NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Europe remains stuck in the middle between the Russia/Ukraine crisis and a weakening global economy

https://soundcloud.com/user-291029717/australia-faring-better-than-most-but-big-hike-still-expected?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

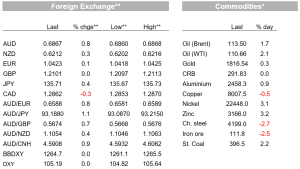

Trading conditions were quiet overnight with the US out on their Independence Day Holiday. Sentiment remains fragile with the EuroStoxx50 +0.1% and S&P500 futures -0.4%. Major moves were concentrated in Europe where yields rose (German 2yr +9.8bps to 0.62% and 10yr +10bps to 1.33%). Hawkish ECB comments added with the Bundesbank’s Nagel stating the ECB’s very accommodative stance would “swiftly be abandoned” and that a restrictive policy stance may be needed to achieve the inflation target. Concerns around European gas are also elevated, particularly for Germany which saw its first trade deficit since 1991, and investor sentiment as measured by Sentix disappointed (-26.4 vs. -20.0 expected). The USD is little changed, though did fall earlier on headlines of Biden potentially easing tariffs on China. Commodity currencies were boosted a little (AUD +0.8%), though NZD was little moved and the Yen underperformed (USD/Yen +0.4% to 135.73).

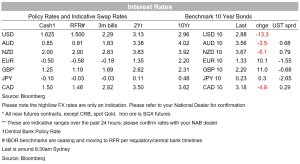

The hawkish ECB commentary was probably the biggest news overnight in what was a quiet night for markets . Governing Council member Vasle of Slovenia said that there will be more hikes after the September quarter. Bundesbank President Nagel said that the ECB’s very accommodative monetary policy stance would “swiftly be abandoned” and a restrictive policy stance may be needed to achieve the inflation objective. Nagel also spoke about the ECB’s new anti-fragmentation tool and suggested that the crisis instrument should only be used in “exceptional circumstances and under narrowly defined conditions” and any activation of the took should be “strictly temporary”. Speaking after Nagel at the same conference, ECB Vice-President de Guindos was also caution on the tool, noting “ we will react to prevent fragmentation, with suitable safeguards to prevent moral hazard”. Overnight Germany’s 10-year yield rose 10bps and the 2-year rate rose 11bps. Italian 10yr yields rose 15.8bps to 3.24%, though this was mostly due to domestic political tensions with PM Draghi and Conte meeting.

Europe remains stuck in the middle between the Russia/Ukraine crisis and a weakening global economy. Illustrative of that was the German trade balance which slipped into deficit for the first time since 1991 (-1bn vs. +1.6 expected). The rise in energy costs is the main driver with import values up 28% over the past year, compared to a 11.7% rise for exports. Given elevated energy prices, trade deficits for Germany are likely to persist at least for the near term. German industry is very concerned and vocal, while investors are becoming more pessimistic with Sentix investor confidence falling by more than expected (-26.4 vs. -20.0 expected). Sentix noted rather alarmingly: “ In every respect, the dynamics are reminiscent of the crisis year 2008, and what was then the collapse of the financial system is now the danger of the collapse of the European energy supply. While the financial system essentially consists of money, which can be printed by its own central bank in any amount as needed, a lack of gas is not so easy to replace”.

On a more positive narrative for inflation, the WSJ covers some anecdotes of excess inventories and an easing of demand in semiconductors. US retailers are starting to clear excess inventory by selling to ‘off-price retailers’ with one off-price retailer noting they are selling name-brand washers and dryers at 40% off the regular prices. The same off-price retailer notes there is more excess merchandise now than at any time in the past two decades (see WSJ: Glut of Goods at Target, Walmart Is a Boon for Liquidators). Meanwhile US chipmakers are starting to see some easing in demand with Memory maker Micron Technologies last week noting “the industry demand environment has weakened”, while others are reporting mixed news on easing consumer demand but a pick-up in business demand (see WSJ: Chip Boom Loses Steam on Slowing PC Sales, Crypto Rout).

Meanwhile in the US, President Biden is again reported to be contemplating rolling back some tariffs on Chinese imports in an effort to slow inflation. It is reported this could entail a pause on tariffs on consumer goods and school supplies, but at the same time raising tariffs on strategic items such as industrial machinery and transportation equipment. As a concession to China hawks, a fresh investigation into China’s subsidies for high-tech firms could also be initiated. It is worth noting the Administration is split on easing tariffs. Treasury Secretary Yellen has seen them as a way to help curb inflation, but China hawks see tariffs as a valuable leverage to get concessions from China (see WSJ: Biden Might Soon Ease Chinese Tariffs, in a Decision Fraught With Policy Tensions). Modelling suggests easing tariffs would take between 0.3-1.0 percentage point off inflation.

In FX it has been a fairly quiet session. USD/CNH and USD/CNY spiked lower on the China tariff news above, but the move has now been fully reversed. The news though did help support the AUD which is up 0.7% from Friday’s close to 0.6860. The NZD is little changed at just over the 0.62 mark, with a lift to 0.6250 not sustained, seeing NZD/AUD down 0.7% to 0.9045. Commodity currencies head the leaderboard, but the NZD didn’t get the memo, with NOK the best performing, up 1.4% and CAD up 0.3%. Crude oil prices have increased almost 2% amid reports Kazakhstan’s oil output is down 22% from May with planned maintenance. Meanwhile in Canada the latest inflation expectation survey sees a record 78% of firms seeing +3% inflation over two years. Elsewhere EUR and GBP are little changed from last week’s close, while the yen is the weakest of the majors against the backdrop of higher global rates. USD/JPY is up 0.4% to 135.70. Given Europe’s dire predicament, it is hard to see an enduring Euro rally, which may keep USD strength going for longer.

Finally in Australia, the Melbourne Institute monthly inflation gauge points to a very strong Q2 CPI print with the trimmed mean measure in quarter-average terms increasing 1.4% q/q, up from 1.1% q/q in Q1. On a monthly basis the trimmed mean measure did ease to 0.3% m/m, but this followed a very strong 0.7% m/m in May and there is no sign yet of core inflation pressures easing out of this monthly indicator. Very little breakdown is available in today’s data. The Melbourne Institute inflation gauge is not ordinarily closely watched and reads through imperfectly to the ABS measure.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.