Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

The US President has said the US needs to get back to work, vaccine or not.

https://soundcloud.com/user-291029717/back-to-work-and-back-to-the-trade-war?in=user-291029717/sets/the-morning-call

Ooh, God, that’s the trouble with me, I need the trouble with you

Ooh, God, that’s the trouble with us, I need the trouble with trust – Chet Faker, Marcus Marr

China and US tensions moved up a notch on Friday and US economic data releases depicted a dire picture of the economy and the Consumer. In spite of the troubling backdrop, equity markets continue to see the bright side of life while a more cautious tone was evident in FX with the USD stronger against growth and commodity linked currencies and softer against safe havens such as JPY and CHF. Oil prices had a solid Friday, capping a very strong week.

The US has moved to limit Huawei’s semiconductor chips supply by tightening restrictions on foreign companies delivering Huawei with semiconductors used in their mobile phones. The new restrictions aim to prevent manufacturers producing key parts for Huawei, using US technology, in offshore production facilities without a licence. The Commerce Department said it would extend a temporary 90-day waiver, allowing firms to supply Huawei over this period, but indicated that this would be the last extension.

In response, the Chinese state-owned Global Times reported that China was prepared to retaliate by putting certain US companies (such as Apple, Cisco and Qualcomm) on its “unreliable entity list”, subjecting them to investigations and new restrictions. The Global Times also said China was prepared to stop purchases of Boeing aeroplanes.

US retail sales collapsed in April, breaking the previous record printed in March (Retail sales ex auto, gas (m/m%), Apr: -16.2 vs. -7.6 exp.), meanwhile April industrial production fell 11.2% m/m after falling 4.5% in March.

Market reaction to these dire data releases what short lived, suggesting investors are now placing more value on forward looking indicators rather than real economic prints, which we all know have been negatively impacted by containment measures against COVID-19.

So on the more promising side, the University of Michigan sentiment index came at 73.7 in May, a little above the 68 expected by markets. Importantly too, the NY Empire manufacturing Survey printed at -48.5 in May vs -60 exp. And -78.2 previously, suggesting activity likely bottomed in April. Still the survey suggests that 63.1% reported general business conditions lower while only 14.5% reported higher.

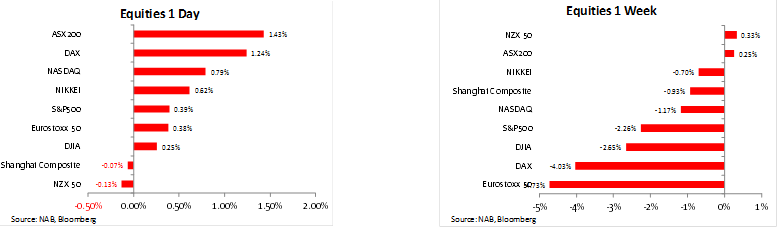

US equities finished the week on a positive note with modest gains for the day notwithstanding the negative US-China vibes and less than impressive US data releases. Talks of an acceleration in the discovery of a COVID-19 vaccine appears to have helped sentiment .The race to find a vaccine continues apace, with more than 100 vaccines in development globally according to the WSJ. Small US biotech firm Sorrento Therapeutics saw its share price rise almost 200% after it claimed that initial lab results on its experimental antibody were effective against COVID-19.

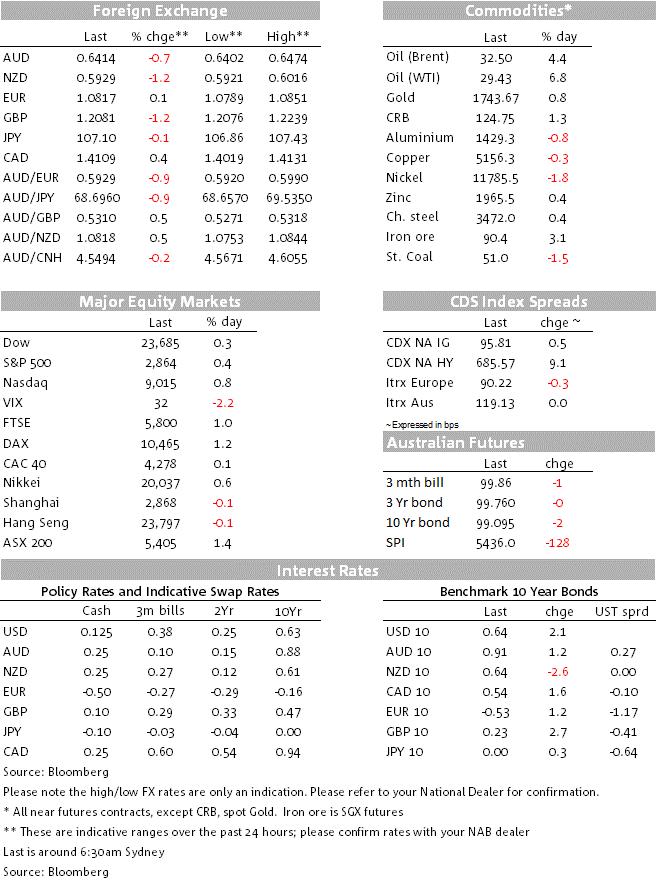

European and US equities had a bruising five days. The S&P 500 was down 2.26% , it worst week since the meltdown in the second half of March and Europe fortunes were even worst with the DAX down 4.03% and the EuroStoxx 50 -4.73%. The US earnings reporting season is coming to an end, but we could still have a sting in the tail with many retailers reporting this week, including Walmart, Home Depot, Target and Best Buy.

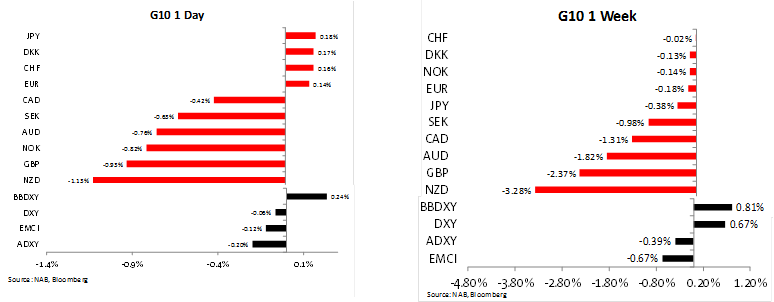

In contrast to equities, Friday’s price action depicted a more cautious mood in the air. The USD ended stronger n when we look at the broad BBDXY index ( +0.25%) but a tad softer in the narrower DXY (-0.06%), reflecting the outperformance of the safe Havens such as JPY and CHF. Meanwhile growth and commodity linked currencies underperformed with NZD (-1.13%) and GBP (-0.93%) at the bottom of the pile. The kiwi ended the week at a three-week low around 0.5935 with last week’s dovish tone from the RBNZ probably the main cause for NZD’s underperformance, given the Bank’s openness to lowering the OCR sub zero next year.

GBP underperformance can be largely attributed to renewed UK-EU trade concerns. The Brexit process remains a big uncertainty, UK’s chief negotiator Frost said “very little progress” had been made in the talks with the EU while EU chief negotiator Barnier said he wasn’t optimistic.

The pound has come under renewed pressure this morning, falling an additional 20 pips to 1.2090 following weekend comments from BoE Chief Economist Haldane noting the Bank is examining unconventional monetary policy measures more urgently amid the economic slump caused by the coronavirus pandemic. Haldane went on to add that the Bank had plenty of other options available besides cutting the cash rate further, including expanded asset purchases (including into higher-risk asset classes). Governor Bailey said last week that the Bank wasn’t currently considering negative interest rates.

The AUD fell 0.76% on Friday and true to form the AUD continues to show its sensitivity to US-China developments. On the week the AUD followed the NZD and GBP as the main underperformers, down 1.82%. That said for now the pair remains contained within its recent 0.6373 and 0.6570 range. Australia and China relationship has also been a focus for the AUD following the Morrison government’s proposed coronavirus inquiry.

Overnight the AFR reported China has sought to defuse tensions with Australia insisting it is committed to the free-trade deal. China’s Foreign Ministry said on Sunday the trade deal -signed in 2014 after a decade of negotiations – had brought “concrete benefits” to both countries and its position on the agreement, which cut tariffs on most Australian exports, was unchanged. The AUD has opened the new week little changed at 0.6419.

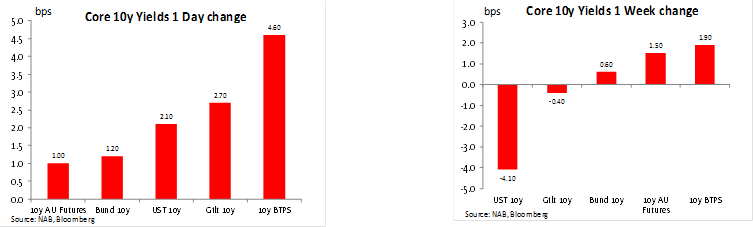

Global rates edged higher on Friday, but remain at extremely low levels. The 10-year US Treasury yield rose 2bps to 0.64%. The US Federal Reserve said it would taper back its bond buying further, from $7b per day in US Treasuries and $5b in mortgage bonds to $6b and $4.5b respectively in the week ahead.

The Fed released its bi-annual financial stability report on Friday and warned stock and other asset prices could suffer significant declines should the coronavirus pandemic deepen, with the commercial real estate market being among the hardest-hit industries. Fed Chair Powell CBS’s 60 Minutes interviewed will be air this morning (9am Sydney time), but CBS notes Powell the US economy will recover from the coronavirus pandemic, but the process could stretch through until the end of next year and depend on the delivery of a vaccine.

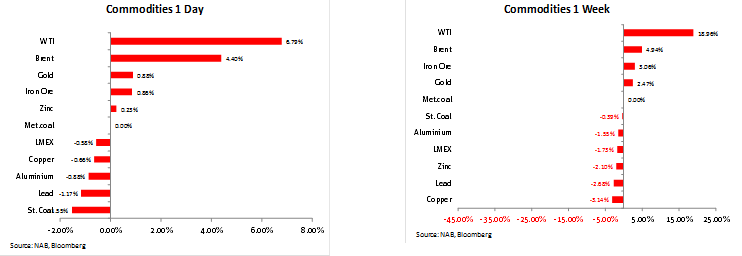

Brent crude oil increased 5%, reaching a two-month high of $31.50 ( WTI gained 18.96% on the week). The US rig count is now at its lowest since 2009, as shale oil operators continue to shut down production. Despite the rise in oil, there was weakness in other parts of the commodity market, with copper (-0.4%) and nickel (-1.8%) declining on Friday. Gold and iron ore where the other performers on Friday and on the week.

The US House of Representatives narrowly (208 to 199) approved a $US3trn bill constructed by Democrats to provide more aid state and local governments, a “Heroes Fund” for essential workers and make another round of payments to individuals of as much as $1,200;. The bill is not expected to pass the Senate, but there are increasing hope it will lead to negotiations for more stimulus with congressional Republicans and Trump, who have been talking about the need for new business liability protections in the age of coronavirus or additional tax cuts.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.