Confidence and Conditions Lift

Insight

Wednesday’s FOMC meeting continues to reverberate through markets.

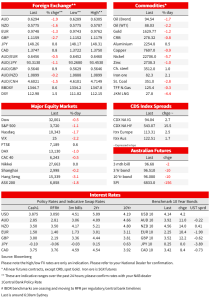

Wednesday’s FOMC meeting continues to reverberate through markets. Peak Fed Funds Pricing has lifted further to a peak of 5.14% by June 2023, building on yesterday’s post-FOMC 5.08% and well up on pre-FOMC levels of 5.05%. The short-end has borne the brunt of this re-pricing with 2yr yields up 8.6bps to 4.71%, while the 10yr yield is up 2.9bps to 4.13% (though at one stage the 10yr did hit 4.22%). Given Powell’s mantra of “…stay the course until the job is done” (similar to Volcker’s 2018 book “keeping at it ”), implied inflation breakevens have fallen back with the 10yr -9.5bps to 2.40% as real yields rose with the 10yr TIP +12.2bps to 1.72%. Equities are down (S&P500 -1.1%), and the USD has surged with the DXY +1.4% to 112.87. The other major story overnight was the BoE which hiked by a dovish 75bps in a split decision (7 vs. 2; one wanted 25bps, another 50bps). What made it dovish was the explicit push back on market pricing with Governor Bailey stating, “we think bank rate will have to go up less than what’s currently priced into financial markets” . Detailed inflation projections revealed that under the market path for rates inflation was set to drastically undershoot the 2% target in two years’ time, and an undershoot would still occur even if the BoE left rates on hold in three years’ time! Before then inflation was set to hit 10.9% y/y in Q4 2022.

Before delving into overnight events, its worth briefly touching on Wednesday’s FOMC meeting with Powell’s press conference transcript now available (see Chair Powell’s Press Conference). The key phrase for your scribe was Powell’s answer to where his risk assessment of doing too little outweighed doing too much. Powell clearly was very asymmetric in his response: “Again, if we over tighten, and we don’t want to, we want to get this exactly right, but if we over tighten, then we have the ability with our tools, which are powerful, to, as we showed at the beginning of the pandemic episode, we can support economic activity strongly if that happens, if that’s necessary. On the other hand, if you make the mistake in the other direction, and you let this drag on, then it’s a year or two down the road and you’re realizing inflation behaving the way it can, you’re realizing you didn’t actually get it, you have to go back in. By then the risk really is that it has become entrenched in people’s thinking and the record is that the employment costs, the cost to the people that we don’t want to hurt, they go up with the passage of time. That’s really how I look at it. So, that isn’t going to change. What has changed though, you’re right, is we’re farther along now. And I think as we’re farther along, we’re now focused on that what’s the place, what’s the level we need to get to rates…” No surprises then to see terminal pricing higher, and yield curves inverting further.

The biggest event overnight was the BoE which hiked by 75bps in what was again, a divided decision (7 vs. 2; Tenreyro for 25; Dhingra for 50bps). Despite hiking by the same amount as the Fed yesterday, the BoE’s hike was dovishly framed (if you can classify 75bps as dovish). Governor Bailey in his press conference said, “we think bank rate will have to go up less than what’s currently priced into financial markets”, albeit recognising that the risks to inflation were to the upside. Key to those statements was that under the market path for rates getting to 5.2%, inflation was projected to fall to “to 1.4% in two years’ time, below the 2% target, and to 0.0% in three years’ time”. And here was the kicker, even assuming “constant interest rates at 3%, CPI inflation is projected to be 2.2% and 0.8% in two years’ and three years’ time”. All that came despite the BoE not factoring likely fiscal austerity measures likely to be announced later this month by new Chancellor Hunt which will further dent GDP growth, with the BoE forecasting calendar year GDP growth to be -1½ in 2023 and -1% in 2024. Even if rates were held constant, GDP would still fall in 2023. Although the BoE pushed back against the market path for rates, Deputy Governor Broadbent clarified “we never said we are aiming for a soft landing”.

Despite that dovish framing, BoE pricing has moved by much with markets pricing around a 50% chance of a 75bp hike at the next meeting, and a peak rate of around 4.75% next year. Gilt yields were actually higher, being dragged by the reaction to the US FOMC with 10yr GILTs +12.2bps to 3.52%, similar to the 10.4bps rise in German Bunds to 2.25%. The biggest move was actually in regards to the currency with GBP plunging -2.6% to 1.1170, partly reflective of USD strength with the DXY up 1.4% overnight. Meanwhile in Europe ECB speakers were out in force with ECB President Lagarde stating she didn’t think a shallow recession “will be able to tame inflation”, suggesting that this wouldn’t prevent further rate hikes (an echo to BoE’s Broadbent comments of “we never said we are aiming for a soft landing”). While Lagarde said her “baseline” scenario was that Europe avoids recession, her colleague Kazaks (and most market participants) think a recession is likely in the coming months. Kazak (echoing the Fed) said at present the greatest danger is from too little monetary policy tightening, rather than too much, with inflation only likely to move back in line with the ECB’s 2% target once rates reach restrictive levels.

In broader FX moves, it was all about USD strength, driven by a backdrop of higher Fed rate expectations and cautious risk appetite. The BBDXY index is up 0.6%, taking it back to within 1.5% of its recent all-time (post-2004) highs. The AUD and NZD are both down around 1% since 5pm yesterday, t the AUD dipping back below 0.63 (0.6294) and the NZD falling back to around 0.5780 (0.5775). Amongst the majors GBP was -2.6% in the wake of the BOE, the EUR was -1.3% and USD/Yen +0.8% to 148.28.

As for data, the US ISM was softer than expected at 54.4 vs. 55.3 consensus and 56.7 previously. The softer than expected data did initially help to stem falls in equities, though equities then sold into the close with the S&P500 closing -1.1%. Details of the release suggested moderating activity with the employment sub-index dipping to 49.1 from 53, while some moderation at still healthy levels was seen in new orders (to 56.5 from 60.6) and production (55.7 from 59.1). Inflation indicators on the other hand were not helpful with prices paid increasing to 70.7 from 68.7, and supplier delivery times blew out with the index lifting to 56.2 from 53.9. Anecdotes revealed it is a very divergent story amongst services firms with one pointing to surprising resilience: “despite the negative inflation news, higher gas prices and concerns of a recession, our restaurant sales have been resilient during what is typically a seasonal slump”. While another is preparing for a recession: “as we prepare for a recession, our stakeholders, clients and vendors are all tightening their belts and reducing new spend.” (see ISM Services for details). Meanwhile Jobless Claims remained low at 217k and still consistent with a tight labour market.

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.