Long-term signal vs. Short-term noise

Insight

Fed speakers were clear that a pause is not imminent and there is more to do, even as they may move at a slower pace, while stronger US retail sales numbers showed resilience in spending, providing some small counter to the burst of optimism after softer-than-expected US inflation data last week.

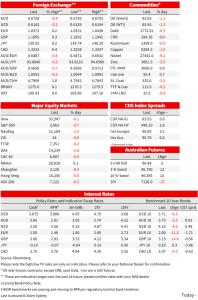

AU: Wage price index (q/q%), Q3: 1 vs. 0.9 exp.

UK: CPI (y/y%), Oct: 11.1 vs. 10.7 exp.

UK: Core CPI (y/y%), Oct: 6.5 vs. 6.4 exp.

CA: CPI (y/y%), Oct: 6.9 vs. 6.9 exp.

CA: Core CPI (avg. of 3 series, y/y%), Oct: 5.4 vs. 5.3 exp.

US: Retail sales (m/m%), Oct: 1.3 vs. 1 exp.

US: Retail sales ex auto & gas (m/m%), Oct: 0.9 vs. 0.2 exp.

US: Retail sales control group (m/m%), Oct: 0.7 vs. 0.3 exp.

US: Industrial production (m/m%), Oct: -0.1 vs. 0.1 exp.

US: NAHB housing market index, Nov: 33 vs. 36 exp.

A more cautious tone in markets overnight with equities lower and the US curve inverting further. Fed speakers were clear that a pause is not imminent and there is more to do, even as they may move at a slower pace, while stronger US retail sales numbers showed resilience in spending, providing some small counter to the burst of optimism after softer-than-expected US inflation data last week. Currency moves have been relatively modest.

Equities were generally lower. The S&P500 was tracking around 0.7% lower, while the Nasdaq is around 1.5% lower. Comments from US President Joe Biden that Ukrainian air defenses, rather than Russian missiles, had likely caused Tuesday’s explosion in Poland earlier allayed some fears of escalation. The Euro Stoxx 50 lost 0.8%.

US retail sales rose 1.3% in October, beating expectations for a 1.0% gain and supported by a jump in auto and gas sales. But more than just higher fuel prices, the detail was also consistent with a stronger recent trend in sales, with revisions adding 0.3% to the prior month, and the control group rising 0.7% (0.3% expected) with net revisions of +0.6% and providing no evidence of a rollover in spending. Target earnings contrasted the retail sales result, saying that consumers pulled back on their spending in recent weeks with sales worsening sharply in October and November. Target’s share price slumped almost 15% as it lowered guidance for the current quarter and said it would need to discount heavily to clear excess inventory.

San Francisco President Daly was explicit that “pausing is off the table right now, it’s not even part of the discussion,” with the discussion instead on slowing the pace. As for where rates should go, Daly nominated “somewhere between 4.75 and 5.25 seems a reasonable place.” and said the unemployment rate might need to move higher to 4.5-5%. Kansas President George said the real challenge for the Fed “is being careful not to stop too soon,” citing the 70-80s experience. She said the tide had turned on supply chains but “now, we’re really looking at labor as the driver here” warning that “I don’t know how you continue to bring this level of inflation down without having some real slowing, and maybe we even have contraction in the economy to get there.”

New York President Williams said, “restoring price stability is of paramount importance because it is the foundation of sustained economic and financial stability.” making the case that monetary policy should not focus on financial stability risks because it can lead to worse outcomes for the economy. Speaking in the last hour or so, Governor Waller said he is comfortable with slowing the pace, but the size of the next move is data dependent.

Fed commentary, like the resilient spending numbers, gave little succour for anyone looking for an imminent pivot. US 2yr yields were 3bp higher to 0.437 as the curve inverted further. The 10yr was 6bp lower to 3.71% with the 2s10s spread falling to -67bp. In Europe, yields were lower. 10yr German bunds were down 11bp to 2.00%, while the 2yr was 7bp lower to 2.084%. Bloomberg reported that “initial discussions suggest a lack of momentum for another 75 basis-point move” among ECB council members, citing people with knowledge of the matter. That comes as Bank of France head Villeroy predicted that the ECB will probably hike to a “normalization range” of around 2% next month. Market now price 56bp of hikes for the 15 December meeting, 5bp less than yesterday. Vice President Guindos said the November 30 inflation data will be “relevant” for the decision

Moves in currency markets were relatively muted. The dollar was unchanged on the DXY at 106.43 and largely consolidating after its recent sharp decline. The EUR was 0.2% higher at 1.0373 but got as high as 1.0438 intraday before paring some of the gains following the Bloomberg report pointed to 50bp from the ECB in December. The AUD was 0.4% lower to 0.6728 and still around 5% higher than prior to US CPI last week.

UK inflation data came in on the high side of expectations at 2.0% m/m (1.8% consensus) and 11.1% y/y (10.7% consensus) . Energy prices were the dominant contributor, but there was still breadth to price rises with the core number was also strong, remaining at 6.5% y/y against expectations for a 1 tenth fall to 6.4% and services inflation was 6.3% y/y. On the month, gas prices surged 36.9%, and electricity rose 16.9%. The ONS said without the energy price guarantee, inflation would have hit 13.8%. Markets currently price a 40% chance of another 75bp hike in December, despite warnings from some BoE MPC members that the extent of tightening priced by markets would lead to a larger downturn than required to get inflation under control.

In Canada, annual CPI was steady, at 6.9% y/y on a 0.7% monthly gain and broadly in line with expectations. The average of the Bank of Canada’s three core inflation measures ticked up to 5.4% y/y, still way above target.

Australian WPI wages rose 1.0% q/q and 3.1% y/y , above both the consensus forecasts for 0.9% q/q and the RBA’s implied forecast track of 0.8-0.9% q/q. Driving the result were private sector wages which rose 1.2% q/q and 3.4% y/y as growth for those on individual agreements accelerated sharply. By contrast, public sector wages grew by 0.6% q/q and 2.4% y/y. The parts of the wages basket that are most responsive to labour market conditions accelerated sharply, and though the large minimum wage increase was a factor in the quarter challenges the RBA’s assessment that the wages growth backdrop will remain consistent with inflation falling back to target. Markets continue to price only around 20bp of hikes for the December meeting.

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.