Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

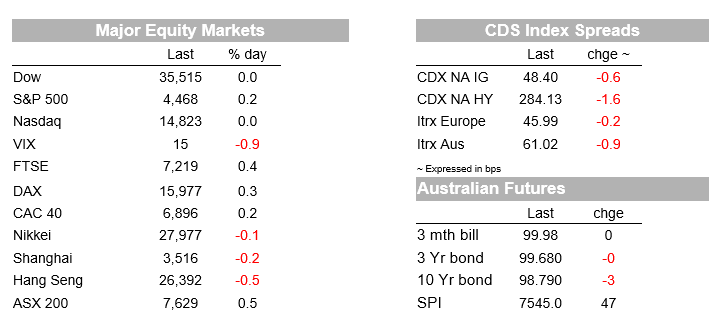

US consumer sentiment plunges to below pre-pandemic levels with yields tumbling (US 10yr -8.2bps), but equities steady to higher with the S&P500 +0.2% to a new record high. For bonds, the plunge in consumer sentiment is an amber signal for the near-term, which if realised in real activity may impact on the timing and form of tapering and puts the focus squarely on retail sales on Tuesday

https://soundcloud.com/user-291029717/back-to-uncertainty?in=user-291029717/sets/the-morning-call

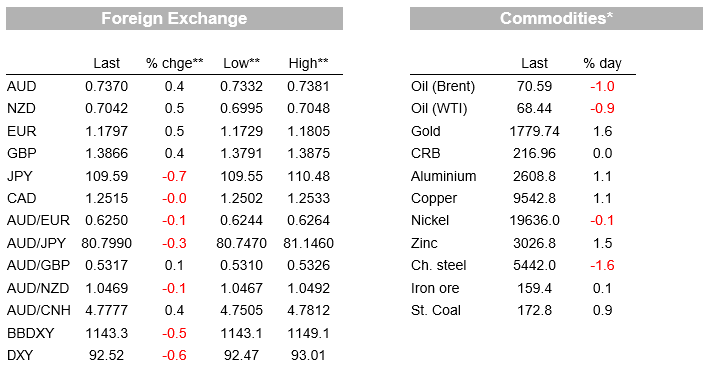

US consumer sentiment plunges to below pre-pandemic levels with yields tumbling (US 10yr -8.2bps), but equities steady to higher with the S&P500 +0.2% to a new record high. For bonds, the plunge in consumer sentiment is an amber signal for the near-term, which if realised in real activity may impact on the timing and form of tapering and puts the focus squarely on retail sales on Tuesday. As for equities, earnings continue to support with 90% of S&P500 companies reporting so far and 88% of those beating expectations. Tech continues to outperform with Disney +1.0% after reporting blockbuster earnings and higher than expected subscriber numbers for Disney+ after the close on Thursday. Trading was also thin amidst the summer holiday season with the S&P500 recording its lowest daily trading volume of 2021. The USD fell alongside yields with the broad BBDY ‑0.6%. Safe havens outperformed slightly with USD/Yen -0.7% and USD/CHF ‑0.9%. Bond and FX markets continue to be more cautious than equities amid the delta variant.

First to the plunge in US Consumer Sentiment . Headline Consumer Sentiment fell 13.5% in August to 70.2 from 81.2 previously and expected, which is not only below the pandemic low of 71.8 recorded in April 2020, but is also the lowest since December 2011. As for the percentage fall, the 13.5% fall is the seventh largest monthly fall in the history of the survey that dates back to 1953, and in recent times is beaten only by the GFC (-18.1% in October 2008) and the initial phase of the pandemic (-19.4% in April 2020). The University of Michigan notes delta concerns was the primary driver, noting that “c onsumers have correctly reasoned that the economy’s performance will be diminished over the next several months, but the extraordinary surge in negative economic assessments also reflects an emotional response, mainly from dashed hopes that the pandemic would soon end” (see University of Michigan for further details). Inflation expectations also moved higher with the 5-10 year at 3.0% from 2.8%, but still relatively anchored given 3% is what it was in 2013 with core inflation undershooting the Fed’s 2% target since 2012.

Does the survey signal an imminent turn in the US economy? We doubt it given vaccine efficacy remains high and the hit to sentiment likely means more people will get vaccinated (61.7% of US adults are fully vaccinated compared to 76.7% in the UK). Instead the delta surge in the US is more a case of delay rather than derail as far as the recovery is concerned. The experience of the UK and Israel continue to show high vaccination rates severely weaken the link between new cases and hospitalisation, allowing countries to start to transition to living with the virus with a high vaccination rate. As for the short-term economic impacts from the delta surge, it is worth noting that on Thursday South Western Airlines warned that it had seen a deceleration in bookings and a rise in cancellations due to the delta variant, while the WSJ notes SafeGraph reported traffic at grocery stores, gas stations, gyms and restaurants fell starting in late July, after having surpassed 2019 levels earlier in the summer. A Covid outbreak in China has also partially shut China’s Ningbo-Zhoushan port, which also suggests supply chain disruptions will continue for some time due to delta.

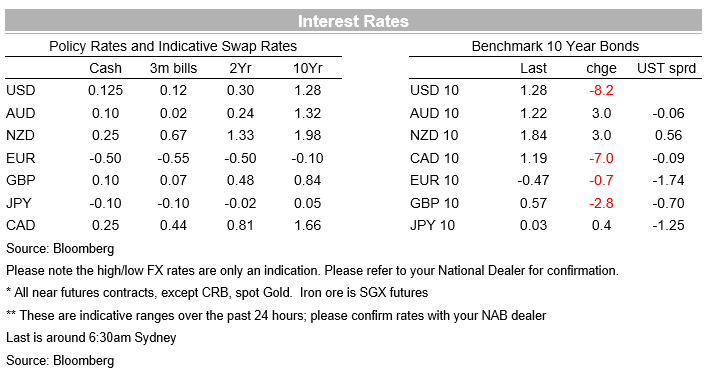

Yields fell swiftly in the wake of the sentiment plunge with the curve bull flattening after its bear steepening last week. The US 10yr yield fell 8.2bps to 1.28% to be 2bps lower than it was at the start of the week. The fall was driven by both the implied inflation breakeven (-3.7bps to 2.38%) and the real yield (-4.3bps to -1.11%). The 5s30s curve flattened 1.9bps to 115.3bps with the 30yr yield at 1.93% and the 5yr at 0.77%. US Fed Chair Powell’s comments on Tuesday will be closely watched to see whether the delta surge is likely to delay a likely tapering announcement (or form of taper). In FX the USD fell across the board with the BBDXY -0.6%, with only USD/CAD bucking the trend at -0.0%. EUR was +0.5% and GBP +0.4%, with the AUD +0.4% and NZD +0.5% moving similarly. Despite the broad-based fall in the USD, risk havens outperformed slightly with USD/Yen -0.7% and USD/CHF -0.9%. Over the week the AUD is up 0.3%, similar for most other majors with EUR +0.3%. Commodities were mixed, with copper (+1.1%) and gold (+1.6%) rising on the back of the weaker USD, while WTI (-0.9% to $68.44) fell on growth concerns.

Australia’s virus outbreak also appears to be going from bad to worse. Sydney’s protracted lockdown has been widened to the whole of NSW, with Sydney’s lockdown set to be extended into September and perhaps even into October. Meanwhile Melbourne’s two week lockdown (coming just 8 days after a 12 day lockdown) looks like it may be extended for another two weeks. The RBA’s most recent August SoMP forecasts are in danger of being out of date within just a week with the detraction in Q3 GDP likely a lot larger than what the RBA had pencilled in. PM Morrison on Friday noted 762,879 NSW people who had lost hours had received income support so far as had 252,843 in VIC. Much of the adjustment in the labour market is likely to come through hours (rather than outright employment losses), though the risks to outright unemployment rises each week. We get the first update on Employment on Thursday in the July Labour Force. NAB still expects a swift rebound in activity once restrictions start to ease when the 70-80% vaccination hurdles are met – on our projections these could be reached by mid-November. Thus the rebound may not occur until late Q4.

Finally in political news, House Democrats are set to progress both the $1 trillion bi-partisan infrastructure bill and the $3.5 trillion budget framework simultaneously, which may increase the probability of the infrastructure bill passing. Note the House reconvenes on August 23. Meanwhile in geopolitics Afghanistan looks like it will fall to the Taliban who are now on the outskirts of Kabul. We do not think this development will have an immediate impact, though it could prove to be a source of regional instability in the medium term.

A big day in Asia with Japanese Q2 GDP and Chinese Activity Indicators headlining. Domestically there is nothing scheduled amid ongoing focus on virus counts and lockdowns. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.