We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Equities driven higher by Biden’s infrastructure plan deal. NAB’s Gavin Friend says bond markets were unmoved by Fed speakers suggesting higher inflation for longer and rate rises sooner.

https://soundcloud.com/user-291029717/biden-whittles-down-plan-to-win-support?in=user-291029717/sets/the-morning-call

As the first line should make clear, this 1999 Randy Newman song was not meant to be flattering, rather it’s about European Imperialism. A tenuous link therefore to news overnight that Germany, France and Belgium – three of the leading contenders to take down the Euro-2020 trophy (doubtless my Pomy colleagues are begging to differ in one case) all reported stronger business confidence survey readings overnight. Belgium’s hit a record high, France (INSEE) its best since 2007 and the German (IFO) was its strongest since November 2018. All were only marginally beneficial to the Euro.

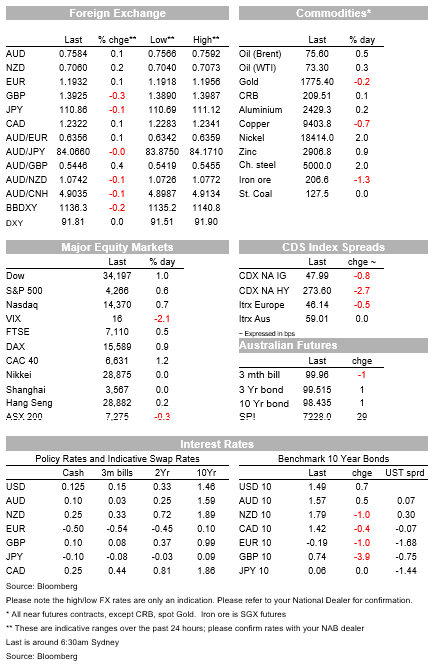

GBP is the weakest G10 currency after the Bank of England failed to provide any succour for the notion of early policy tightening, while AUD is struggling to get back onto a 0.76 handle; whether or not it does ahead of the weekend will be important here regarding the outlook into next Wednesday’s month, quarter, half and, in Australia’s case, year-end.

US President Biden and a group of bipartisan Senator have shaken hands on an infrastructure package touted to be worth $1tn in total over 8 years, though not all new money. Rather some $440bn is from funds saved from previous fiscal packages. It appears though that Democrat Senators are tying their approval to the Biden administration’s separate (now $1.8tn) American Families Plan being approved via the reconciliation process, i.e. without the need for Republican support. The latter is where proposed corporate and other high income earner tax rises are now embedded.

The Infrastructure deal news helped US recover from an intra-dip after opening smartly higher, such both the S&P500 and NASDAQ have posted new record closing highs, S&P +0.6% nd NASDAQ +0.7%. All S&P sub-sectors bar real estate and utilities are in the green, led by a 1.2% gain for financials. In the case of the latter this hasn’t been because of any fresh curve steepening (2, 5 and 10-year Treasuries are all between 0.6 and 1.1bp higher), though post close the Fed has said all 23 big US banks have easily cleared their latest stress tests, news that might have been anticipated earlier in the day.

On the US data front, U.S. weekly jobless claims were 411k last week, higher than the 380k consensus and little changed from 412k the prior week. So the downtrend trend looks to have flattened out, the data are of course noisy on a week to week basis. Durable goods for May saw a headline +2.3% m/m vs. 2.8% consensus and an upward revision to -0.8% in May (previously -1.3%). Core capital goods orders (non-defence ex-aircraft) were also a disappointment relative at -0.1% relative to the 0.8% consensus, though they follow an upward revision to 2.7% in May (from 2.2%).

The Bank of England votes 8-1 for no change to the Bank Rate at 0.1% and to keep QE pegged at £875bn + £20bn of corporate bonds, outgoing chief economist Andy Haldane the lone dissenter. In the accompanying narrative, the BoE says it won’t tighten until there is clear evidence of progress toward its goals, that inflation is expected to exceed 3% for a ‘temporary’ period and – most telling – that it would be wrong to undermine recovery with premature tightening.

GBP/USD has lost about 0.3% on the day and is the weakest G10 currency, some in the market obviously positioned for less dovish/hawkish tilt from the Old Lady. The only other G10 currency down on the day is CAD, off 0.15% for no obvious reason, though we’d note that diplomatic relations between Canada and China look to be taking a furtherturn for the worse. NOK again tops the G10 scoreboard as Brent crude prices maintain their hold above $75 (up another 40 cents overnight to $75.63). The high on AUD/USD has been 0.7592, so as noted above, recapturing the 0.76 handle is so far proving elusive. Whether or not it does before the week is out will be important.

Finally, the law of diminishing returns looks to have well and truly set in with respect to incoming Fed speak. Having just read the transcript of a lengthy Bloomberg radio interview with NY Fed President John Williams you can see why (in the words of Talking Heads’ Psycho Killer, ‘You’re talking a lot, but you’re not saying anything’).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.