Robust growth for online retail sales observed in June

Insight

Reassurances from US authorities not enough yet to appease markets. Bank stocks remain under pressure with bond yields diving as the path of future Fed hikes comes into question. The USD is also weaker across the board.

NZ: Perform. of services index, Feb: 55.8 vs. 54.7 prev.

NZ: Food prices (y/y%), Feb: 12.0 vs. 10.3 prev.

Measures by the US Treasury, Fed and FDIC have so far prevented a US bank run on deposit but have not been enough to avert a bank run by investors. Overnight price action has been dominated by a rush to reduce exposure to the US banking sector with regional banks leading a sharp decline in bank stocks. The slump in UST yields has extended over the past 24 hours with front end yields leading an aggressive bull steeping of the curve. The market has also trimmed near term Fed and ECB rate hikes expectations with over 80bps of Fed rate cut now seen before year end. The decline in yields sees the USD weaker across the board while gains in risk sensitive equity sectors are helping main US equity indices head into a positive close, notwithstanding loses in financial stocks.

Yesterday morning (Sunday evening NY time) the US Treasury, Fed and FDIC announced a bundle of measures primarily aimed at protecting depositors with liquidity provisions for banks . The joint statement noted that the FDIC will resolve SVB in a way that “fully protects all depositors.” Similarly, “all depositors” at Signature (a main bank to the cryptocurrency industry which was also closed down by regulators) will be made whole. The Fed also announced a new “Bank Term Funding Program” that offers one-year loans to banks under easier terms than it typically provides. In addition, the Fed also relaxed terms for lending through its discount window, its main direct lending facility. Importantly the Fed will apply no haircut to the necessary collateral. This means banks can get bigger loans than usual for bonds and they don’t have to sell securities at a loss. Bloomberg notes US banks were sitting on more than $300bn of losses on securities they planned to hold to maturity at the end of 2022.

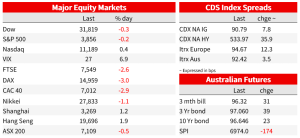

Measures by authorities have so far prevented a US bank run on deposit but have not been enough to avert a bank run by investors. The risk of a financial crisis remains elevated, and investors have rushed to reduce their exposure to the sector . The KBW Bank index is down 12%, its biggest decline since the start of the pandemic on Mach 2020, regional banks have led the declines with Western Alliance Bancorp plummeting 61% before a trading halt, and First Republic Bank diving 66%. There have also been several regional banks that fell more than 20% on the day.

Risk aversion in the air is also palpable in the big increase in the VIX index, jumping above 30 at one point during the overnight session before easing down to 26 where it currently trades. Credit spreads have come under pressure with US high yields spreads widening some 43bps and investment grade 13bps.

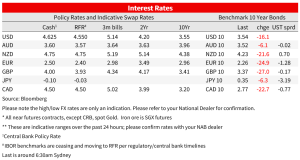

The bank led turmoil has also triggered big moves in the rates market. Yesterday, Goldman Sachs became the first bank reported to call that the Fed would no longer hike rates next week then overnight the likes of PIMCO and NatWest Markets also joining the call. Fed Fund futures are now pricing +13bps for the March 22 FOMC meeting, compared to +33bps at Friday’s close and +43bps soon after Fed Chair Powell’s testimony to lawmakers last week. Of note too, the market not only sees a lower peak in the Funds rate now at 4.74 (down from around 5.68% last week), but also a sooner and faster pace of rate hikes thereafter. The market now sees the fund rate ending 2023 at 3.785%, that is almost a 100bps of rate cuts.

As many commentators have noted overnight, the market is now seeing a big tightening in US financial conditions, the collapse of SVB effectively means US banks will now need to lift their lending rates in order to attract deposit whiles at the same time they are likely to adopt a more cautious approach to lending . The Fed has been aiming to tightening conditions to cool the economy, now the Fed’s jobs has become easier in this regard, with banks expected to do the heavy lifting.

The decline in rates has not been limited to the very front end of the curve. The UST curve has enjoyed an aggressive bull steepening with the 2y tenor down 58bps (two hours ago it was down 46bsp) to 4.01% as I type. The 10y Note is also down around 16bps to 3.49%. Closing of short positions have likely exacerbated the moves. The 2s10s curve is now only inverted by 46bps, from a peak inversion last week of 110bps. This are big moves!

As my BNZ colleague Jason Wong notes curve inversion is a harbinger of economic recession, and it is well known that in terms of timing, the actual inversion is not the best indicator, it is the subsequent steepening of the curve which gives the best signal on that. The fact that the entire Treasuries curve now sits below the Fed Funds rate has also been a good predictor of economic recession.

Looking at other rates markets, the ECB meets later this week and concerns of contagion into the European markets has also triggered a repricing of ECB rate hike expectations . Pricing for this week has shifted down to +39bps. Before SVB looked to be heading for collapse last week, a 50bps hike was almost a given. The doves on the committee will be arguing for some pullback in the scale of tightening given the turmoil in the banking sector. But at the same time, making a u turn on its guidance for a half-point hike could diminish the bank’s credibility, Europe still inflation problem.

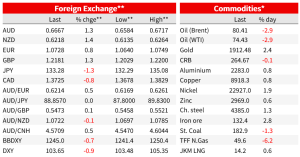

Looking at FX, the USD is weaker across the board with the sharp declines in UST yields and Fed pricing expectations more than offsetting any safe haven bid from the increase in market uncertainty. The DXY index is -0.88% as I type with gains in G10 pair led by NZD and AUD. The kiwi is up 1.34% over the past 24 hours to 0.6219 while the AUD is up 1.31% to 0.6666, the latter traded to an overnight high of 0.6717, before losing some altitude in the past couple of hours. The increase in volatility suggests some short covering may be at play, as traders look to reduce positions, then there is also the argument that Australia’s and New Zealand banking sector are in a better shape to withstand the turmoil seen in the US.

Looking at other G 10 pairs, USD/JPY is down 1.3% to 133. EUR and GBP are up in the order of 0.8-1.2% to 1.0740 and 1.2175 respectively.

US equities look set to end the day mixed. The decline in UST yields has help the tech sector with the NASDAQ up 0.45% while the S%P 500 is down 0.15% with gains in risk sensitive sectors such as real estate and utilities ( both up around 1.6%) offset by declines in financial (3.78%) and energy (-1.96%). Earlier in the session the Euro Stoxx 600 index fell nearly 2½%, with its heavy weighting to bank stocks not helping.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.