Coming in for landing in a heavy cross wind

Insight

Risk assets remained out of favour as concerns over inflation and recession risk continued to dominate.

https://soundcloud.com/user-291029717/a-world-of-worry?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

Risk assets remained out of favour as concerns over inflation and recession risk continued to dominate. Rumours of lockdown in Beijing had added to the risk-off tone, though were denied by Beijing, with the city instead opting for increased testing and reduced movement. Gazprom implemented Russian sanctions on the Yamal pipeline, reducing gas supplies to Germany.

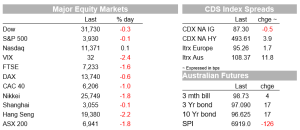

Equities were mostly lower in another volatile session. The S&P500 was down as much as 1.9% at one point, before staging a late rally to finish 0.1% lower as gains in health care and consumer discretionary were offset by lower utilities and IT stocks. The Nasdaq managing to close in the green, up 0.1%. The Euro Stoxx 50 lost 0.9%, while the Nikkei was down 1.8%.

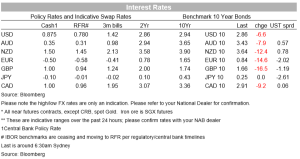

The USD was stronger against all G10 currencies except the yen . The dollar rose 0.9% to 104.8 on the DXY, its highest since 2002. The move was driven by a softer euro, losing 1.3%. In contrast, the yen rose 1.3%, the dollar buying 128.34 yen, after dipping as low as 127.52 intraday. The AUD fell 1.1% to trade at 0.6856, off its intraday low of 0.6829. The RMB continued to weaken, spurred on by concerns about tighter COVID restrictions and the hit to activity. The CNY was off 1.0%. In a further sign that China is continuing with its zero-covid polices, the government announced that it would ‘strictly limit’ unnecessary outbound travel by its citizens.

Growing fears for the growth outlook have also seen yields lower. The US 10yr was 7bp lower at 2.86, after dipping as low as 2.81%, their lowest since 28 April. European yields declined sharply. The German 10yr down 15bp to 0.84%, and the UK 10yr 17bp lower to 1.66%.

Late comments from San Francisco Fed president Mary Daly in the couple of hours seemed to help a turnaround in equities . Daly sees no reason to alter the course for 50bps at the next two meetings and reiterated that she wants to see rates at neutral of 2.5% by the end of the year. Daly said that she wasn’t especially surprised by the April CPI data and that debate between 50 and 75bps was not a primary consideration. That seemed to provide some relief for equities, which pared losses after the comment. As I type, Fed Chair Powell reiterated that message, repeating that 50bp moves at the next two meetings were appropriate. Separately, the Senate confirmed Powell for a second term. Lisa Cook, and Philip Jefferson, were also confirmed by the Senate this week to fill two vacancies on the Board of Governors.

In terms of data flow, UK Q1 GDP came in a little softer than expected. The UK economy contracted 0.1% in March and the February number was revised down to flat form a 0.1% expansion. That combined to put Q1 growth at 0.8% q/q, below the consensus for a 1.0% gain. That’s ahead of a larger squeeze on real incomes to come in Q2.

US PPI came in around consensus in April, with the headline PPI decelerating to 0.5% m/m as expected from an upwardly revised 1.6% in March, but remaining elevated. The y/y rate slowed to 11% from 11.5%.

Russia state-owned gas-supplier Gazprom indicated it will cut shipments through the Yamal pipeline , which runs from Russia to Germany via Poland. That follows sanctions on European gas companies by the Kremlin the previous day. Very little gas has been passing through the pipeline recently. German economy Minister Robert Habeck said “the situation is escalating” and that supply had dropped by 10m cubic metres a day, or 3%. Natural gas prices were 12% higher. Meanwhile, Finland said it would apply for NATO membership “within days” and Sweden’s government is expected to make a decision soon.

Adding to the volatile picture, the crypto landscape has been roiled as tether, the largest stablecoin, failed to maintain its link to the dollar. Tether fell as low as $0.9511, before revering back above 99 cents. That follows the implosion of the TerraUSD stablecoin on Wednesday. The stabilisation in tether and the restart of the Terra blockchain has seen some panic subside. Bitcoin rose as much as 6% to around $30,000 after falling to around $25,000.

Read our NAB Markets Research disclaimer For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.