Coming in for landing in a heavy cross wind

Insight

Equities bounced back in the US and Europe as markets re-evaluated the comments about the timing of tapering in this week’s FOMC minutes.

https://soundcloud.com/user-291029717/it-was-another-turnaround-thursday?in=user-291029717/sets/the-morning-call

Equity markets in the London, Europe and the US were back in the black today, helped by the combination of some further easing in oil prices, general market stability (including bitcoin) and especially in the US session, a marked reduction in US Treasury yields, mainly from a pull-back in market-implied inflation rates. Mainboard European-UK markets rose by between 1% (FTSE) and a 1.7% gain in the DAX. Fed Chair Powell announced overnight (see here for the statement and a video message from Powell) its response to technological advances driving rapid change in the global payments landscape, refining its role as a core payment services provider and as the issuing authority for U.S. currency, including whether and how a central bank digital currency could improve the US payments system. They plan to publish a discussion paper in the summer.

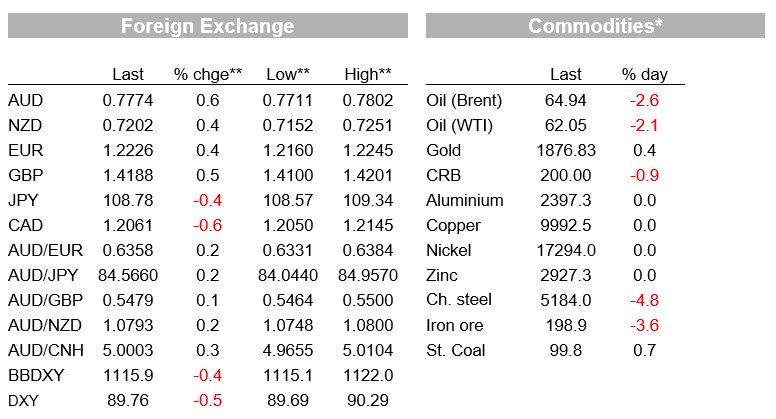

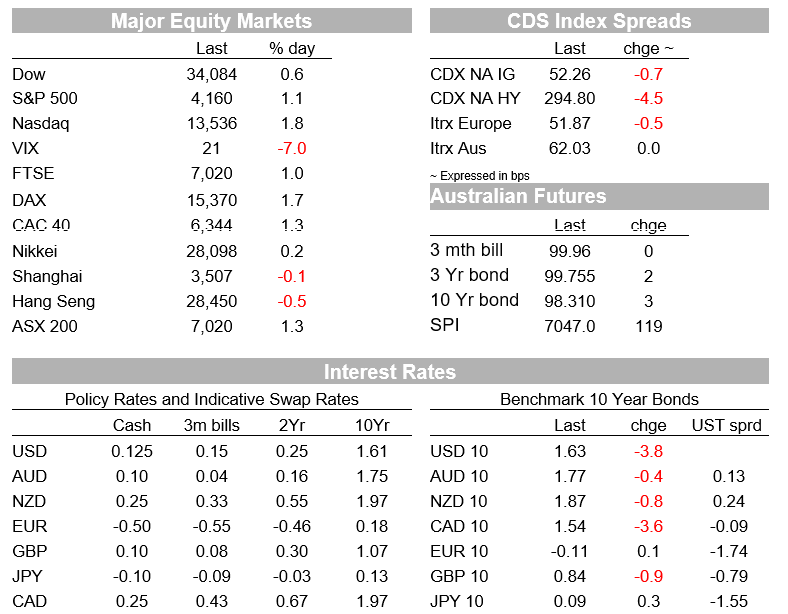

US equity markets have closed higher, the Dow up 0.56%, S&P 500 +1.06% and the Nasdaq up 1.77%. ‘FAANG’ stocks closed up 2.38%, Netflix +2.86%, Twitter up 3.38%. Tesla rose 4.14%. Ahead of the local open today, SPI futures are up 0.50%.On the commodity price front, base metals and iron ore were mixed, oil lower again.

It was a more balanced and uneventful session, US Treasury yields retraced lower after the FOMC Minutes inspired spike yesterday and 10s almost back to post CPI levels.

The pull-back in Treasury yields was given more impetus in the aftermath of an auction of 10 year Treasury inflation-protected stock seeing weaker demand, playing to the narrative of some re-think that inflation could still be more of a temporary nature. The 10y break-even inflation rate is trading this morning at 2.4565%, down 3.93bps for the day, shorter-dated BEIs down by even more as market-implied inflationary expectations get wound back. It closed at 2.56% last week after the April CPI. Make an adjustment to the CPI-based 10y BEI to convert to a PCE deflator-implied BEI and it’s not far above 2% and not above the Fed’s modestly above 2% inflation target.

As bond yields retraced back down, so did the USD, the DXY index finding more comfortable ground below 90, currently at 89.8 as we go to press this APAC morning. Top of the currency leader board overnight has been sterling, cable up 0.51% since early in the London session to almost 1.42, currently at 1.4189. Public Health England is continuing to report reductions in COVID fatalities and hospital admissions, even though pockets of the India variant remain under close scrutiny and infections perhaps flattening out after very big falls in recent months.

The CBI manufacturing trends survey May jumped to +17 from -8 ahead of the Markit preliminary PMIs for May and April Retail Sales tonight, both expected to reflect the continuing re-opening of the economy through April and May. This was the equal strongest reading from this survey since May 1988. Rather unsurprisingly, selling prices were punchy too at 38, up from 27, an almost equal record too.

Speaking on the UK housing market, BoE Deputy Governor and head of financial stability, Sir Jon Cunliffe spoke about how the housing market boom may persist after the tax incentives end. (A 500K stamp duty free threshold has been extended to June, then tapered to £250K to the end of September.) He mentioned what has now become a refrain of buyers looking for more space and a sea change in many housing markets that “the composition of ….. demand, which has driven the U.K. market in recent months reflects some more persistent drivers and that the market will not fall back to its pre-pandemic decade performance when the tax incentives have gone”.

Elsewhere in currency space, the risk/commodity currencies made gains of 0.30% (NZD), 0.34% for the AUD, and a 0.46% rise in the CAD despite further softness in world oil prices after further reports that the Iranian government seems to be closer to the prospect of a nuclear deal that would unlock opportunities to lift its oil export revenues. Also offering some support for the CAD was the release of the BoC Financial Stability Review with its warnings about Canadian house prices. Governor Macklem flagged a worsening quality of new mortgages during the pandemic, also calling out major city housing markets as ‘exuberant ‘.

On the US data front, US weekly jobless claims came in at 444K last week, a smidge better than the 450k consensus. PUA (gig economy) claims were 95k, down from 103k. These are continuing to move in the right direction but the Fed will want to see more data prints to fulfil its claim of ‘substantial further progress to its goals …relative to conditions prevailing in Dec 2020’. In that measurement the US has created 1.67mn new jobs only and inflation, while now above 2%, dies not fulfil the ‘sustained basis’ requirement.

The Philly Fed Business Outlook for May disappointed at 31.5 for the general business activity headline vs the 50.2 record in April and 41 forecast. The detail shows new orders slipped to 32.5 from 36, employees fell to 19.3 from 30.8, shipments eased to 21 from 25.3, with unfilled orders ramping to 40.4 from 27.2, underlining the shortage of available workers to get the stuff out. Meanwhile prices paid continued accelerating to 76.8 from 69.1, a new high (though they were at 72.6 in Mar). It is a neat account of supply/demand issues and bottlenecks continuing. However, the slide in new orders raises another question.

Dallas Fed Kaplan was speaking again, repeating his call for taper talks to begin sooner rather than later (we know who at least one of those ‘participants’ mentioned in the Minutes is), also noting the wisdom of weighing up cost-benefits of the Fed’s emergency policies. No such views in the ECB it seems, ECB chief economist Lane saying overnight that the recent increases in input prices have “nearly zero connection” to underlying economic trends and the ECB has “a lot of work to do” to reach its inflation target.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.