On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

After a solid run in the previous two days, equities are taking a breather with European shares closing lower amid concerns over the need for a new round of covid restrictions.

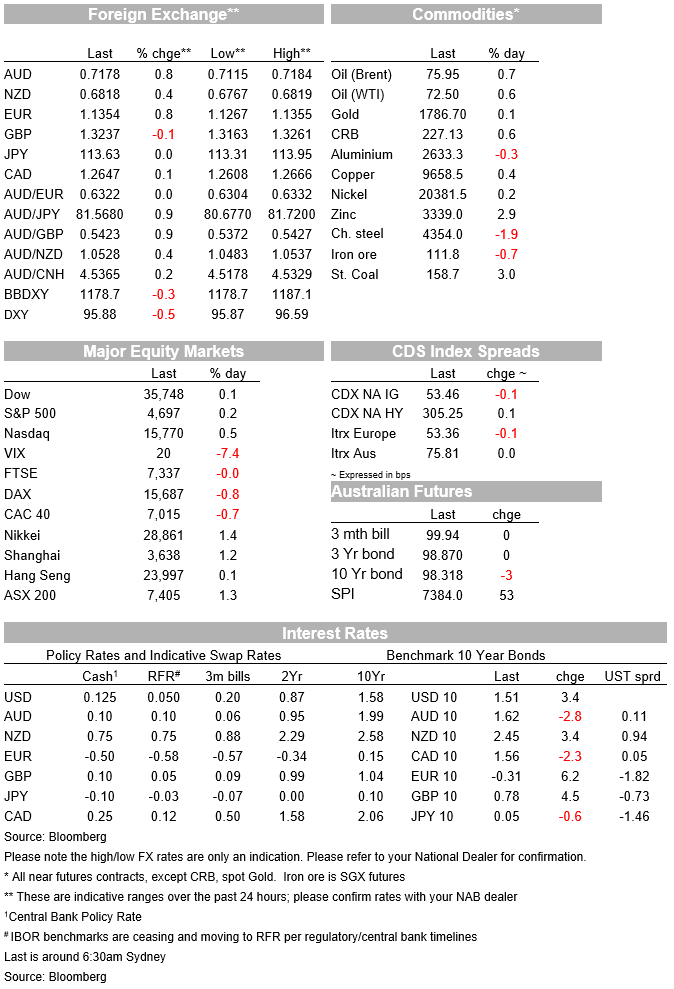

After a solid run in the previous two days, equities are taking a breather with European shares closing lower amid concerns over the need for a new round of covid restrictions. News that Pfizer- BioNTech booster shot is effective against omicron variant lifted sentiment early in the NY session, but as type main US equity indices look set to close a little bit higher. Longer dated UST yields have led a steepening of the UST curve while the USD is a tad weaker with commodity linked currencies edging higher. CNY strength amid improved China growth outlook helping the latter.

After climbing 4.8% over Monday and Tuesday, the Eurostoxx 600 index has closed 1.01% lower overnight. Investors’ enthusiasm has been curbed amid concerns new covid restrictions may be needed, hindering activity. Sentiment took a hit following a Financial Times report that UK PM Johnson was set to announce new measures to limit the spread of the omicron variant. Early this morning PM Johnson confirmed the introduction of Plan B to buy time to get booster shots.

The plan introduces measures such as advising people to work from home and mandating the use of vaccine passports in large venues. Ahead of Christmas, retail, hospitality and leisure spending are likely to take a hit with expectations for a BoE rate hike next week effectively evaporating in the process. A 15bps rate hike is now fully priced for February. The pound lost ground on the FT headlines, trading to an intraday low of 1.3163, but has now retraced all its early decline and trades little changed at 1.3232.

The introduction of new restrictions in the UK are a potential taste of what is yet to come in Europe and other regions around the globe. The UK is among the leaders in terms of booster shots with almost a third of the population triple jabbed, yet with over 51k covid infections recorded yesterday, PM Johnson has been forced to reintroduce restriction. Germany’s delta wave appears to be peaking at the moment, but infections are still rising in other parts in Europe with France now the country to watch. Low booster shots stats and a strong anti-vax movement is a problem for Europe, specially if we see an increase in hospitalisation.

US equities look set to close marginally higher with the Dow up 0.05% as I type while the S&P 500 is 0.15% and the NASDAQ is 0.45%. Financials and Energy are the notable underperforming S&P 500 sectors with health care and communication the outperformers, up ~0.65%

Global yields were already coming off highs before the UK govt announced plan B of greater restrictions, but the announcement provide an extra momentum. UST 2s now at 0.67% vs 0.71% Still, the theme for the day has been a decent UST curve steepening led by the 30y bond up 7 bps to 1.875% (after being 13bps higher with session high 1.88%). Similarly, 10y UST yields now trade 2bps higher on the day to 1.5041, after trading to an overnight high of 1.5349%. Core European yields also closed higher, 10y Bunds up 6bps to -0.33% while 10y Gilts rose 4bps to 0.775%

Early in the session sentiment was boosted by positive Omicron news from Pfizer- BioNTech publishing results of lab tests done on the Omicron variant of COVID19, which suggested a significant reduction in vaccine efficacy from two-doses, but a third booster shot increased antibodies 25-fold compared to the original strain of the virus. Pfizer added that a two-dose regimen may still induce protection against severe disease. The results are broadly consistent with a South African lab study that was released yesterday. Pfizer said a new Omicron-specific vaccine might be available from March 2022.

Moving on to central bank news, as expected the BoC reaffirmed its rate hike guidance the middle quarters of next year. The Bank remain committed to “holding the policy interest rate at the effective lower bound until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved.” Based on the BoCs October projection, this is expected to happen sometime in the middle quarters of 2022. A reference to inflationary pressures being temporary was dropped but overall the incremental change in the statement wasn’t hawkish enough for the market’s liking, and some of the aggressive rate hike path priced from early next year was priced out of the curve. The 2-year bond rate fell 6bps to 1.08% and the CAD was slightly weaker post-Statement and now is unchanged on the day at 1.2649.

An FT poll of economists showed that the majority (56%) expected it was likely or very likely that the Fed’s QE programme would be finished by the end of March and 50% believed the first rate hike would come in Q2, with 10% saying even earlier, in Q1 next year. This closely aligns with market pricing based on Fed Funds futures, which suggest a high chance of a 25bps hike by the end of Q2.

The USD is a tad lower with the DXY index back below the 96 mark. Pro-growth risk sensitive currencies showed little ill effect from the European equity woes with the resilience of US equities and positive vibes coming from China more than outweighing any concerns over covid restrictions . CNY has strengthened to a three-year high, with USD/CNY trading down to 6.34, supported by the policy easing early this week, that incorporated a reduction in the RRR for banks, signs that the government was looking to ease curbs on the property market and attempts to reduce contagion risk from the imminent restructuring of Evergrande debt. This dynamic continues to help lift the AUD and NZD from year-to-date lows printed late last week. The AUD and NZD have made modest gains overnight to add to their appreciation during local trading hours. AUD now trades at 0.7178, up 0.83% over the past 24 hours, while NZD is at 0.6814, up 0.34%.

GBP and CAD are on the weaker side of the ledger, as noted above, alongside the yen, against the backdrop of higher global rates. EUR has enjoyed some support, up 0.9% since this time yesterday to 1.1345.

A final comment on US economic data releases with the JOLTS report showing job openings rising in October to 11m, after two monthly falls, to take it close to the record high set in July. The data remained consistent with a very tight labour market, even if the “quits rate” fell slightly to 2.8% from the record high of 3% in September.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.