Confidence and Conditions Lift

Insight

US equity markets slip for second day, bigger falls in Europe amid more cautious mood. NY Fed’s Williams re-enforces markets views post-Jackson Hole, August payrolls.

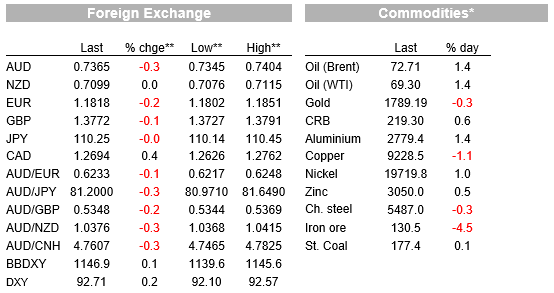

Whether or not because of fresh waves of concerns about the economic impact of the spread of covid-19 – but where there has not been any ratcheting up of the negative news flow – equity market have maintained the more cautious tome evident since the end of last week. This sees bond yields retracing some of their recent back up, aided by a strong 10-year Treasury auction result, while the US dollar is once again attracting a haven bid (DXY +0.2%) the flip side of which is that AUD/USD is down a quarter of a percent on Tuesday’s close at 0.7365, but which still leaves it above key support levels.

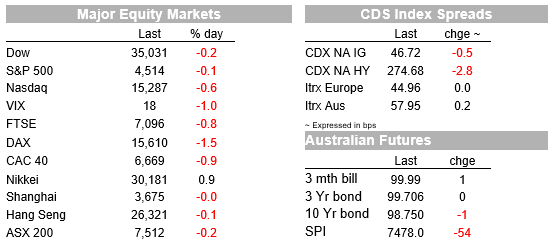

Perhaps a better explanation than covid-related news for the softer US equity tone overnight, continuing on from Tuesday’s modest losses, is the fact that a couple of global investment banks have been out with ‘underweight’ recommendations, while another is reportedly suggesting that any pull-back in US stocks could be amplified by the weight of long positioning. This follows downgrades to 2021 US growth projections by another investment bank on Tuesday and which spawned plenty of media attention. Before we start getting too alarmed though, note the S&P 500 is back a mere 0.5% on the new record highs recorded only last Thursday, while the 1.1% fall in the Eurostoxx50, bringing Tuesday and Wednesday’s combined loss to 1.6% is off a record high seen on Monday.

That said, defensive posturing is evident in the sector breakdown of the S&P, with Utilities, Consumer Stapes and Real Estate all doing well overnight, just not enough to keep the overall index in the green (-0.13%) and where Energy (-1.3%) followed by Materials (-1.0%) have fare worse (so certainly synonymous with downgraded near-term US growth expectations).

On the news front, the Fed’s Beige Book, compiled for an released in front of the Sep 21-22 FOMC meeting, notes that US economic activity “downshifted” in July and August due to rising concerns about COVID’s delta variant, as well as supply chain problems and labour shortages. The survey said the slowdown was largely attributable to a pullback in dining out, travel and tourism in most parts of the country, reflecting concerns about the spread of the delta variant.

On the more positive side, the JOLTS report for July showed a further widening in the gulf between job openings (up to a new high of 10.934mn) and hirings (down to 6.667mn). While an indicator of labour market strength, it does also further highlight the potential skills/location mismatch in the labour market which could take a long time to be resolved.

On the Fed speaker circuit, New York Fed President John Williams , part of the FOMC inner sanctum along with Powell and Clarida, has been speaking. He says there has been very good progress toward maximum employment, but wants to see more improvement before being ready to declare the test of substantial further progress being met. “Assuming the economy continues to improve as I anticipate, it could be appropriate to start reducing the pace of asset purchases this year,” Williams said (a line last used by Fed chair Powell in his Jackson Hole address now almost two weeks ago). He said the delta coronavirus variant is weighing on consumer spending and job growth, and that there is “a long way to go” before the central bank will meet a separate test to begin to raise short-term interest rates, in which respect Williams said he expected inflation to slow down to a 2% rate next year.

The Bank of Canada left its policy settings unchanged, as expected, and while it acknowledged the weaker than expected Q2 GDP data, the Bank continued to expect the economy to strengthen in the second half. The market continues to expect a further tapering of QE from the current C$ 2bn weekly pace, ahead of higher rates in the second half of next year. There was little net market reaction on CAD or in the rates market.

Bank of England officials have also been speaking in parliament, the highlights of which were from Governor Bailey, who said that he was one of the four members who thought that the minimum criteria for tighter UK monetary policy had been met. Still, he stressed that even with the 4-4 split on the MPC (with one vacancy), those who thought the condition of the forward guidance had been met didn’t consider there were sufficient grounds to push for immediate tighter policy”.

The focus in the UK this week has been more on fiscal policy than monetary policy, with the controversial proposed increase in National Insurance, a burden of £12b on workers and companies (worth some 0.6% of GDP), and breaching a promise by the government on taxes, passed in the last couple of hours. before we went to press, PM Johnson won the vote to pass this tax increase, which will take the tax revenue to GDP ratio up to its highest level on record. Neither this nor the BoE speak has made much of an impression on GBP, while prior to the parliamentary vote, 10 year gilt yields were +0.6bp, which in the context of falls elsewhere does owe something to the BoE rhetoric.

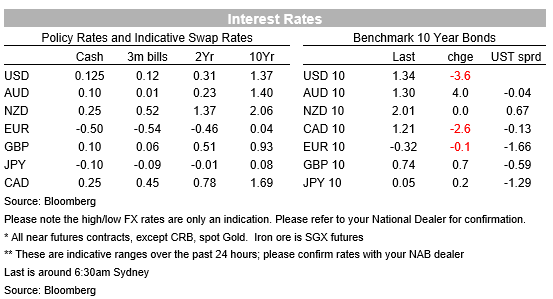

US bond yields have fallen by 3.6% at 10 years, a move down aided by a strong result for the 10-year Note auction, which cleared some 1.5bps below where it was trading in the when-issued market just prior to the auction. Incidentally, Treasury Secretary Janet Yellen has been out warning that the government is likely to run out of cash in October (when the new fiscal year begins) in the absence of an interim lift to the debt ceiling, something not a single Republican Senator is in a mood to support.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Confidence and Conditions Lift

Insight

Online retail sales growth slowed in May following a fairly strong April

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.