Coming in for landing in a heavy cross wind

Insight

If there’s one takeout from the Fed’s Beige Book overnight, aside from the continued improvement in the US recovery, it was the rising concern about input costs.

https://soundcloud.com/user-291029717/beige-book-highlights-brisk-rise-in-input-costs?in=user-291029717/sets/the-morning-call

“I knew you were waiting. I knew you were waiting for me”, Aretha Franklin and George Michael 1987.

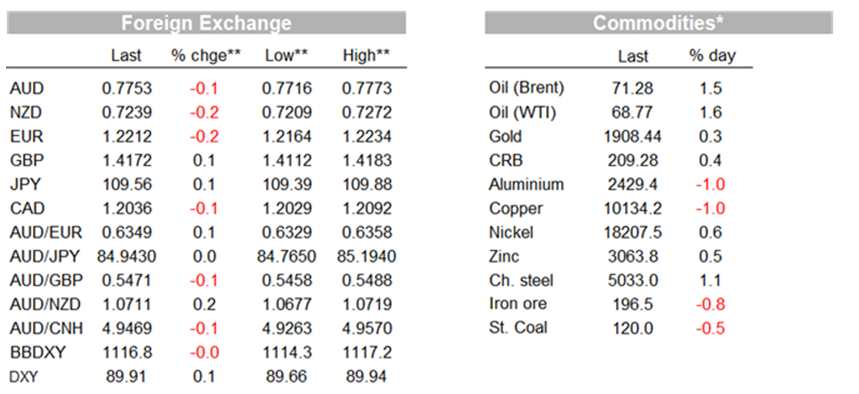

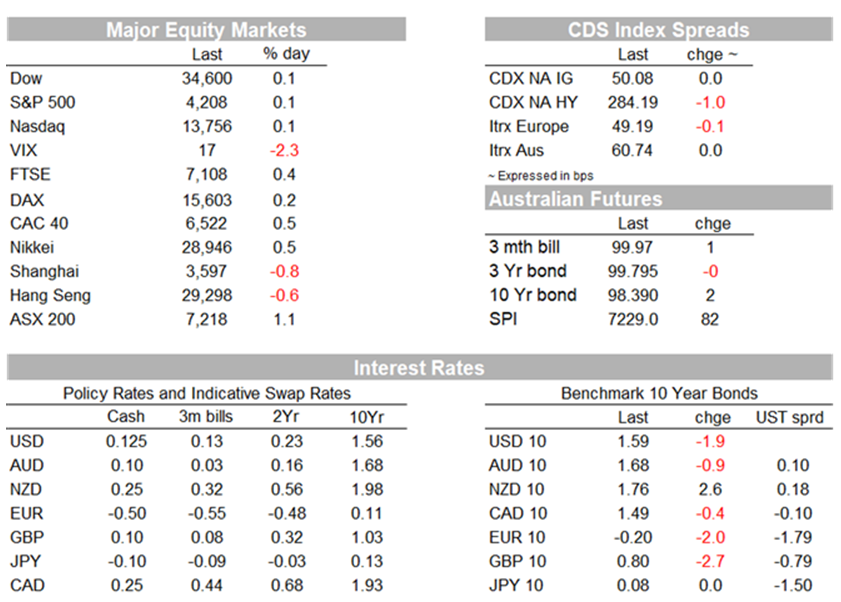

Markets were again very quiet overnight as is typical in a Non-farm Payrolls week. The S&P500 is flat (+0.1%), while rates have been little moved with the US 10yr yield -1.9bps to 1.59%. FX has also been quiet with the USD BBDXY -0.0% with most pairs +/- 0.2% (EUR -0.2%, GBP +0.1%, USD/Yen +0.1%). CAD (USD/CAD -0.3%) outperformed on a higher oil price (Brent +1.5% to $71.28), while the NZD (-0.2%) has underperformed slightly. The AUD (‑0.1%) has largely followed USD moves and is currently trading at 0.7753. Data flow has also light with only the Fed’s Biege Book of note and pointing to inflation pressures (“looking forward, contacts anticipate facing cost increases and charging higher prices in coming months”). Investment managers it seems are also worried with BlackRock’s Fink stating that market was underestimating the risk of higher inflation. The Fed’s Harker also restated his call that the FOMC should “at least think about tapering”. Closer to home, Deputy Governor Debelle yesterday gave further hints that the RBA is unlikely to extend its 3yr YCC target, stating he is hopeful wages growth is 3% + in 2024. Meanwhile the RBA also pushed back on the need to tighten macro-prudential rules and played down the recent pick-up in investor housing activity.

We don’t normally start with Australian data in overnight commentary, but the GDP figures yesterday were remarkably strong (1.8% q/q against 1.5% expected; NAB 1.7%) with the level of GDP now 0.8% above pre-pandemic levels. The data adds to the evidence of a strong rebound in the economy and should prompt questions around the appropriateness of current unconventional policy settings. NAB remains comfortable in its view that the RBA will not roll its 3yr YCC target and will also taper QE in a 3rd round. RBA Deputy Governor Debelle also appeared before Senate Estimates last night and noted the possibility of wages growth at 3% + in 2024 (3% wages growth being seen as needed to have inflation at 2-3% sustainably), which further supports NAB’s view that the RBA will not roll the 3yr YCC target bond from April 2024 to November 2024. Markets are largely there, pricing around a 70-80% chance that YCC will not be extended. Debelle’s colleague Assistant Governor Bullock also pushed back on the need for a tightening in macro-prudential, noting that “lending standards are not being relaxed” and showed no concern around the recent pickup in investor housing credit growth.

As for global markets, it has been a very quiet overnight session. The S&P500 is +0.1% and sits just 0.7% below its record high in May. Below the surface, meme stocks have soared with AMC +95.2% and GameStock +16.2%, while crypto currency Dogecoin is up 30.3%. Frothiness it seems is there, particularly on the retail side, which may be part of the caution being seen in the wider stock market ahead of Non-farm Payrolls on Friday.

Global rates remain largely rangebound having been stuck in a 1.5-1.7% range for a few months. Overnight the US 10yr yield fell -1.9bps to 1.59%. Implied interest rate volatility continues to decline amidst the ongoing range-trading environment, with the MOVE index near its lowest level since February and below its five-year average. The decline in interest rate volatility sits in contrast with the high degree of uncertainty around the inflation outlook. Again, Non-farm Payrolls on Friday could shake things up and until Friday conditions are likely to remain relatively sedate.

As for Fed policy, the Fed’s Harker re-iterated his view that “it may be time to at least think about thinking about tapering”. Meanwhile, the Fed’s Beige Book pointed to growing inflationary pressure. The survey noted “Contacts reported that continuing supply chain disruptions intensified cost pressures. Strengthening demand, however, allowed some businesses, particularly manufacturers, builders, and transportation companies, to pass through much of the cost increases to their customers” and “Looking forward, contacts anticipate facing cost increases and charging higher prices in coming months”. Labour demand was also expected to remain strong, while “a growing number of firms offered signing bonuses and increased starting wages to attract and retain workers” (see the Beige Book for details). The Beige Book overall does little to dissuade investor concerns around the potential for inflation. BlackRock’s Larry Fink the latest to warn on inflation risks, stating “Most people haven’t had a forty-plus year career, and they’ve only seen declining inflation over the last 30-plus years…so this is going to be a pretty big shock.”

Oil prices have made further gains, with US West Texas crude hitting its highest level since 2018 (+1% overnight). Growing market confidence in the global recovery, this week’s announcement from OPEC+ that it intends to only gradually increase supply going forward and diminished expectations for the removal of Iranian sanctions have boosted sentiment in the oil market. Other commodity prices were mixed, with copper falling around 1%, although it remains above the $10,000/tonne mark.

FX moves have been limited with the USD BBDXY -0.1% and most major pairs are within +/-0.2%. The CAD and NOK have outperformed over the past 24 hours (USD/CAD -0.3%) on the back of higher oil prices. At the other end of the currency ladder, the NZD is the laggard, down 0.2%. As for the AUD, it is little changed at -0.1% and currently trades at 0.7753.

Across the Ditch yesterday there were some hawkish headlines from the RBNZ, playing to the view of the need to eventually normalise policy. RBNZ Governor Orr warned of the dangers of not raising interest rates, stating asset prices were “very richly priced” due to the historically low interest rates and would be sensitive to changes in rates. And that that not raising rates could see the return of strong inflation, with flow-on effects to economic activity, welfare and intergenerational equity (see Stuff.co.nz interview for details). Deputy Governor Bascand also noted “our big story is, you shouldn’t expect to have these extraordinary emergency monetary conditions forever”.

Domestically a quiet day with only final measures of the Trade Balance and Retail Sales out. Offshore itiss final-PMI day in Europe, though consensus is around where the flash estimate printed. US data is very heavy with two key released being ADP Payrolls and ISM Services. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.