Economic and financial market update

Insight

Not much reaction to the ECB, says NAB’s David de Garis, but a big reaction in currencies and Treasurys to the latest US GDP numbers. With a lot of European data today and early next week, things could stay quite ‘whippy’.

Events Round-Up

GE: GfK consumer confidence, Aug: -24.4 vs. -24.8 exp.

EA: ECB deposit facility rate (%), Jul: 3.75 vs. 3.75 exp.

US: GDP (ann’lsd q/q%), Q2: 2.4 vs. 1.8 exp.

US: Core PCE deflator (ann’lsd q/q%), Q2: 3.8 vs. 4.0 exp.

US: Durable goods orders (m/m%), Jun: 4.7 vs. 1.3 exp.

US: Durables ex trans. (m/m%), Jun: 0.6 vs. 0.1 exp.

US: Initial jobless claims (k), wk to Jul-22: 221 vs. 235 exp.

US: Goods trade balance ($b), Jun: -87.8 vs. -92.0 exp.

US: Pending home sales (m/m%), Jun: 0.3 vs. -0.5 exp.

Better than expected US data releases, including a solid Q2 GDP print, followed by news that the BoJ will consider a YCC tweak at its policy meeting today, triggered a sell off in UST yields, the curve bear steepened with 10y UST gaining 14bps on the day to 4.0%. The ECB hiked by 25bps as expected, but amid evidence of a weakening economy, it softened it policy guidance. JPY has outperformed against a backdrop of a broadly stronger USD. After a solid start, US equities ended the day in negative territory weighed down by the move up in UST yields.

The ECB policy decision was the first major event in the overnight session and as widely expected the Bank lifted its deposit rate by 25bps to 3.75%. The statement noted that the ECB will ensure that rates remain sufficiently restrictive given that inflation was still expected to remain “too high for too long”. The Bank will continue to follow a data dependent approach to its policy decision adding that it expected inflation to decline over the remainder of the year while also noting that past rate increases continue to be” transmitted forcefully” with financing conditions” increasingly dampening demand, a clear node to the very week Bank Lending Survey released earlier in the week.

Speaking at the press conference, ECB President Lagarde toned down her previous hawkish policy guidance saying that “We have an open mind as to what the decisions will be in September and in subsequent meetings,”. Lagarde also noted how “The near-term economic outlook for the euro area has deteriorated owing largely to weaker domestic demand,” and this cooling of demand should over time ease inflationary pressures over time.

The softening in ECB guidance triggered a move lower in European yields with German two-year yield initially falling as much as 12bps to 3.02%, while the 10-year yield fell 8bps to 2.40%. But this initial declines partially reversed following a move up in UST yields boosted by a stronger-than-forecast US 2Q GDP figures and lower-than-expected US jobless numbers. US equities also opened higher, helped by the better-than-expected US data releases.

US GDP rose an annualised 2.4% in Q2 well above the 1.8% expected by consensus. Details in the report were also impressive with consumer spending up a solid 1.6%, considering the outsized 4.2% gain in Q1. Business investment was strong and stronger than expected durable goods orders bode well for future investment. Initial jobless claims continue to undershoot expectations, and at 221k were the lowest level since February, conveying a message of a still-robust US labour market.

On the inflation side, the GDP report showed weaker than expected PCE deflators with the core rate down to an annualised 3.8%, the lowest increase in over two years.

One major take-away from the recent flow of EU vs US data releases is that the aggressive policy tightening in Europe is certainly having a more significant impact in dampening demand with the Russia -Ukraine war an additional headwind, particularly for the German economy. Meanwhile in the US, notwithstanding 525bps of policy tightening, the economy and consumer resilience continue to surprise. Both central banks have retained a hawkish bias, but the Fed looks more likely to hike again while the data is telling us the ECB is probably done. That said while ECB rate hike expectations have been paired back (pricing 11bps of hikes in September compared to 13bps on Wednesday; peak rate pricing drop 4bps to 3.93% by year-end), Fed pricing expectations have not moved that much with the September Fed meeting priced at just 6bps and a cumulative 10bps priced through to November.

The better than expected US data releases triggered an uptick in UST yields and then the move was boosted by a softer than expected 7y Bond auction. The auction was awarded at 4.087%, the highest on record in 7-year auctions since 2009, and about 1.3bp higher than where it was trading at the bidding deadline.

The move up in UST yields was then turbo charged following a Nikkei report suggesting the BoJ will consider a tweak to it YCC policy at its meeting today. This of course after media reports last week suggesting the Bank was set to stand pat. The article noted that BOJ will consider letting long-term interest rates rise above its 0.5% cap by “a certain degree”. Under the more flexible policy being considered, the BOJ would permit gradual increases above the 0.5% threshold, but still clamp down on any sudden spikes. That would allow it to rein in fluctuations driven by speculators.

The report boosted the move up in longer dated UST yields with the curve bear steeping. Relative to levels seen 24 hours ago, the 2y rate rose 8bps to 4.936% while the 10y climbed 14bps to 4.0%.

The move up in UST yields supported by the solid US data releases, boosted the USD across the board with European currencies the notable underperformers following the dovish hike by the ECB. The USD gained between 0.5% and 0.8% in index terms with the Euro down 1.07% to 1.0978 while GBP fell 1.17% to 1.2796. Following the Nikkei report, JPY is the strongest G10 currency (+0.82%), smartly outperforming the USD. USDJPY now trades at 139.4655.

NZD and AUD also succumbed to the USD strength but to a lesser extent compared to the euro and GBP, down 0.5% and 0,8% respectively. The AUD traded down to an intraday low of 0.6698, and now starts the new day at 0.6709 while the Kiwi trades at 0.6183, 8 pips above its overnight low.

US equities opened higher boosted by the better than expected the US data releases, but as the session went by UST yields climbed higher, equities eventually succumbed to the pressure from higher yields. The S&P 500 closed -0.65% while the NASDAQ was 0.55%. Earlier, the Euro Stoxx 600 closed up 1.4% to reach its highest level since Russia invaded Ukraine .

Coming Up:

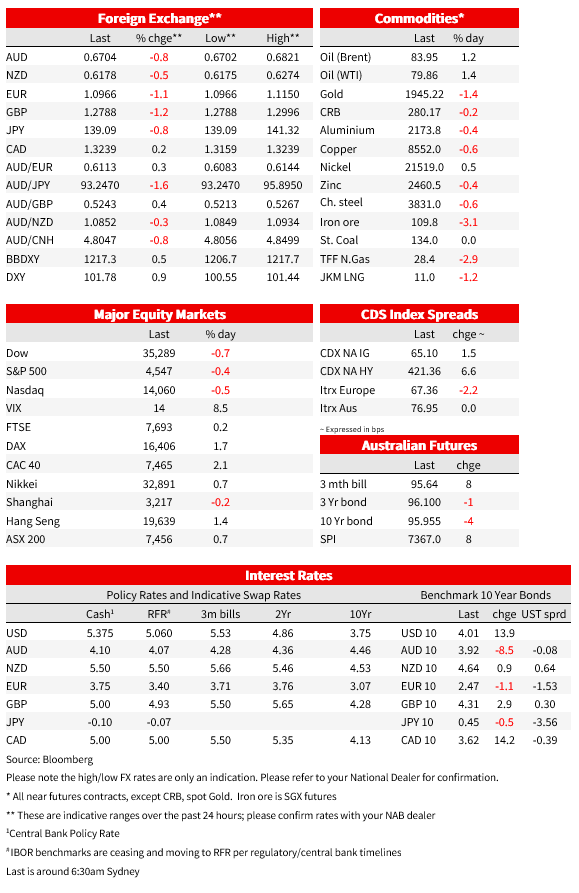

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Economic and financial market update

Insight

Online retail sales growth slowed in March

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.