Total spending grew 0.9% in June.

There’s still plenty of positive sentiment around as the US, UK and Europe continue to vaccinate at pace.

https://soundcloud.com/user-291029717/bitcoin-stalls-but-us-economy-set-to-rip?in=user-291029717/sets/the-morning-call

‘Cause it’s Saturday night and I just got paid

..My heart says go, go

.I’m gonna rock it up

I’m gonna rip it up – Little Richard

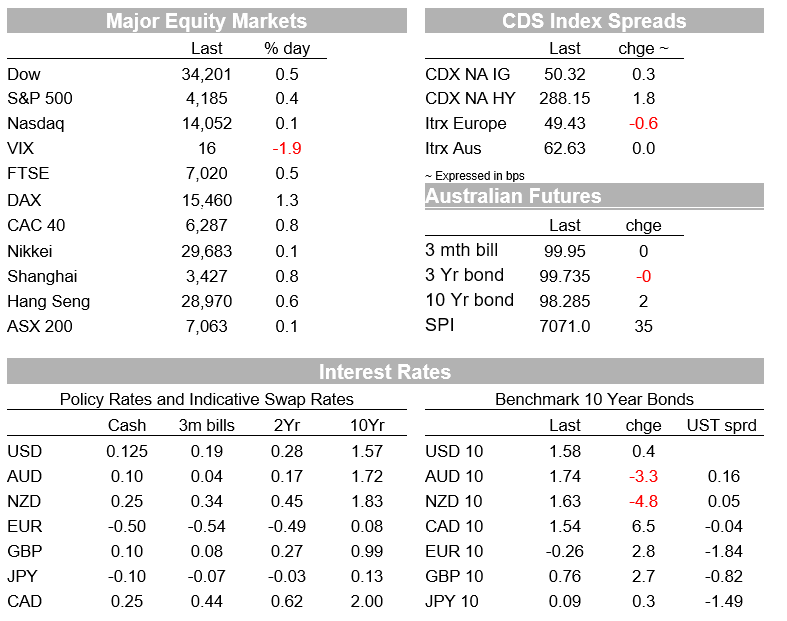

Equities edged higher on Friday with major equity indices in Europe and the US recording new record highs. A supportive policy backdrop and good EU and US Covid news favouring the improvement in risk sentiment with Fed Waller noting the US economy is ready to rip while inflation is only likely to tick higher on a temporary basis. After their big declines on Thursday, UST yields where stable on Friday and the USD was a tad softer, losing ground against GBP and CAD while scrapping small gains against the AUD and NZD.

The extremely supportive monetary and fiscal policy setting continues to provide a fertile environment for risk assets. The S&P 500 gained 0.36% on Friday, its closed at a new record high and recorded its sixth consecutive weekly gain . The Dow closed +0.48%, also at a record high while the NASDAQ climbed 0.1%. In Europe the Stoxx Europe 600 Index jumped 0.9%, helping lift its weekly gain to 1.2%, recording its seventh positive week in a row. Chinese equities had a good Friday, but they were the notable underperformers on the week with the Shanghai Composite down 0.70% while the CSI 300 was -1.37%

US and European COVID news also contributed to the risk positive backdrop . Last week, the US crossed the 200m threshold of vaccine doses administered, with just under 40% of the population having had at least one shot. While the European vaccine rollout is finally gathering some momentum, almost 28m doses have been administered in the EU over the past fortnight, with almost 20% of the population now having received at least one dose.

Echoing the market’s upbeat sentiment, new Fed governor Christopher Waller told CNBC on Friday that he thought the US economy was “ready to rip”, with a clear runway for COVID-related restrictions being lifted in the coming months. But, reinforcing the idea that central banks will be slow to move, despite what will be a sharp bounce back in economic activity, Waller noted that “there’s no reason to be pulling the plug on our support till we’re really through this.” Another factor supporting the Fed’s dovish leanings is its greater focus on broader measures of labour market performance, with Waller observing that unemployment rates were still relatively high for minority groups

COVID news in other parts of the world unfortunately have not been great, India reported another daily record of new infections and ahead of the BoC meeting this week, Ontario reported 4,812 new cases in 24 hours, more than half of Canada’s total. Ontario unveiled its strictest measures yet to limit the movement of people.

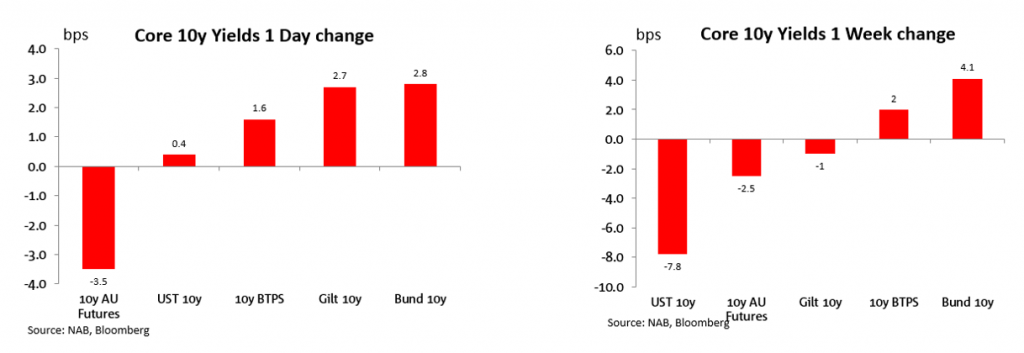

Moving onto the rates market, after the big declines on Thursday, longer dated UST yields had a relatively quiet Friday with the 10y Note and 30y Bond little changed on the day. 10y UST yields closed the week at 1.5798%, down 8bps over the past five days while the 30y yield fell 6bps on the week, closing at 2.268%. Core EU yield in contrast climbed a couple of bps on Friday adding to the rise over previous days, the 10y Bund ended the week 4.1bps higher at -.2650%.

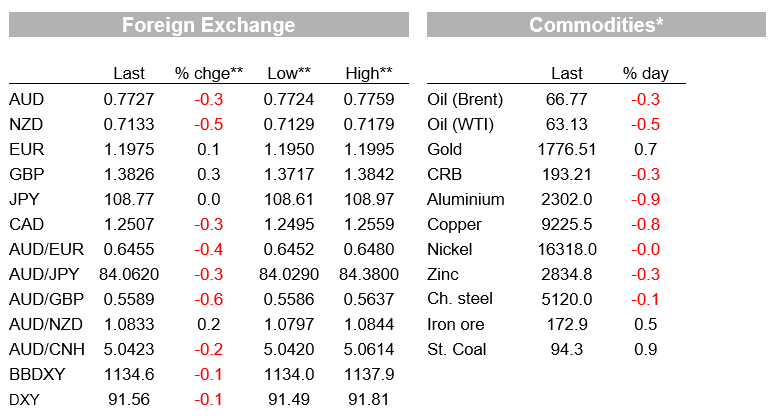

The decline in UST yields has certainly played a part on the weaker USD over the past week. On Friday, as UST yields consolidated the previous day’s decline, USD indices were marginally lower with GBP and CAD outperforming while the AUD and NZD were a tad lower notwithstanding the risk positive equity backdrop. Cable gained 0.33% on Friday closing the week at to 1.3832, CAD was up .028% while the AUD slipped 0.23% and the NZD was -0.39%. The AUD now begins the new week at 0.7730 and NZD is at 0.7127, both antipodean pairs recorded decent gains for the week, up over 1%.

Ahead of the ECB meeting this week, the EUR increased slightly on Friday (+0.1%), with the market turning a bit more optimistic around the European vaccination drive, the union currecny ended the week just below the 1.20 mark. USD/JPY was also little changed on Friday, consolidating its decline below the 109 mark.

Commodities had a mixed day on Friday and probably contributed to the AUD pullback on the day. Iron ore gained 1%, but metal prices and copper were down between 0.5% and 1.3%. However, looking at the performance for the week, it was all good news within the complex with oil prices leading the gains, up over 6%. A weaker USD no doubt a contributing factor, but perhaps more importantly commodity gains for the week also reflect an increase in confidence in the global growth recovery story.

There wasn’t much market reaction to economic data released on Friday . Chinese GDP growth for Q1 came in weaker than consensus, at 0.6%, but revisions to prior quarters meant the annual rate of growth, at 18.3%, was close to market expectations. The extremely high annual growth rate is flattered by the comparison to the COVID-related slump a year ago. The monthly Chinese activity indicators were a mixed bag, with retail sales stronger than expected in March but industrial production and fixed asset investment weaker than expected. In the US, the University of Michigan consumer confidence index increased to 86.5, although this undershot the consensus which was looking for an even larger rebound.

In other news Bloomberg reports, Blackstone has agreed to sell a portfolio of warehouse and logistics assets in Australia for USD 3bn to property investor ESR Cayman. The sale would mark the largest real estate transaction in Australia in at least five years but is unclear whether the transaction will have any AUD flows associated with it given ESR is a Hong Kong listed while Blackstone is a US listed company.

Bitcoin plunged over 15% at one point on Sunday, now down around -9% following speculation in several online reports that the US Treasury may be looking at cracking down on money laundry activity within digital assets. The drop in bitcoin comes after a big week which saw the crypto currency trade to a new record high on Wednesday and Friday’s decision by Turkey’s central bank to ban the use of cryptocurrencies and crypto assets for purchases. Bitcoin is still up 90% year to date and close to five times higher relative to its level in October last year.

Following a meeting between senior envoys and notwithstanding of an increase in geopolitical tensions, over issues ranging from human rights, trade, technology, Hong Kong and Taiwan, China and the US have agreed to cooperate to tackle climate change. The weekend announcement comes after US President Biden and Japan’s PM Suga said in a joint statement early during our Saturday that said they “shared their concerns over Chinese activities that are inconsistent with the international rules-based order.” China rejected the criticism and accused the presidents of meddling in its affairs.

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.