Total spending grew 0.9% in June.

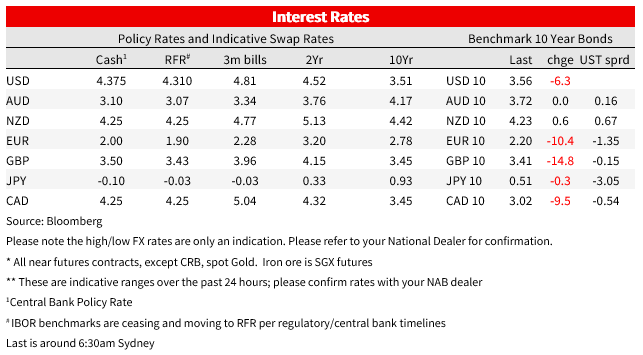

Ahead of CPI tonight US Treasuries (and bonds globally) have rallied, 10-year US notes off 5bps (3bps of that seen in the Tokyo session) and 2s down just under 2bps.

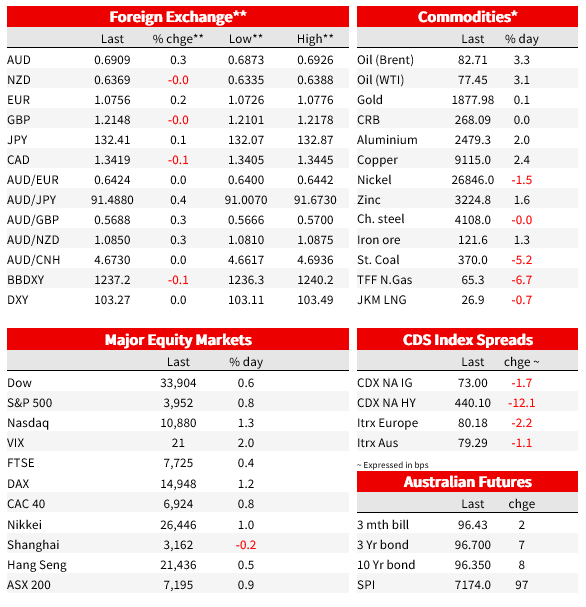

There has been very little ‘new news’ flow ahead of tonight’s all-important US CPI release, but which hasn’t prevented a reasonable amount of volatility in markets, more so bonds and stocks than currencies, where the AUD/USD maintained its G10 leadership role established after yesterday’s CPI and retail sales data. Bonds, which on Tuesday were retracing some of the year-to-date rally and deemed to be a product of position reduction ahead of CPI, have instead rallied (more so in Europe than the US), while US equities approach the last hour of NYSE trade showing gains of +/- 1% for the S&P500 and NASDAQ in a broad-based but led by a 3%+ rally in the Real Estate sector. Gains follow a good day for European stocks where the Eurostoxx 50 finished with a 1% gain. There has been no economic data of note in either Europe or North America overnight.

Ahead of CPI tonight US Treasuries (and bonds globally) have rallied, 10-year US notes off 5bps (3bps of that seen in the Tokyo session) and 2s down just under 2bps. The US 0-yar Note sales went off well if not quite as impressively as the prior day’s 2-year Note sale. It cleared 0.5% through the when issued yields (3.575% vs 3.58%) with an above (1-year) average bid-cover ratio of 2,53 and also above average indirect bidder take-down. European bond yields fell by much more than the US, by 10-15bps for 10-yar benchmarks (including gilts -15bps and Italian BTPs by 19bps).

Incoming central bank speak has generally been supportive of bond price gains. Susan M. Collins, President of the Federal Reserve Bank of Boston, is the latest FOMC official to lend support to a quarter-point move at the Feb. 1 meeting. “I think 25 or 50 would be reasonable; I’d lean at this stage to 25, but it’s very data-dependent,” Ms. Collins said in an interview with The New York Times on Wednesday. “Adjusting slowly gives more time to assess the incoming data before we make each decision, as we get close to where we’re going to hold. Smaller changes give us more flexibility.” Ms. Collins said she favoured raising interest rates to just above 5 percent this year, potentially in three quarter-point moves in February, March, and May. “If we’ve gone to slower, more judicious rate increases, it could take us three rate increases to get there – and then holding through the end of 2023

We also had a Market News source report titled ‘ECB Doves Eye Smaller Hikes as Inflation falls’ which is being credited for a fall-back in ECB pricing by July this year from a cumulative 148bps to 141bps beforehand. ECB hawk Robert Holzmann, the Austrian central bank chief, meanwhile said that while interest rates will have to rise significantly further to reach levels that are sufficiently restrictive to ensure a timely return to the 2% medium term inflation target, there are ‘no signs of de-anchored market (inflation) expectations’.

For JGBs meanwhile, where the 10-year yield has been stick at 0.5% (or a bit higher) all week, of note yesterday in relation to ongoing fevered speculation of an early end, or further adjustment, to the BoJ’s YCC policy and with the BoJ having to step in with more unscheduled bond buying operations, Fast Retailing, Asia’s largest clothing retailer and owner of the Uniqlo fashion brand, said it will increase employee wages in Japan by as much as 40 per cent as inflation in the country rises at its fastest pace in decades. The sharp jump in pay follows Prime Minister Fumio Kishida’s calls on Japanese businesses to raise real wages, that have remained stagnant for decades.

Yesterday’s local data, comprising a slight upside surprise to November monthly CPI (up to 7.3% y/y. from 6.9% and market consensus 7.2%) and bigger upside surprise in November retail sales (1.4% m/m against 0.6% expected and with the previously reported 0.2% October fall revised to +0.4%) saw money markets lift their pricing for February (and March) RBA tightening prospects, but the moves completely evaporate in afternoon trade, no doubt thanks in part to a rally in US interest rate markets, albeit concentrated at the longer end.

The FX market took (durable) notice of the data at least, AUD the best performing G10 currency during the local session, with all of the gains coming post the data, AUD/USD recapturing the 0.69 handle amid significant cross-rate outperformance. AUD is currently still holding above 0.6900, but only just and back a little from its APAC session highs (+0.2% on the day). It’s still the best performing G10 currency of the last 24 hours (and YTD), followed by EUR/USD up 0.15%, while GBP is a touch softer, as is NZD. CHF, down 0.9%, is the worst performing major currency, not on any significant news as best we can tell.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.