Online retail sales growth slowed in May following a fairly strong April

Insight

Expect a cautious start to the week with the Netherlands going into lockdown on Sunday

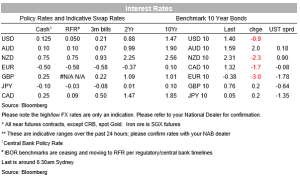

Omicron is set to be the Grinch who stole Europe’s Christmas with weekend news that the Netherlands will be the first country to go into lockdown until 14 January (non-essential stores closed and only 2 visitors to a home). Other European countries have also tightened restrictions. With trading into year-end starting to thin out, it may be volatile run into Christmas. A prelude of that tone was seen on Friday with the S&P500 falling -1% to be down -1.9% on the week. Yields were also heading that way with the US 10yr yield hitting a low of 1.37% at one stage before being pulled higher on hawkish Fed comments to be down just -0.9bps to 1.40%. Fed Governor Waller noted inflation is “alarmingly high”, that “March could be a live meeting ” for a rate hike, and that the Fed could actually undertake quantitative tightening by mid-2022. That hawkishness underlined by 2yr yields which rose 3bps to 0.64%, with 2/10s flattening by -3bps to 76bps.

Waller’s remarks are worth highlighting in detail for how hawkish the Fed has tilted and that shrinking the balance sheet by mid-2022 is a real possibility. “The whole point of accelerating the tapering was to end it much faster in March so the March meeting could be a live meeting. That was the intent,” and thus “… March is a live meeting for the first rate hike.”. Note March is now 54% priced and there is 68bps of hikes priced for 2022. Waller also argued in favour of the Fed starting to undertake quantitative tightening within one or two meetings of rate lift off by allowing maturing securities to run off (“If we start doing some balance sheet runoff by summer, that’ll take some pressure off, you don’t have to raise rates quite as much,” he said. “My view is we should start doing that by summer.”. As for Omicron, Waller also noted the potential impact on inflation by exacerbating labour and goods suppl shortages (see Waller’s speech: A Hopeless and Imperative Endeavor: Lessons from the Pandemic for Economic Forecasters).

The other Fed speaker of note on Friday was the Fed’s Williams who stated he thought the Fed could tighten policy without causing the next recession. Those comments came in reaction to former Treasury Secretary Summers a fortnight ago who noted: “there have been few, if any, instances in which inflation has been successfully stabilized without recession”. Summer’s clarified last week he sees a 30% to 40% chance of recession over the next 2 years. A slowdown is baked in given tighter policy, and Summers only ascribes a 20-25% chance of a soft landing where tighter monetary policy doesn’t sharply constrict economic growth. It’s no surprise then to see curve inversion in OIS FWD Swaps (2Y1Y @ 1.29%; 3Y1Y @ 1.27%) and Eurodollars beyond Dec 2024, while government yield curves themselves have flattened further with 2/10s at 76bps.

Omicron news meanwhile was mixed. News from South Africa continues to suggest vaccines provide a high degree of protection against severe illness. An initial study indicated the T-cell response against Omicron was still 70-80% effective in those who have had two shots of the Pfizer vaccine (see Guardian interview: T-cells in Pfizer Covid jab recipients stay robust against severe illness). Consistent with this, South Africa’s Health Ministry said the hospitalisation rate among those infected with Covid has been much lower this time. Just 1.9% of cases in the second week of the Omicron wave were hospitalised compared to 19% in the same week of the previous Delta wave. Nevertheless, with Omicron cases doubling every 1.5-3 days, the potential for hospital systems to be overwhelmed even with effective vaccines remain. Countries are set to take diverging views on this with Europe tightening restrictions and the US less likely to.

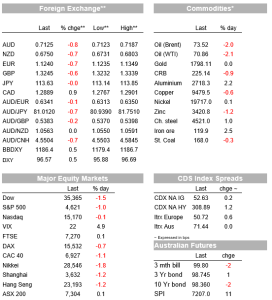

FX moves on Friday showed typical risk haven trends on Omicron concerns with the USD up (DXY & BBDY +0.5%) against every G10 pair apart from the Yen with USD/JPY -0.0% to 113.63. Commodity currencies were particularly hard hit with AUD ‑0.8% and USD/CAD +0.9%, while NZD was -0.7%. As for commodities themselves Brent oil slid -2.0% to $73.52, while gold was largely unchanged in the face of USD strength. The majors also saw heavy action with EUR coming under pressure to be -0.7% to 1.1240, along with GBP -0.6%. Speaking of GBP, expect a soft tone for cable due to the growing Omicron threat and news that Brexit Minister Frost has resigned. PM Johnson’s leadership is now being described as tenuous by many in his party, including leaks by the backbench 1922 Committee, especially after losing a recent by-election, and a leadership challenge in the new year is a possibility. There is though no clear challenger.

ECB speak was on the mildly hawkish side with ECB Governing Council member and Belgium Central Bank head Pierre Wunsch stating the euro area risked falling behind peers in confronting soaring prices: “The big issue for me is the narrative that doesn’t recognize enough that there seems to be an inflation issue in the world and we seem to see it very differently ”. Meanwhile across the channel BoE Chief Economist Pill said he was “uncomfortable” with inflation and that further rate hikes were likely. Data flow was quiet on Friday. UK Retail Sales beat expectations with core retail 1.1% m/m against 0.8% expected. The German IFO in contrast was slightly weaker than expected with the business climate at 94.7 against 95.3 expected and 96.6 previously.

Finally, and perhaps a prelude to 2022, Biden’s signature $1.75tn ‘Build Back Better’ bill looks dead in the water. The bill had included funding for such things as climate change and pre-school childcare, now looks like it doesn’t have the numbers to pass the Senate. West Virginia Democrat senator Joe Manchin told Fox News over the weekend that he couldn’t support it, which would leave the Democrats short of the 50 votes needed in the Senate (assuming the Republican partly remains united in opposition). With the Republicans set to sweep the November mid-terms, fiscal policy could turn heavily contractionary at the same time as monetary policy gears up to fight more persistent inflation pressures. PredictIt has a Republican clean sweep at 0.68c.

The final week into Christmas is very quiet. In Australia we get the RBA Board Minutes for the December meeting on Tuesday which is unlikely to contain much new given Governor Lowe’s remarks last week. In that speech Dr Lowe again pushed back on market pricing for interest rate rises in 2022, but interestingly made little mention of 2024 which to us suggests the RBA is now seeing 2023 as being more probable than the previously characterised “plausible”, and that the upside scenario is probably sitting in late 2022/early 2023. As for QE, three options were discussed with the ‘default’ option being one last taper and finishing in May, while if the data surprised to the upside QE could be finished as early as February. NAB’s view is that QE will end in February based on our forecasts with last week’s strong employment figures, which saw record high levels of employment and the unemployment rate falling sharply to 4.6%, affirming our view.

As for offshore it is even quieter. The US has the PCE deflators on Thursday with he consensus for core at 4.5% y/y. Durable goods are also on Thursday. Neither are expected to be particularly market moving given the hawkish tilt by the US Fed last week. Instead, Omicron is likely to be the bigger news piece and whether individual states in the US tighten restrictions to slow the spread of the variant as many European countries have. Europe’s main focus will be whether other countries follow the Netherlands into lockdown, ditto the UK. As for China it is also a quiet week with only the Loan Prime Rate decision today with the consensus for no change. Across the ditch in NZ there is a little bit more data, but all second tier, with the trade balance today and later in the week credit card spending and consumer confidence.

There is nothing domestically or offshore of note. Across the ditch NZ has the trade balance which is unlikely to be market moving with no consensus available. China has the loan prime rate decision with the consensus for no change, though there is a small minority tipping a cut of 5bps for the 1yr rate to 3.80% from 3.85%.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.