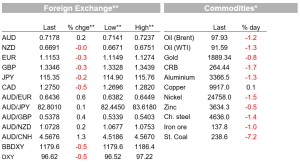

The wild ride in FX continued Friday , but where the risk-positive session meant that the USD was weaker across the (G10) board. USD/RUB had already pulled back from Its intra-day of 90 last Thursday to 84.25 at the close, and extended its gain to 83.75 on Friday. It won’t be anywhere near there today, assuming it can trade. Commodity currencies together with the SEK all fared best Friday with gains of 1.5% for NOK and 0.9% for AUD/USD to 0.7225, so back into the upper half of the YTD range of 06965–0.7314, having been as low as 0.7095 on Thursday. NOK has already fully reversed those gains in early day APAC trade, while AUD/USD is trading back below 0.72 . Improved risk sentiment, rather than stronger commodity prices, were the main driver here on Friday, with only lead and copper higher amongst the commodities we track (see chart below). Therefore whether or not Friday’s currency gains can be maintained looks heavily dependent on whether risk sentiment can hold up. We are (very) sceptical.

Economic news Friday saw, in Europe, a big upside surprise in France’s February CPI , up to 4.1% from 3.3% on an EU-harmonised basis and well above the 3.7% expected, plus a hefty upward revision to Germany Q4 GDP, from the -0.7% flash estimate to -0.3% (meaning annual growth in 2021 was 1.8% not 1.4% as first reported). France’s GDP was unrevised at +0.7%. the EC’s Economic, Industrial and Services C onfidence survey readings for February were all up on January and two out of three better that expected (Economic and Services sentiment) though these pre-date Russia’s invasion of Ukraine so need to be seen in that context.

ECB president Christine Lagarde spoke with journalists on Friday after meeting Euro-area finance minister and said that while it was too early to judge the overall economic impact of Russia’s invasion of Ukraine, persistent uncertainty will likely drag on investment and consumption and impede growth. “The ECB stands ready to take whatever action necessary within its responsibilities to ensure price stability and financial stability within the euro area,” she said. That includes ensuring that cash and liquidity will be available, and using optionality and flexibility in setting monetary policy. Her comments come after ECB Chief Economist Philip Lane earlier in the week said that conflict may reduce euro-area output by 0.3 percentage point to 0.4 percentage point this year, and Austrian CB chief Robert Holzmann who told Bloomberg that the central bank is moving toward normalization, though action might now be “somewhat delayed” because of the Ukraine situation.

In the US, Personal Income, Spending and Deflator data showed the core PCE deflator up from 4.9% to 5.2% (0.5% m/m) exactly as expected, while Income (0.0%) and Spending (2.1%) were better than the -0.3% and 1.6% consensus expectations, respectively. Durable Goods Orders rose by 1.6% in January, above the 1.0% expected with durables ex transport 0.7% against 0.4% consensus and the core ‘capital goods orders non-defence ex-aircraft’ 0.9%, above the 0.3% expected. The final UoM consumer sentiment reading came in at 62.8 from a preliminary 61.7, but the level still sits well below the Conference Board’s measure, the latter currently offering a better read on actual (strong) consumer spending. And, of some note given the recent sharp rise in 30-year US mortgage rates, Pending Home Sales fell by a chunky 5.7% on the month to be 9.1% down on a year ago.

In Fed speak, neither Fed Governor Christopher Waller nor his former St Louis Fed boss James Bullard have altered their desire to see 100bp of Fed tightening by July as a result of Russia’s invasion of Ukraine. Bullard’s said Friday that “The direct linkages to the U.S. economy are minimal so I wouldn’t expect that much impact directly on the U.S. economy”, though adds “Of course, we will have to watch this very carefully and see what happens in the days ahead”. He says “The fighting in Ukraine is something that has been around off and on for the last couple of decades, so in that sense it is not really that new. This is a bigger, more aggressive Russia here but I think the baseline expectation has to be there will not be a wider war associated with this. There are risks around that.”

And in the Fed’s report to Congress released Friday ahead of chair Powell’ testimonies to House and Senate panels on Tuesday and Wednesday this week, it re-iterates the view that “it will soon be appropriate to raise the target range for the federal funds rate,” citing inflation well above its 2% target and a “strong” labor market.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.