Housing market sentiment rallied as national housing price growth accelerated in the March quarter.

Insight

The Bank of Japan’s changing approach to yield control and China’s policy to protect the economy had the most impact on markets today.

https://soundcloud.com/user-291029717/a-weakening-renminbi-rising-bond-yields-and-tweets-in-block-caps

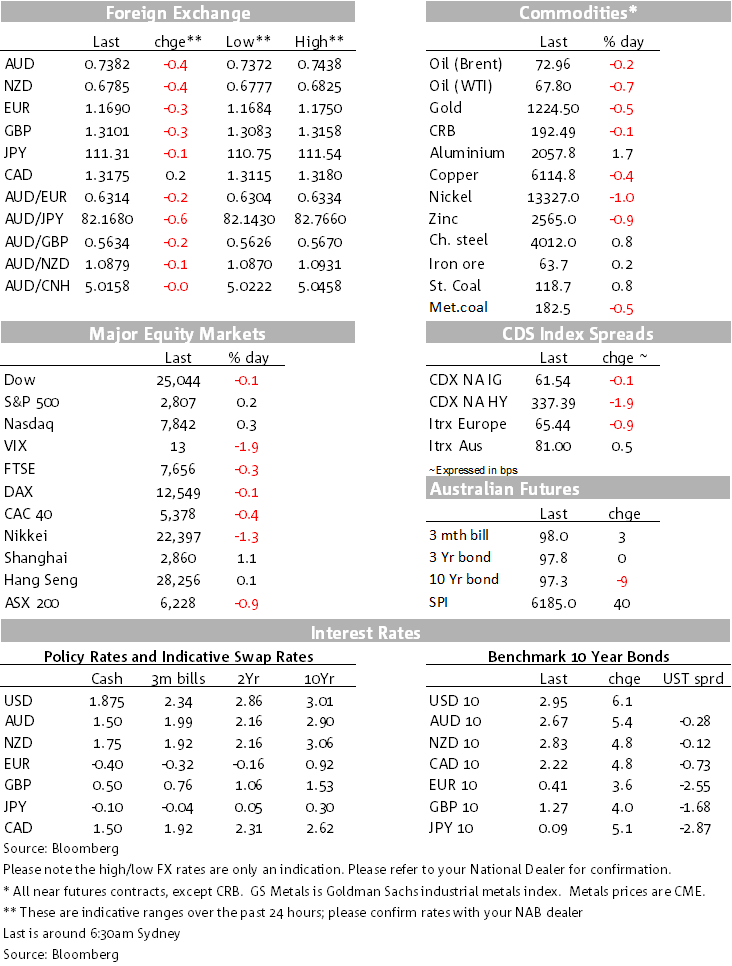

Bond markets have grabbed the primary attention of markets, centred on Japan for once, while in currency markets, the USD has made up some net ground, if assisted by weakness in the AUD and NZD stemming from weakness in the Chinese yuan.

Bond markets in recent times have been taking their lead from developments in the US, but it’s been developments in Japan that have gripped the market’s attention since late last week, developing further in the past 24 hours.

The BoJ meets next week and there is speculation that the central bank will tweak its policy in some way (support for medium to longer term yields?) to make it more sustainable, whatever that might mean. This also comes with the expectation that the BoJ will likely lower its inflation forecasts with the implication that its QE policy with yield curve control (-0.1% short term rate and 0.0% JGB 10 year bond yield target) might need to be tweaked/adjusted in some way, possibly to support bank profitability and avoid other side effects of exceptionally low yields for an even more protracted period.

The Asahi newspaper reported that BoJ policymakers wouldn’t make a decision at this meeting, but would announce a review of its framework. Even so, JGB yields retained support, the market anticipating the policy risk of more steepness in the yield curve. In response to market moves, the BoJ announced yesterday it would be it would be offering an unlimited fixed rate bond auction for the first time since February 2018 with a yield of 0.11%, drawing a line in the sand that caps the ceiling on 10 year yields at 0.10%.

The 10 year JGB yield spiked initially higher, settled back but rose again, peaking intra-day at over 0.09%, closing up a net 5.1bps to 0.086%. European and US bond yields have moved higher in sympathy on the back of a very light news flow overnight, the German 10 year bund up 3.7 bps to 0.406% and the 10 year Treasury up a solid 6.47bps to 2.9578. 30 year Treasuries rose 7.09bps, Japanese 30 year bonds up a net 9.4bps yesterday to 0.784%, the 40y bond up 10.8bps to 0.919%.

Of course, there is the added difficulty that if any BoJ “policy tweaks” do have the effect of supporting medium to longer term yields further then that would also have the effect of supporting the yen, blunting chances of achieving higher inflation. That is the way the market played it yesterday, the yen outperforming and closing square against the USD after some initial strength in the APAC session. The Nikkei closed down 1.33%, the Topix down 0.4%. European equities closed down marginally (the Eurostoxx 600 index by 0.19%), the Dow has closed close to square (-0.06%) and the S&P 500 +0.18%. Amazon shares closed down 0.6% after a taking an initially larger hit from a Trump tweet saying that many feel Amazon should face anti-trust claims.

The Japanese yen certainly outperformed on the crosses, the AUD and the NZD losing some steam at the overnight session from further weakness in the Chinese yuan. The AUD trades this morning at 0.7382, down 0.4% over the past 24 hours and the NZD at 0.6785, also down 0.4%. (Recall that speculative NZD positioning has been very short, hinting at potential AUD/NZD downside risk.)

The Aussie remains centred on Chinese currency developments. The PBoC injected $74b of liquidity via its Medium-Term Lending Facility (MLF), its largest ever operation via this facility. Amidst further policy easing from China, the CNY weakened 0.4%, with USD/CNY approaching its highs for this year of 6.8. The CNY has fallen over 6% against the USD in little more than a month. There were also some further incremental policy developments.

Elsewhere in the currency space, Sterling had a brief dip after BoE Deputy Governor Broadbent said he didn’t know whether he’d vote for an August rate rise. The fall wasn’t sustained, the GBP sits just above 1.31, down 0.2% over the past 24 hours. Conservative cabinet minister Jeremy Hunt was the latest to sound a warning about UK-EU negotiations, saying that there was “a very real risk of a Brexit no deal by accident”.

It was very light for data with only the Chicago Fed National Activity Indicator (a volatile indicator and nowhere near the top of the watch list), coming with US Existing Home Sales for July. There were soft again in July (-0.6% after -0.7%), though the US National Association of Realtors Chief Economist attributed this to a shortage of stock and not a weakening in demand. Median prices were up 5.2% y/y.

Not too much further to report with somewhat lower oil, gold and base metal prices (USD strength), while on the Australian bulk commodity export front, Met Coal prices eased, steaming coal prices were higher again, as was iron ore on the day.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Housing market sentiment rallied as national housing price growth accelerated in the March quarter.

Insight

Growth slowing, but less abruptly than Q1 GDP suggests

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.