SVB fails, roiling markets, taking the gloss off a mixed payrolls report

Focus now on whether actions to date can avoid a regional US bank run

Payrolls mixed; strong payrolls, but softer than expected earnings

This week: SVB fallout; AU Jobs, NZ GDP, US CPI, ECB, CH Activity

Coming up: Nothing of note, all about the fallout from SVB

“If you invest your tuppence; Wisely in the bank; Safe and sound; Soon that tuppence; Safely invested in the bank; Will compound”, Fidelity Fiduciary Bank, Mary Poppins, Richard & Robert Sherman, 1964

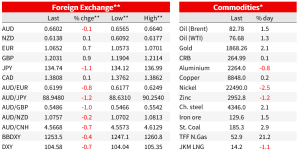

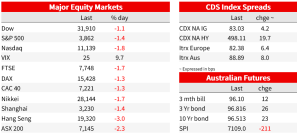

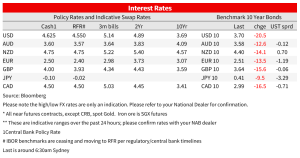

The collapse of SVB, the 16th largest bank in the US with $209bn in assets (as at 31 Dec 2022), shook markets on Thursday and Friday. That event, alongside a mixed US payrolls report (Payrolls 311k vs. 225k expected; UR 3.6% vs. 3.4% expected; AHE 0.24% m/m vs. 0.3% expected), saw yields and rate hike expectations fall sharply. Over Thursday and Friday the 2yr Treasury yield fell -47bps to 4.59%, and the 10yr yield by -27bps to 3.70%. Positioning likely exacerbated moves; CFTC data up to 21 Feb showed spec investors held large net shorts. Terminal fed funds pricing now stands at 5.29% from 5.69% on Wednesday, and markets now only ascribe a 32% chance of a 50bp hike in March, well down from 71% on Wednesday. Equities fell sharply with the S&P500 -1.4% on Friday, following -1.8% on Thursday. Sharp falls have been seen in bank stocks with the Invesco KBW Bank ETF -11.1% over Thursday and Friday. Interestingly gold rallied on Friday (+2.1%), while the USD (DXY) fell -0.9% as yields tumbled.

Safe havens outperformed with USD/JPY -0.9% to 135.03; and USD/CHF -1.7% to 0.9197. Meanwhile risk proxies such as the AUD and NZD underperformed. As markets open, all focus will be on whether authorities have done enough to stabilise confidence in US banks to avoid a spread of depositor flight. The situation is in flux and as your scribe types the Washington Post reports regulators are contemplating protecting all depositors at SVB (see WAPO: U.S. officials weigh protecting all deposits at Silicon Valley Bank ). There has been some improvement in sentiment of the back of this headline with the AUD +0.4% to 0.6601, and Bitcoin has spiked up 2.5%. Against that voluminous twitter posts show people queuing outside of certain regional US banks on the weekend, including First Republic Bank. The FDIC had said on Friday that for SVB insured depositors (those with amounts <$250k), they would have their funds available in full from Monday, with the standing of uninsured depositors less certain (a sales process kicked off on Saturday with bids to be finalised by Sunday afternoon according to reports)

Treasury Secretary Yellen on Sunday said there would be no bailout for SVB, but hinted at something to shore up depositor confidence. It was also reported the FDIC and the Fed are discussing creating a fund that would allow regulators to backstop more deposits at banks in the future. The FDIC/Fed of course will do whatever it takes it avoid a bank run spreading, key is whether actions to date are enough, or whether more is needed. The drama around SVB also highlight several issues. It is clear inflation remains too high, so the need to continue with rate hikes remains. However, it is uncertain what financial structures could be vulnerable following a decade of extraordinary low rates – you only when the tide goes out. If mark to market losses on bond portfolios are a worry for certain US banks, what about European and Japanese banks? Finally, deposit outflows could continue, the sharply inverted yield curve means competition for deposits, a Treasury Bill now earns close to 5%, compared to paltry returns on deposit accounts.

What happened to SVB? In short, poor interest rate risk management on the asset side. SVB was the 16th largest bank in the US with US$209bn in assets as at 31 December 2022. The bank had a large focus banking silicon valley tech firms and venture capital, with strong growth in deposits seen during the pandemic. With strong deposit growth, but less growth in loan demand, it invested those deposits in fixed income securities, mainly Treasuries and agency backed MBS. As interest rates rose, the market value of those assets fell. The mark to market losses on assets though were not recognised and regulatory capital not increased given they were held as either ‘Held to Maturity’ ($91bn), or had special regulatory treatment within ‘Available for Sale’ ($22bn). As rates rose, the bank suffered from greater than expected deposit outflow (likely from tech clients needing liquidity as private capital became more expensive and possibly as depositors saw rates elsewhere). To meet outflows, it sold securities, but given the mark to market it made losses, and it needed more capital. A 2.25bn capital raising failed, with depositor flight ensuring with reports depositors tried to withdraw $42bn on Thursday.

As for Payrolls, it was a mixed report, which absent SVB would have put focus on CPI on Tuesday as the decider on whether the Fed would go 50bps in March. Headline payrolls were stronger than expected at 311k vs. 225k and 504k previously. However, the unemployment rate rose by two tenths to 3.6% vs. 3.4% expected, while average hourly earnings came in at 0.24% m/m vs. 0.3% expected. Very mixed. There was enough strength in the report to justify another 50bp hike though given average hourly earnings for production and non-supervisory workers was stronger at 0.46% m/m after being 0.3% in January. Of course talk of a 50bp hike in March has lessened sharply and markets now only ascribe a 32% chance, down from 71% on Wednesday. Peak Fed Funds pricing has also fallen to 5.29% from 5.69% on Wednesday.

There was also other data and events on Friday, but these took a back seat to the dramas around SVB and to payrolls. In Japan BoJ Governor Kuroda went out with a whimper than a bang, leaving policy settings unchanged and entrusting any potential change in policy direction to the new incoming Governor Ueda. Given the outside chance of a surprise move, the yen immediately weakened, with USD/JPY peaking just under 137, before risk off hit to now trade at 134.71. In the UK Monthly GDP rose 0.3% m/m against 0.1% expected, a positive surprise that followed weak growth over Q4. And in Canada employment growth was stronger than expected (21.8k vs. 10k expected), unemployment held steady (5.0% vs. 5.1% expected), and hourly wages were stronger (5.4% y/y vs. 5.1% expected). Further strong data would challenge the BoC’s case for a pause in the tightening cycle. Finally, China credit growth was much stronger than expected in February (aggregate financing 3160.0b vs. 2300.0 expected)

This week:

Australia: Two of the four data pieces the RBA will be looking at ahead of the April Board meeting come out this week, with Employment on Thursday and the NAB Business Survey on Tuesday. We look for employment to rebound sharply after January was weighed down by shifting seasonals, with around 70k extra people waiting to begin a job than usual. We pencil in +60k for February, above the consensus for 50k, and for unemployment to fall a tenth to 3.6%. The risks are tilted to an even stronger report. Given Governor Lowe said the RBA expects more tightening is necessary, if employment rebounds as we expect, a hike is likely in April. Markets currently price just 11bps for April and 21bps of further tightening by May. Other data out includes the NAB Business Survey and Consumer Confidence, both on Tuesday. Note there are public holidays today in VIC, SA, TAS, ACT have a public holiday on Monday.

Offshore: Five key events to watch this week: (1) The fallout from SVB and how quickly authorities can restore confidence in regional banks. Assuming confidence is stabilised then focus shifts to; (2) US CPI on Tuesday as a key input into the 22 March FOMC meeting. Markets have sharply pared pricing to just a 33% chance of a 50bp hike and now price a peak terminal rate of 5.29% in the wake of SVB. Other key data includes Retail Sales and PPI; (3) ECB on Thursday where a 50bp hike is universally expected. Expect upward revisions to inflation forecasts, but pre-commitment to another 50bp hike in May looks a step too far; (4) China activity data on Wednesday for January and February should confirm the rebound and China’s statistics head on Sunday flagged a strong print and also hinted that the official ‘about 5%’ 2023 growth target was conservative; and (5) NZ Q4 GDP on Thursday where my BNZ colleagues see a decline of 0.2% q/q (+3.3% y/y). This contrasts with the 0.7% gain the RBNZ anticipated, as per its February MPS.

Coming up today (very quiet):

NZ: Services Index and Food Prices: No consensus available; the prior read for the services index was 54.5.

AU:Public Holidays in Certain States: public holidays today in VIC, SA, TAS, ACT

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.